3.8. Engineering Assessments of Cost Reduction Potential

We have assessed the potential for cost reductions based on engineering fundamentals. This is intended to provide a “reality check” on the cost trends modelling presented above. We have not carried out any engineering modelling for this work.

The potential for cost reduction is influenced by various factors, which sometimes work in opposite directions. The potential to reduce costs appears to be large, due to the early stages of the technology’s development. In contrast, there are physical fundamentals that make large cost reduction more difficult. In particular, the low concentration of CO2 in the atmosphere inevitably requires large volumes of air to be moved and treated (see Introduction), with correspondingly large requirements for energy and materials.

We nevertheless find many areas in which substantial cost reductions appear possible. The mix of costs, and the potential for different types of reduction, are likely to vary greatly with location and technology. The main costs of the capture unit, with indicative shares of costs for the capture plant, are:

- the capital cost of the capture plant, including construction costs and land acquisition (63%);

- energy costs (24%);

- other operating costs, of which the cost of sorbents is the largest component (13%); and

- CO2 transport and storage costs, which may also be large, depending on location.

Correspondingly, we find potential for cost reduction in each of these areas.

Lower construction costs. There may be substantial opportunities, for example in standardizing unit design.

Reduced cost of capital. As technologies mature and risks correspondingly decline, required rates of return will decrease. This could, illustratively, lower project costs by approximately 9%. Opportunities for lower cost of capital may depend on the type of policy support available (see next section).

Improved reliability reducing unit capital costs. As the technology matures it is likely to become more reliable. This should enable increased load factors and thus lower unit costs.

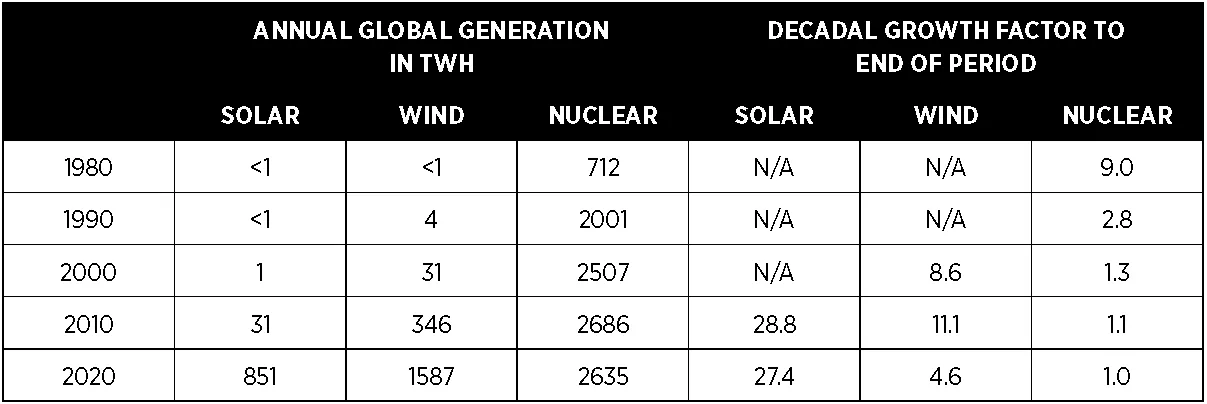

Reductions in costs of low-carbon energy. In practice, energy supply for DACCS is likely to be mainly solar and wind, where costs are expected to continue to fall as more widespread deployment continues. While some projects may rely on fossil fuels with CCS for their energy supply, this is likely to be too costly in most locations. Nuclear may also be too costly, though it may provide good opportunities for matching supply with baseload demand (see below), and there may be the potential for greater efficiency from the use of waste heat from the nuclear plant.

This does not imply that costs of low-carbon energy will necessarily be lower than costs of high-carbon energy, especially when costs of managing variable production of renewables are taken into account. However, the use of high-carbon energy sources greatly reduces the amount of net removals. Consequently, net costs per tonne of removals will usually be lower if low-carbon energy is used, even if the high-carbon energy is cheaper.

In the short to medium term there may be opportunities to use waste heat from industrial plants, although such opportunities may decline as industrial processes decarbonize.

Longer lifetime and improved performance of sorbents. There also appear to be opportunities to reduce capital costs by increasing the recovery ability of the sorbent, which reduces the required size of the capture unit. This may increase costs of the sorbent in the short term but the capex reduction is likely to be the more significant over time. In the case of liquid sorbents, development in processes should keep disposal costs low, and reduce fugitive emissions when they are in service. These materials should also require less energy to regenerate.

Lower costs of other utilities such as water may be important in some cases.

