The global transition to a low-carbon economy and adopting the needed clean energy technologies at scale will significantly impact existing value chains1 and transform production-to-consumption lifecycles. Regulatory and business models will need to rapidly evolve to manage the resulting substantial cost challenges and dramatic shifts in stakeholder interactions while continuing to create value.

Green hydrogen2 is likely to play a pivotal role in a carbon-free future, as its adoption will enable the decarbonization of energy-intensive industrial processes whose emissions are hard to abate through simple electrification—such as steel and cement production. However, to take advantage of the economic opportunities created by its adoption at scale, countries will need to rethink the roles they could play in a new energy landscape and define strategic industrial policies accordingly.

Our research3 shows how successful industrial policies must reflect a country’s potential value chain positioning in future green hydrogen markets and elucidates macro geopolitical trends that could reshape international relations as countries compete for industrial leadership, market shares, and opportunities for job creation.

Country Groups

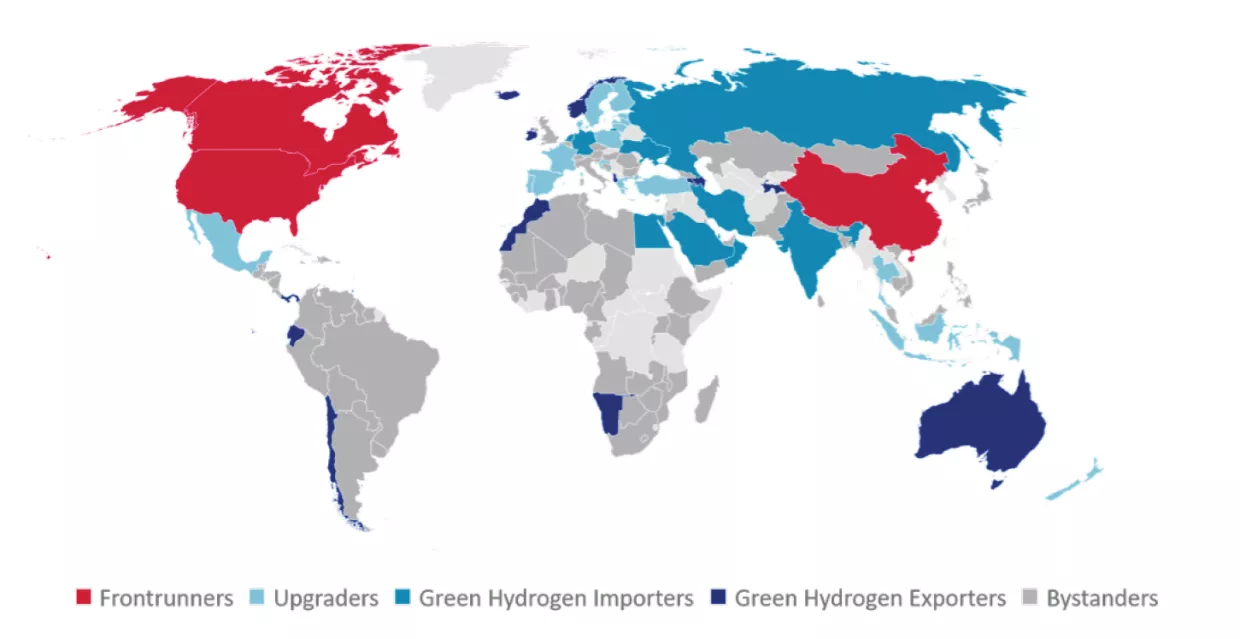

Focusing on three key industrial applications—ammonia, methanol, and steel production, which today account for about 41% of global hydrogen demand and which are expected to increase their shares due to global decarbonization efforts (IRENA, 2022)—we identify five country groups based on the three key variables of resource endowment, current positioning in hydrogen markets, and economic relatedness.4

While individual countries in each group face unique challenges and opportunities, nascent dynamics between these groups could spur a green race for industrial leadership impacting international relations.

Frontrunners. Countries with vast resource endowments and considerable market shares in today’s hydrogen industrial applications could evolve into frontrunners by integrating the green hydrogen value chain segments of production and industrial applications. Potential frontrunners should focus on industrial policies that foster upscaling along value chains.

Upgraders. Countries with adequate resources for green hydrogen production and highly related economic activities could upgrade their value chain position and attract green hydrogen-based industries. Potential upgraders could benefit from strategic partnerships with frontrunners to foster technological and knowledge transfer. Policies should focus on attracting foreign capital—for example, by lowering market risk, developing public-private partnerships, and forming joint ventures.

Green hydrogen exporters. Resource-rich countries without upgrading potential should prioritize green hydrogen exports and would benefit from partnerships with green hydrogen importers to deploy enabling infrastructure and reduce market risk. Furthermore, coordination on international standards for green hydrogen production and use could avoid conflict and facilitate trade at a global scale.

Green hydrogen importers. Resource-constrained countries with hydrogen-based industrial applications must develop strategic partnerships to ensure secure and stable green hydrogen supplies. Furthermore, stimulating innovation and knowledge creation through targeted policies will be critical to sustaining competitiveness during the transition to a low-carbon economy and avoiding industrial relocation to frontrunners or upgraders.

Bystanders. Countries with significant constraints along all mentioned three key variables of resource endowment, current positioning in hydrogen markets, and economic relatedness should assess the techno-economic feasibility of removing some of these limitations. Figure 1 depicts the overall geopolitical and market potential for green hydrogen industrial applications.