Abstract

There is growing recognition of the relative importance of anthropogenic emissions of methane as a contributor to global climate change. An important source of such emissions in some countries, including the United States, is the oil and gas (O&G) sector. This points to the importance of developing understanding of the marginal abatement cost functions for methane emissions reductions. Scholars have employed a diverse set of methodologies to estimate abatement costs, including engineering cost models, econometric analysis of natural gas markets, and statistical retrospective analysis of state-level regulation. We critically summarize these approaches and synthesize their results. We find significant potential for low-cost methane abatement in the O&G sector in the United States and elsewhere, although claims of widespread negative abatement cost opportunities should be taken with a grain of salt. We also find that the potential for low-cost abatement is not without limit. Whereas it appears that cutting methane emissions in half would be relatively inexpensive, a sharp uptick in marginal abatement cost may occur when reductions exceed 60 to 80 percent below baseline levels. This threshold may change over time with technological advances in remote sensing, which can reduce abatement costs at various levels of ambition.

1. Introduction

One hydrocarbon, methane (CH4), has received much less attention than the principal anthropogenic greenhouse gas (GHG) driving global climate change – carbon dioxide (CO2) – both in academic studies (IPCC 2023) and policy actions (United Nations 2015). This is largely because annual quantities of anthropogenic methane emissions are much less than those of CO2. Methane also has a relatively short atmospheric lifetime, on the order of twelve years, compared with the atmospheric half-life of CO2, which exceeds 100 years.

On the other hand, each molecule of methane has very high global warming potential (GWP) relative to CO2, being twenty-eight times greater over 100 years, and some eighty-four times greater if measured over a 20-year period. Historically, methane is responsible for about 30 percent of the global warming that has occurred since the beginning of the industrial revolution (International Energy Agency 2023).

Methane-emissions abatement can significantly reduce GHG concentrations, warming, and damages, particularly in the short term, which could help give the world time to “bend the curve” on CO2 emissions, conduct research on carbon removal, and, more generally, implement longer-term strategies to mitigate and adapt to climate change. Key sources of anthropogenic methane emissions include: oil and gas (O&G) extraction, transport, and refining; coal beds; landfills; and agriculture (livestock, as well as rice paddies).

The oil and gas sector is a major source of anthropogenic methane emissions in a number of countries, including the United States. Emission estimates for this sector come from government inventories, bottom-up detection and estimation under the U.S. Environmental Protection Agency’s (EPA’s) Greenhouse Gas Reporting Program, and estimates based on aerial and satellite remote-sensing technologies. U.S. EPA (2024a) estimated that U.S. O&G methane emissions represent nearly one-third of overall U.S. methane emissions, and about 3 percent of U.S. GHG emissions (based on a 100-year GWP). As discussed below, the U.S. EPA inventory may underestimate methane emissions (e.g., Alvarez et al. 2018). This sector may also provide opportunities for relatively low-cost emissions abatement.

Knowledge of the marginal costs of abating methane emissions is important for the development of the most efficacious and cost-effective government policies. First, such knowledge can help inform agencies in developing and implementing regulatory standards, such as EPA’s upstream O&G methane regulation (U.S. Environmental Protection Agency 2024c), by enabling effective targeting of emission-reduction strategies and technologies. Second, estimates can inform the anticipated response to emissions fees and taxes, such as the Methane Fee (literally, the “Waste Emissions Charge for Petroleum and Natural Gas Systems”) incorporated in the U.S. Inflation Reduction Act of 2022. Third, knowledge of marginal abatement costs could facilitate estimates of the potential emissions reductions that may be induced by subsidy policies (such as for plugging abandoned wells) and voluntary offset credit mechanisms. Finally, such estimates could inform the costs of complying with trade measures, such as a life-cycle methane emissions standard for liquified natural gas (LNG) exports to the European Union or other methane border adjustment mechanisms (Clausing et al. 2023).

Recent technological advances related to monitoring, measuring, and controlling methane emissions have enabled both private-sector efforts and public policies focused on methane emissions abatement. In this paper, we review and synthesize the academic and gray literatures on the costs of such emissions abatement in the O&G sector, with a focus on the United States.