Access to low-cost CO2 transportation and geological storage. Cost reductions may come from siting DAC facilities close to storage locations, where both transport and storage costs are low. Lower costs may be achieved by economies of scale from existing CCS. While the overall technical capacity for storing CO2 underground worldwide is estimated to be vast, detailed site characterization and assessment are still needed in many regions. An operating CO2 storage site can take three to ten years to develop from project conception to CO2 injection. This could become a bottleneck for DACCS deployment (and wider CCS deployment) without accelerated efforts to identify and develop CO2 storage sites.

Improved efficiency by optimizing for local conditions. There may be opportunities for increasing average efficiency of the capture unit by managing directly the humidity and temperature of the incoming air. Cool air is preferable, as adsorption or absorption in general increases with decreasing temperature. Dry air will tend to be better for solid adsorbent systems. Less water is present to compete with CO2 for removal, which means less solid material is required, and hence smaller equipment can be used, reducing the capital and operating costs. In the case of a humid climate, it may be advantageous to either have a dehumidification system, or to make the solid material hydrophobic (so not adsorbing water) to help lessen the effects of humidity. This may not be an issue for liquid systems.

Improvements in overall process integration can reduce a range of costs, including both capital and energy costs. An area of particular importance may be in the integration of power supply and the capture plant (see below). Low-cost energy can also enable changes to design which substitute energy for capital, which may also reduce total costs.

Scale can also bring a range of costs down. Larger-scale plants should have lower unit costs, and development of multiple projects should lead to cost reductions, including through increased availability of standardized products as the industry grows.

3.8.1. Reductions in Energy Costs

There are potential gains in more effectively managing the differences in patterns between energy supply (variable) and patterns of energy use (largely constant). This could include increasing storage, especially as the costs of diurnal storage reduce. It could also include active management of the load across the day, and across longer timescales. It could also include better integration with the wider electricity grid. Seasonal variations may be more challenging to manage.

In any case, it will not be appropriate to treat energy costs as a simple $/kWh based on the prevailing Levelized Cost of Electricity from a solar PV array. It is often not clear how existing cost modelling in the literature addresses this issue.

4. Policy Support to Finance DACCS

DACCS will require substantial policy support. Required support includes establishing adequate regulatory frameworks for DACCS. In particular, monitoring, reporting, and verification (MRV) processes will be required, for example to measure the amount of CO2 stored. Regulatory frameworks will need to extend to reliable certification of removals.

Policy support will also be needed to meet the substantial costs of DACCS, which are not currently funded by commercial markets. Voluntary markets for carbon removal may play some role. However, they are unlikely to be anywhere near enough to achieve full commercialisation of DACCS. The high unit costs of DACCS and the large absolute sums required imply that use of compliance markets and other regulatory approaches will be necessary. This may include inclusion of removals in emissions trading systems.

Financial support for DACCS projects could be provided by a range of regulatory mechanisms, which may be used in combination. The choice will depend on the circumstances of the project and the jurisdiction.

Funding need not necessarily come ultimately from governments. It may, at least in part, come from hard to abate sectors, for example long haul aviation. These sectors may eventually require permanent net removals to balance their emissions. They could be obliged by regulation to purchase the necessary removals. This would be consistent with the Polluter Pays Principle. However, overall “netnegative” emissions, with removals of past emissions to reduce atmospheric concentrations, will likely require funding from governments.

Policy support will need to be sustained over decades, because this is the amount of time needed for scale-up. This is likely to be especially challenging as DACCS does not produce a product that has value beyond its benefits for the global climate. Products made from CO2 that keep the CO2 permanently out of the atmosphere are likely to provide only small markets globally compared with volumes captured. In contrast, products of other low-carbon technologies have wider value. For example, electricity from low-carbon power generation earns income from electricity sales, and has benefits for energy independence. Similarly, energy efficiency measures can reduce costs.

In this section we briefly review how policy may enable financing of the substantial costs identified in the previous two sections. Appropriate choices of policy instruments can help reduce costs and accelerate deployment. There are few examples of financial support for DACCS to date, although some are beginning to emerge. However, insights can be gained from considering policy support for CCS and other low carbon technologies.

4.1. Designing Policy Support

DACCS is capital-intensive, implying that support will be particularly valuable if it reduces:

- total capital costs; or

- required rates of return (cost of capital), and thus levelized costs of removals.

4.1.1. Capital Grants and Other Capital Subsidies

Total capital costs to project developers may be reduced by capital grants. These may be provided in cash, or in other ways, such as access to land for projects at preferential rates. In the United States, Canada, and elsewhere, capital support may be in the form of investment tax credits. Low-cost loans can provide similar benefits by reducing the weighted average cost of capital, and thus total costs.

