This post follows up on “What Determines When a Recession is a Recession?” which pointed out some drawbacks of defining a recession by two negative quarters of growth.

In some countries, there is another, more fundamental, basis for questioning the two-quarter rule for determining recession or any GDP-based rule. Some countries experience sharp slowdowns or periods of diminished economic activity and yet their long-term trend growth rates are either so high or so low that the negative-growth rule does not capture what is needed to describe the cyclical state of the economy. For such countries, the problem is that perhaps there is nothing special about the number zero. This is particularly true for the global economy considered as a whole.

Consider first a country where the rule would yield excessively frequent “recessions.” In Japan, the population is shrinking and productivity growth is far below what it used to be, so the country’s output growth has averaged only 1% per year in recent decades. As a result, even small fluctuations can turn GDP growth negative. The two-quarter rule would suggest that Japan had seven recessions between 1993 and 2015, or once every three to four years. Perhaps this is why the Japanese government does not follow the rule but rather, like the NBER, looks at a wider variety of indicators to determine recessions.

Now consider the opposite problem, when the two-quarter rule yields infrequent recessions. Australia is said to have had the world-record for the length of its recent expansion, at 28 years. To be sure, Australia has earned much of its success. Still, one reason why Australia’s GDP showed no downturns in the past 28 years is that the country’s labor force grew substantially faster than those in other advanced economies, especially in Europe and East Asia.

Similarly, China has not had an outright recession in 26 years (since 1993). The reason, of course, is that its trend growth rate has been high, owing to rapid growth in labor productivity. Chinese growth slowed sharply in the Great Recession of 2008-09 but did not turn negative. GDP did fall sharply when the coronavirus hit in the first quarter, but if the level of GDP rises even a little off the floor in the current quarter, China will not meet the technical definition of a recession even now.

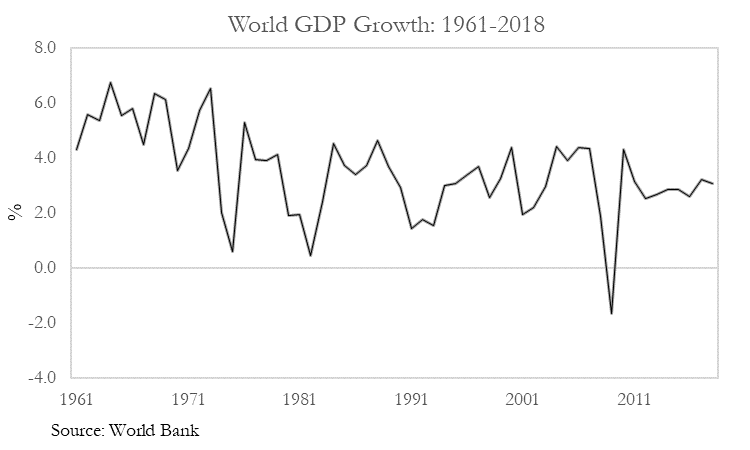

This problem arises when seeking a definition of a global recession. If negative GDP growth is the criterion, then global recessions are very rare, as a result of high trend growth among the average of EM and developing countries. (To be sure, global growth went negative in 2009. See chart.) For this reason, the IMF and other observers tend to adopt other less strict rules-of-thumb for calling a global recession, such as global GDP growth below 2 ½ % or negative growth in GDP per capita. But there is no consensus.

I presented thoughts about the 2-quarter rule versus the NBER approach last October, at a Seminar on Business Cycle Dating, CIDE & INEGI. My ½-hour video presentation and notes were titled “Why do we need a Business Cycle Dating Committee?”

{kind=link}