A potential weakness of these forms of support is that they give little or no incentive on their own for the operation of the capture project. Consequently, capital subsidies may often be used in combination with other forms of support. This may include operating costs subsidies.

The role of subsidies for CCS is illustrated by Norway’s Longship project, which is currently under construction. The Norwegian State will pay around three quarters of the costs of the project. This support will run for the first 10 years. The State also takes a large proportion of the risk of cost overrun up to specified limits. In broad terms, for capital costs it takes 80% of overrun costs for Northern Lights, which is the transport and storage part of the project, and 83% for the capture plant. For operating costs over the first 10 years, it takes 75% of the costs of overruns for transport and storage and also 75% for the capture plant.

Investment and production and tax credits can also provide substantial subsidies. In the United States, the Inflation Reduction Act has expanded and enhanced the existing 45Q tax credits to $85/tCO2 for CCS, with new provision for DAC, including a higher incentive level at $180/tCO2 for storage in saline formation. For DAC facilities, it decreases the CO2 capture requirements from 100,000 tonnes captured per year to 1,000 tonnes per year, implying smaller demonstration projects can benefit.

In addition, the Investment and Jobs Act (signed into law in November 2021) includes funding of $3.5 billion to establish four large-scale DAC hubs and related transport and storage infrastructure. This is the largest commitment any jurisdiction has made to DAC so far.

Recently the Department of Energy has announced funding for two large scale DACCS projects, which appears to be in the form of direct subsidy.

Projects can also benefit in some cases from tradable credits under the California Low Carbon Fuel Standard, providing the DAC project meets the requirements of the Carbon Capture and Sequestration Protocol. These may be combined with tax credits and other forms of support to make a package that will enable projects to proceed.

4.1.2. Payments Under Contracts

Contracts that provide a payment per net tonne of CO2 removed from the atmosphere and permanently stored are likely to be an effective way of incentivising construction and operation of DACCS plant. Basing payments on net tonnes removed from the atmosphere aligns financial rewards to the project with the project’s climate benefits.

Contracts between the project and an appropriate counterparty, such as a government backed company or agency, can reduce project risks and thus cost of capital. This reduction in risks is likely to be especially marked if the payments are made under a private law contract, rather than as discretionary government payments, because it reduces the risk of unexpected reductions in payments due to changes in policy.

For example, in the UK, a company owned by government (the Low Carbon Contracts Company, LCCC), is the counterparty for contracts (CfDs) with renewable energy projects, and makes and receives payments under the contracts. Electricity suppliers are required by regulation to fund the CfD payments made by LCCC to generators through the CfD Supplier Obligation Levy. Studies have indicated that this approach to funding has created significant benefits when used to support offshore wind power.

DACCS is capital-intensive, so reductions in the cost of capital can have a significant effect on total costs. Illustratively, each one percentage point reduction in cost of capital due to the type of support available can reduce total cost per tonne of removals by approximately 5%.

The UK is in the process of negotiating contracts to support industrial carbon capture. Contracts will include separate capital cost and operating cost payments. The capital remuneration component is planned to run for five years, consistent with the short paybacks required by industry. The opex remuneration component runs 10-15 years. For early projects, payments will not vary with the actual market price for carbon, which is set by under the UK Emissions Trading System (UK ETS). However, it is intended that this will change for subsequent rounds of projects, with payments varying with the carbon price under a contract for difference (see below).

4.1.3. Contracts for Difference

Contracts for difference (CfDs) may be appropriate if a market price of removals develops. Under a CfD, a payment is typically made for the difference between a market price, for example for electricity or carbon, and a pre-determined price, the strike price. This essentially fixes the price the project receives. If a project can earn revenue from the sale of carbon dioxide removal certificates, then subsidy payments can be reduced accordingly under the CfD, and the project can remain profitable.

For example, if certified removals from DACCS projects can be sold in an emissions trading system, they will earn revenue that depends on the prevailing carbon price. The higher the price, the lower the required subsidy. In such circumstances, support may then be set under a CfD on the carbon price (Carbon CfD, or CCfD), with subsidy decreasing as the carbon price rises. Such mechanisms are also currently under discussion elsewhere, for example for the EU’s Innovation Fund.

4.1.4. The Importance of Competition for Funding

The level of contract payments can likely be reduced by the use of competition to award contract-based funding. Competition for contractual support has been important in driving down prices paid for renewable energy and other low carbon technologies. Competition is likely to be in the form of an auction for contracts, or some form of competitive tender.

Separate allocations may apply to different technologies, with different amounts of support. This has been common in renewables, for example with different allocations for onshore wind and solar. This helps ensure that a variety of technologies with different characteristics are supported.

The Dutch SDE++ mechanism provides an example of such support for CCS. Under this system support is awarded to CCS as a contractual payment per tonne of CO2 stored. Contracts are awarded by auction, with support awarded to the lowest cost per tonne. There are parallel auctions for different types of project, for example renewable electricity and CCS.

4.1.5. A Regulated Asset Base (RAB)

Under a Regulated Asset Base approach, costs are recovered by charges to customers for the service provided. Typically, a regulator awards a company a licence to charge a regulated price to consumers in exchange for the company providing essential infrastructure. This enables investors to share some of the project’s construction and operating risks with consumers, helping to lower the cost of capital.

Such approaches are used for various types of infrastructure, including natural gas and electricity networks.

Under such an approach is may be more difficult to maintain competition between projects, so risking higher costs. It is also more difficult for the regulator to assess costs for an industry with rapid innovation, such as DACCS, than for more wellestablished industries, such as natural gas networks.

We do not expect a RAB model to be used for DACCS value chains as a whole, except perhaps in the long term. However, it may play a role in providing transport and storage networks.

4.2. Creating a Market for Removals

In the medium and longer term, removals could become a traded commodity, with projects earning revenue from removals markets. This may happen through an ETS modified to include removals, with any emissions requiring surrender of either an emissions allowance or a certified tonne of net removals. Alternatively, jurisdictions may adopt arrangements where there are obligations on remaining emitters to balance any emissions with removals, but without creating a full ETS.

Eventually, caps under emissions trading systems will need to be set to zero, consistent with net zero commitments. This will require the total volume of remaining emissions to be matched by removals. The price and volume of removals should, in principle, then be driven by demand from hard to abate sectors, with removals preferred where they are cheaper than abatement.

Variants of such approaches are possible. For example, an exchange rate might be introduced where more than one tonne of removals is required to balance a tonne of emissions, in order to recognise uncertainties and risks. Also, governments may act as intermediaries, rather than emitters and owners of removal certificates trading directly.

The UK government has recently concluded that the UK Emissions Trading System (UK ETS) is an appropriate long-term market for greenhouse gas removals. It intends to include engineered GGRs in the UK ETS, subject to further consultation, a robust MRV regime being in place, and management of wider impacts.

Inclusion of removals in an ETS seems likely eventually to be favoured in the EU. Incorporation of removals in the EU Emissions Trading System is already being discussed. However, adoption of such measures in the EU appears likely only in the longer term, for example in the mid-to-late 2030s and beyond. This in part reflects concerns about the effects of early inclusion of removals, in particular that they may weaken incentives for emissions reductions (mitigation deterrence).

Where no ETS is in place, demand for removals may be created by other forms of regulation. For example, governments may require emitters or emitting sectors to buy a specified quantity of certified removals.

In the longer term, there may be additional demand for removals from governments or other entities with obligations to achieve net-negative emissions. This could, for example, be in the form of tenders for defined quantities of removals.

4.3. The Potential Role of Revenue from EOR

T hecosts of DACCS can be mitigated if captured CO2 is used for Enhanced Oil Recovery (EOR) and the project benefits from the resulting revenue stream. This may reduce or eliminate the benefits of DACCS for the climate if it results in extra oil being burned. This could be reflected in reductions in the number of any certified removals credits earned. However, use of EOR revenues it may also reduce required policy support and thus aid in the early development of the technology.

One project developer, Occidental Petroleum (Oxy), is promoting the idea of “carbon neutral oil.” At present this appears to be mainly bundling offsets with oil. However, there are reported to be plans to develop DACCS to provide physical carbon neutrality, where the additional CO2 released from the combustion of additional oil recovered matches the net amount of CO2 captured by DACCS. This may include EOR associated with its capture plant currently under construction.

We estimate that approximately 1.6 additional barrels of oil production would create emissions equal to one tonne net of DACCS, allowing for emissions from the refining process. At an illustrative price of $80/bbl, this would produce $128 of revenue for each tonne of DACCS. If the oil were to obtain a premium price, for example because it helped meet corporate carbon neutrality goals, it could create greater value for projects. However, in doing so it may forego revenue from generating net removals, as these removals may not qualify for credits under a certification regime if oil from EOR is included in the certification lifecycle analysis.

5. Concluding Remarks

Based on the analysis presented in this paper we derive the following conclusions.

Potential scale

DACCS remains at an early stage of deployment and realising its full potential will take many decades.

By 2050, DACCS appears likely to achieve removals equivalent to at most about 1% of current emissions of fossil carbon from energy and industry, and likely significantly less than this. It will thus make at most only a small contribution to meeting 2050 net zero targets. Even by 2060 it will be challenging, and perhaps impractical, to get to net removals from DACCS as large as 1-3% of current global emissions. Among other things this illustrates the importance of focussing on emissions reduction wherever possible.

There appear to be few fundamental limits on the scale of total operating DACCS capacity, although it requires large-scale physical resources, especially energy. Consequently, DACCS may have a major potential role in the second half of the century, including in achieving net negative emissions.

To be effective, DACCS requires energy used to be low-carbon. This implies either dedicated low-carbon power, or a fully decarbonised electricity grid, and the means to produce low-carbon heat.

The earlier scale-up begins, the earlier benefits of DACCS will be realised. However, projections of the mix of removals employed over the coming decades inevitably remain highly speculative.

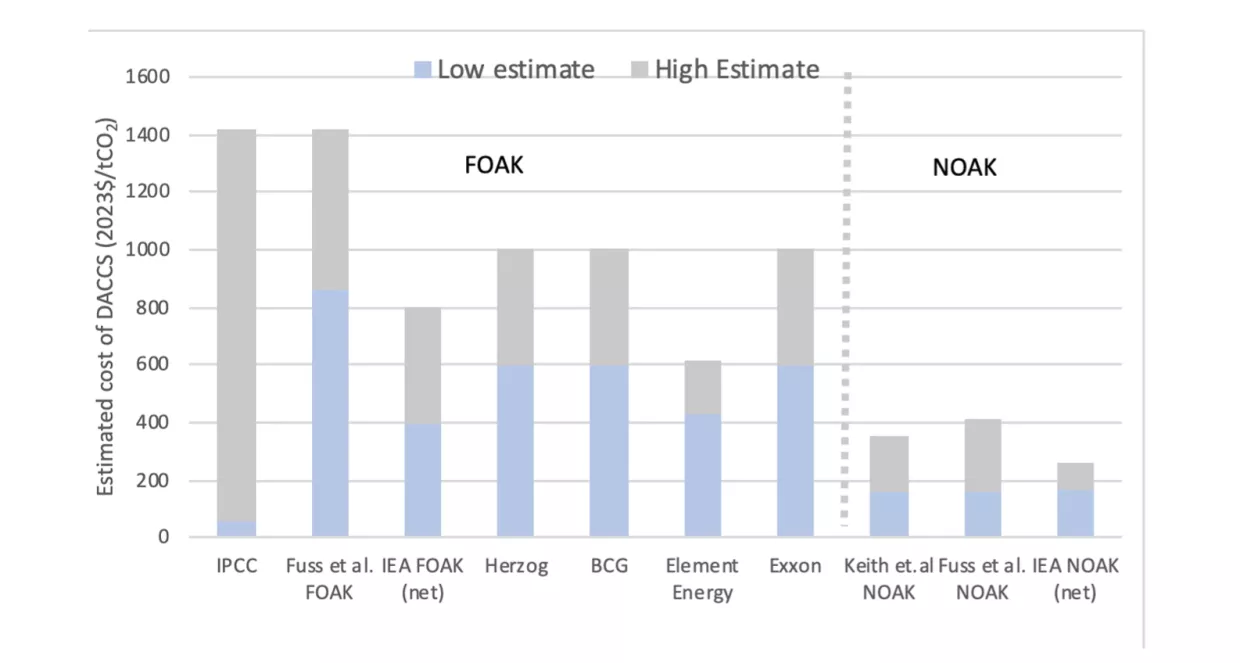

Costs

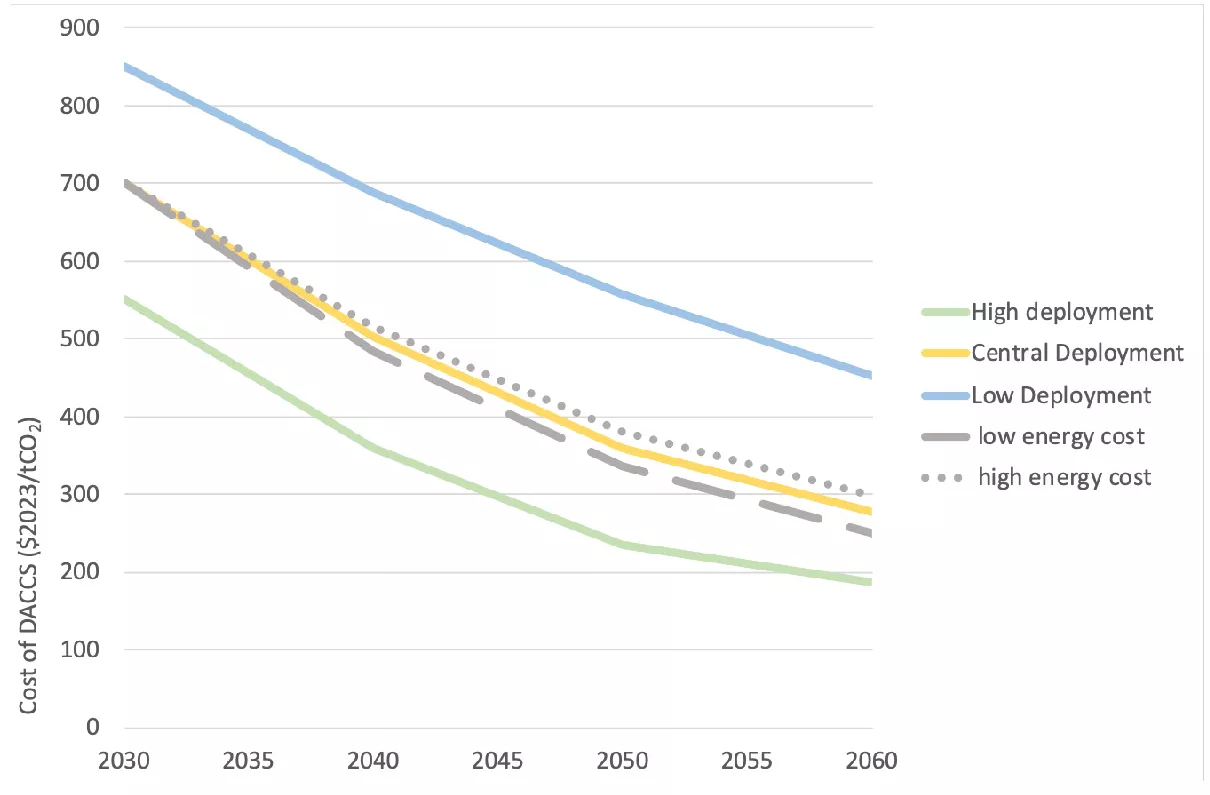

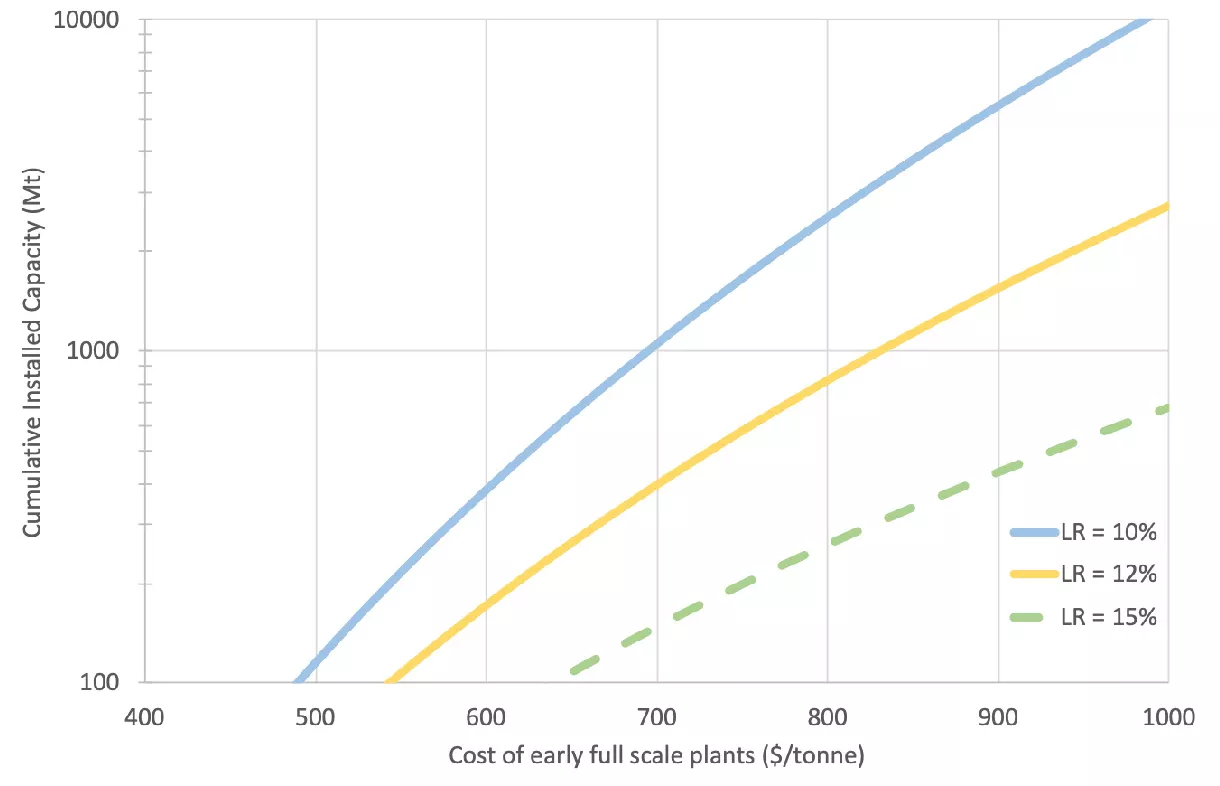

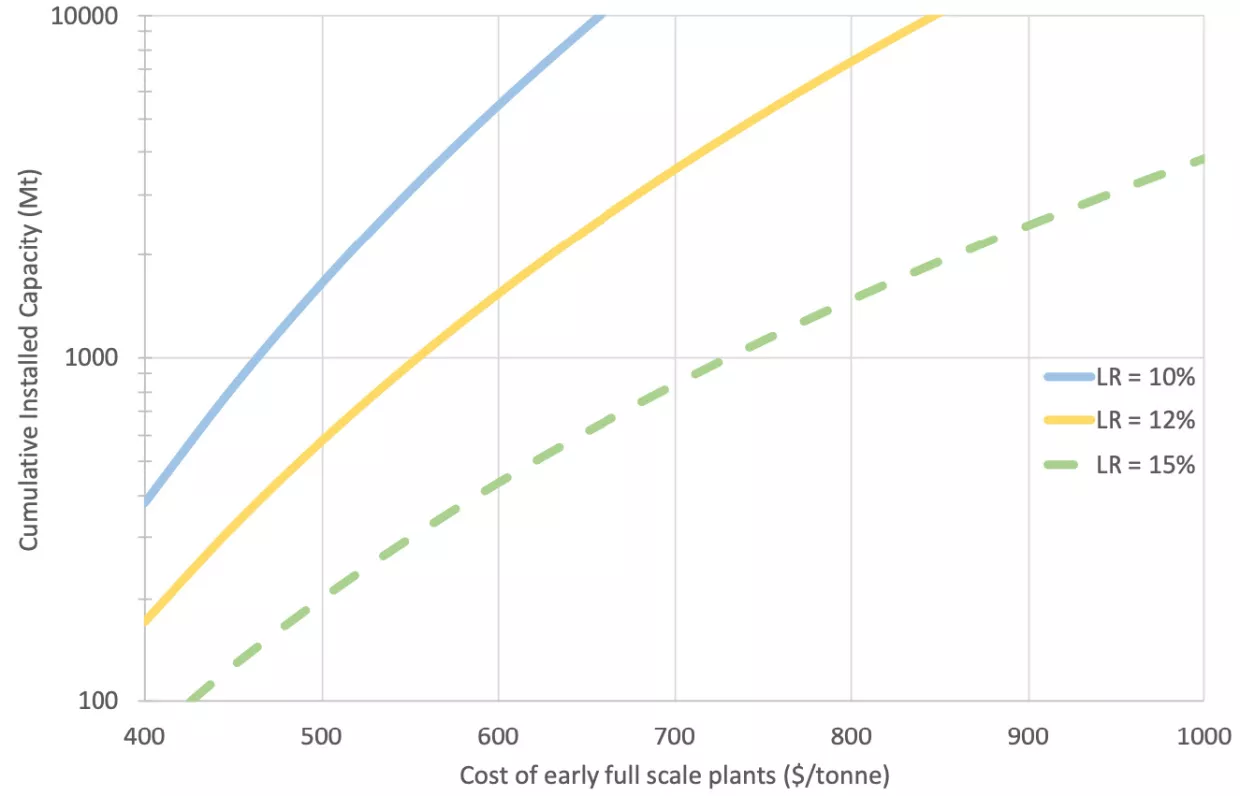

- We estimate that the costs of full-scale DACCS will likely be about $400-1000/tCO2 around the end of this decade, where tonnes are net tonnes permanently removed from the atmosphere. This total includes transport and storage costs.

- Costs will fall with deployment. Costs may fall to around $200-400/tCO2 sometime in the 2050s if large scale deployment is successful. However, the lower part of this range will only be achieved if costs of early plants are close to the bottom end of the currently estimated range of $400-1000/tCO2, there is rapid large-scale deployment of DACCS, and learning rates are moderate to high.

- Aspirational targets of $100/tCO2 seem unlikely to be reached even by 2060.

- Costs of $400/tCO2 may nevertheless be below the marginal cost of abatement in some sectors and applications. This could give DACCS a valuable role in meeting net zero goals at lower cost.

Funding

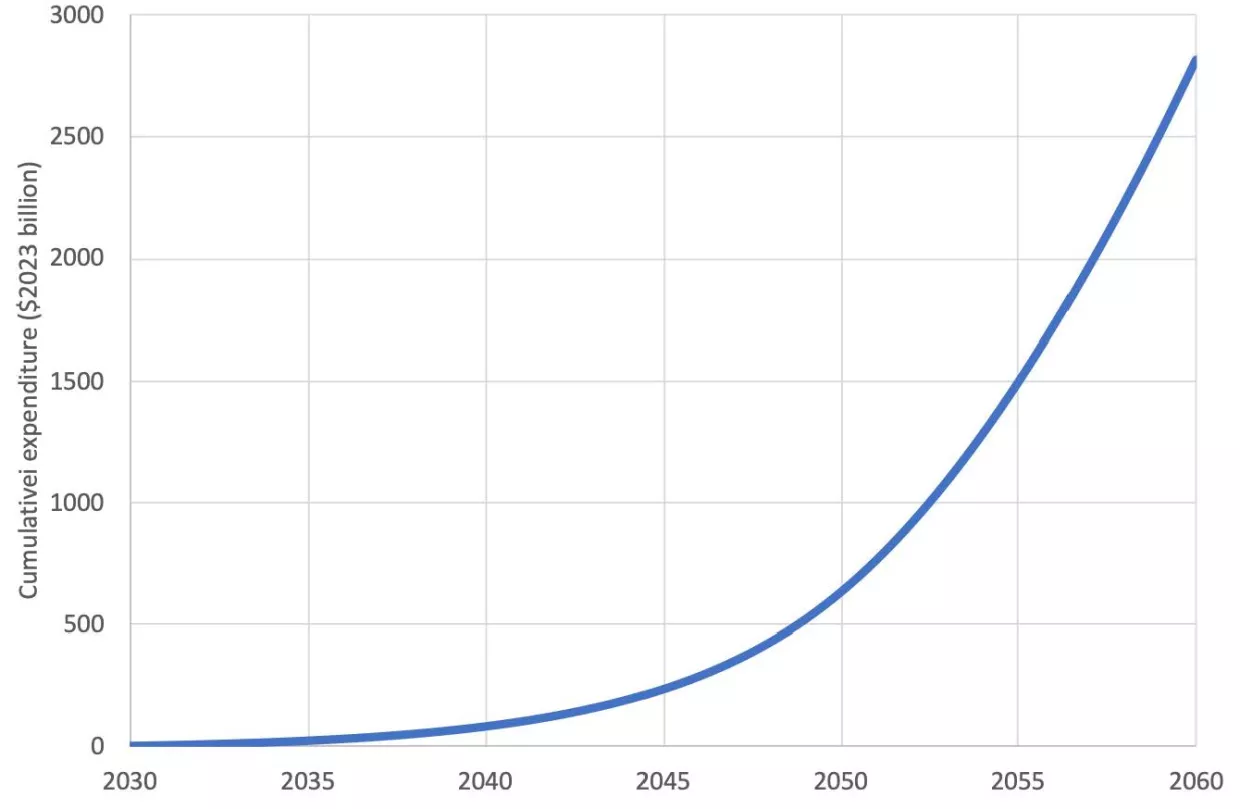

- Reaching Gigatonne scale of removals using DACCS will likely require cumulative expenditure into the trillions of dollars.

- The high costs of DACCS derive in large part from CO2 being very dilute in the atmosphere. It will usually be cheaper to capture emissions from more concentrated sources such as industrial plants, or to switch to low-carbon electricity or other low-carbon energy sources, preventing the CO2 getting into the atmosphere in the first place.

- Among other things the high cost of DACCS favours moving to high capture rates for industrial and power sector CCS projects, to reduce residual emissions which must then be removed. Industrial CCS projects can also help develop the CO2 transport and storage infrastructure necessary for DACCS, which can often have substantial lead times.

Financial and policy support

- There are now emerging instances of policy support for DACCS, including under the Investment and Jobs Act and the Inflation Reduction Act in the United States.

- Current high per tonne and total costs of DACCS, and lack of corresponding demand for removals, implies that strong financial and policy support will be required for initial deployment, including large subsidies for projects.

- Possible sources of funding include governments with a strong strategic interest in removals, including those wishing to sustain some level of oil and gas production, and those with strong negative emissions reductions commitments.

- Funding may also be made available from industries which may require permanent removals into the longer term, for example aviation. This would be in line with the Polluter Pays Principle.

- In most jurisdictions optimal policy support is likely to be a mixture of capital grants, tax credits, and contractual payments per tonne of net removal.

- The use of competitions or auctions to award funding has the potential to reduce costs in some instances.