2. Categories and Existing Estimates of Abatement Costs

We identify three methodological categories for estimating marginal abatement costs. One category is engineering cost estimates, with prominent examples including: the International Energy Agency’s (IEA’s) marginal abatement cost (MAC) curve for methane emissions from fossil fuel operations, covering new processes and equipment, leak detection and repair, vapor recovery units, replacement of leaky equipment, abatement ventilation, and coal mine methane utilization (International Energy Agency 2024); U.S. EPA’s Regulatory Impact Analysis (RIA) for the Supplemental Oil and Gas Sector Methane Regulation (U.S. Environmental Protection Agency 2022); ICF (2014, 2015, 2016) modeling of methane abatement opportunities; and energy-economic modeling (Delhotal 2006). Such engineering-based approaches can inform prospective analyses of proposed policies and actions.

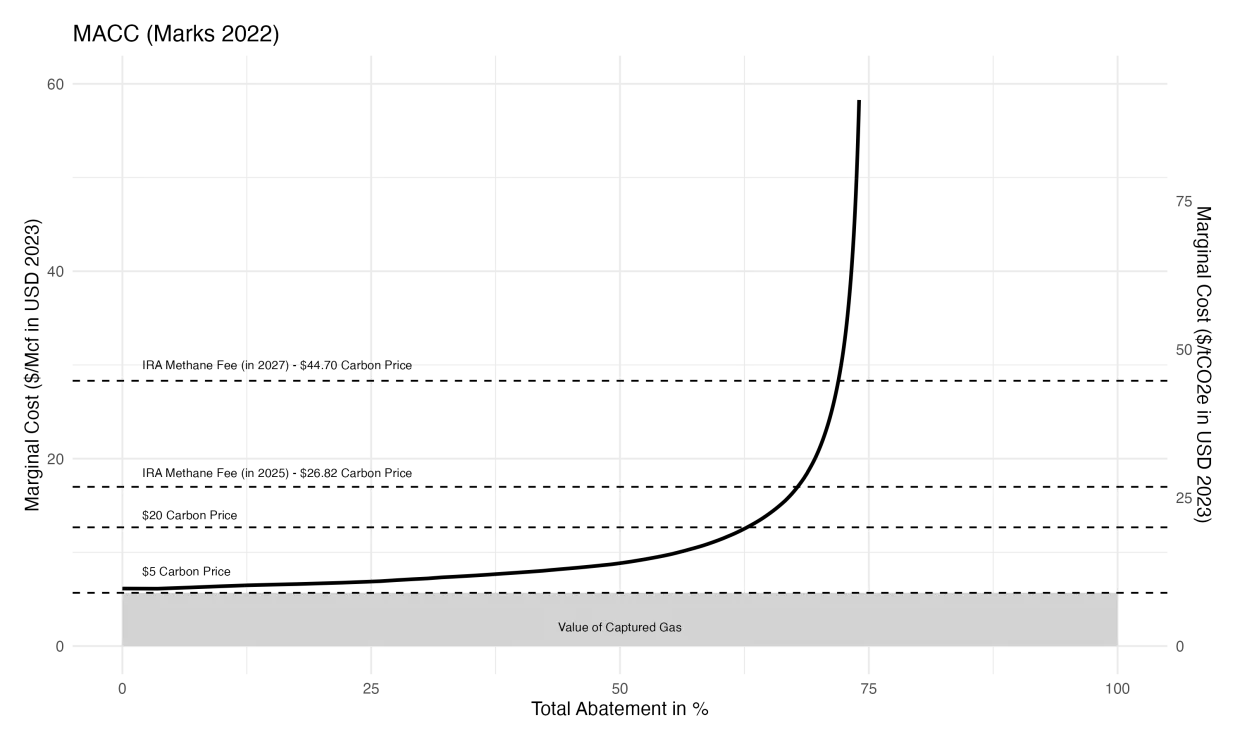

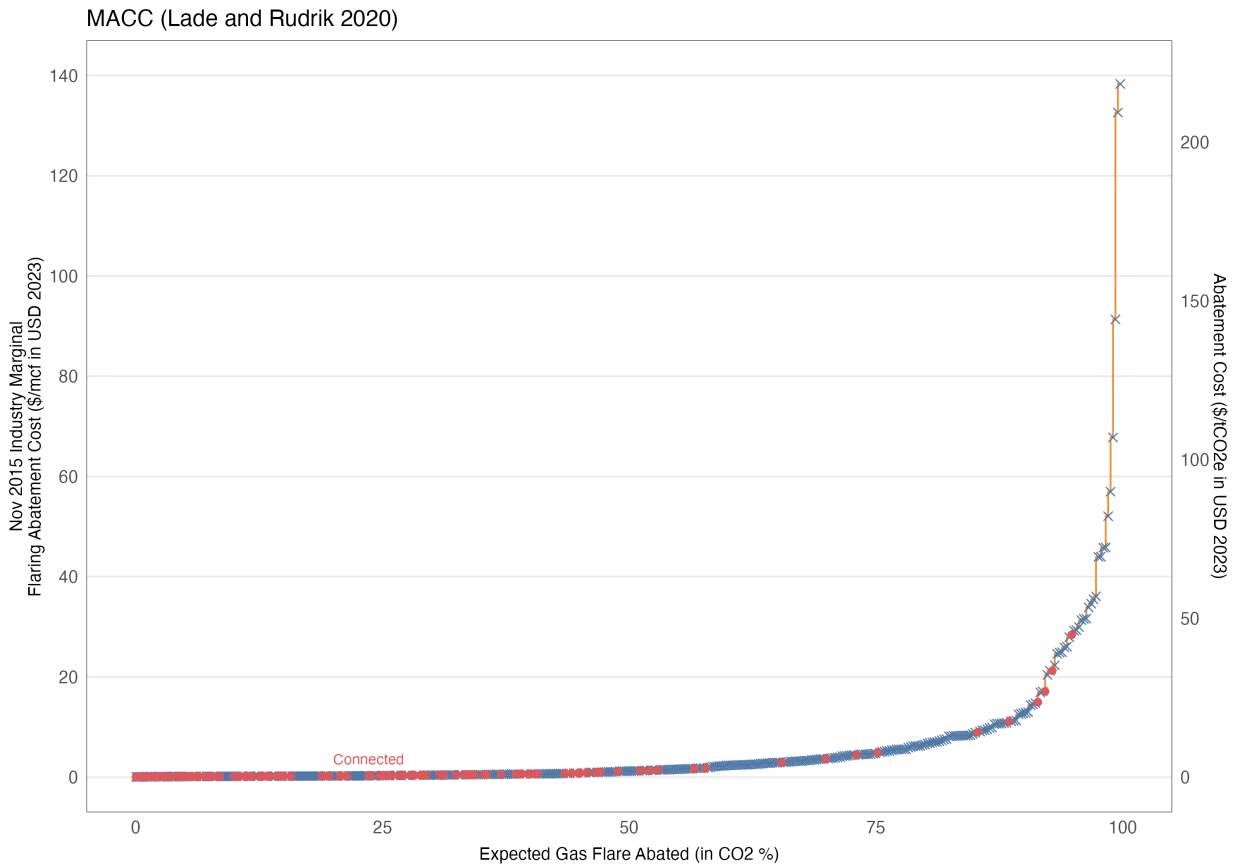

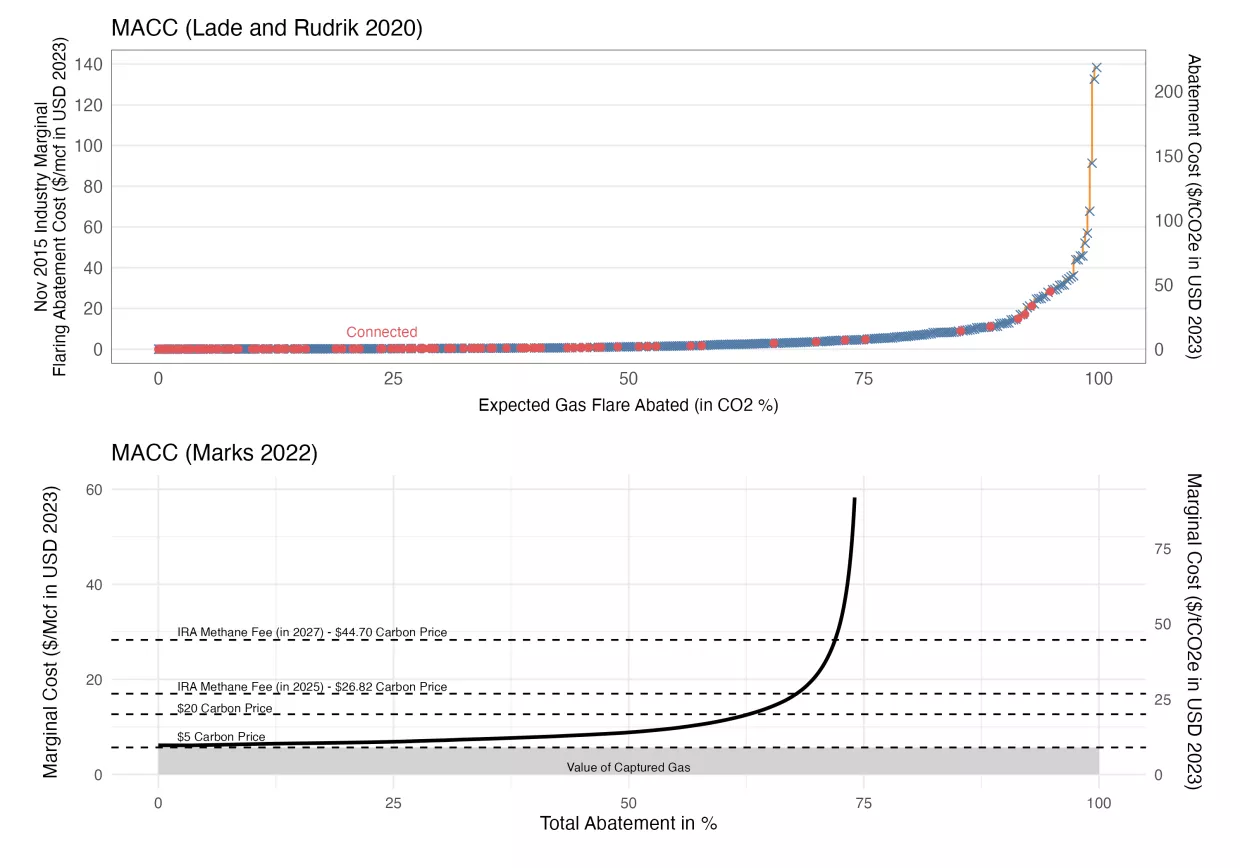

Retrospective analyses of markets and policies can produce estimates of abatement costs in practice. Hence, a second category of methane abatement cost estimates is econometrically estimated measures of costs. These are potentially important because engineering cost estimates may be incomplete, or may fail to fully reflect incentives among private firms to adopt, maintain, and use control technologies. There is an emerging literature that has exploited variation in natural gas prices (Marks 2022), as well as variation in regulations (Lade and Rudik 2020), to estimate abatement costs and emissions abatement associated with O&G extraction.

The third category of potentially useful methane abatement cost estimates consists of costs that may be revealed through implementation of public policies, including various policy instruments intended to reduce methane emissions (White House Office of Domestic Climate Policy 2021). In particular, implementation of subsidies and voluntary programs for methane reductions (U.S. Environmental Protection Agency 2024a), methane regulations (U.S. Environmental Protection Agency 2024c), and the methane fee in the Inflation Reduction Act of 2022 (U.S. Congressional Research Service 2022) could reveal upper bounds of costs of abatement. Such cost estimates can come directly from government or other analyses of these policies.

We carried out a comprehensive search within the above three categories for useful information about methane abatement costs. This search involved four approaches. First, we searched the relevant academic literature in key areas, including economics, political science, and law, as well as general climate change scholarship. Second, we searched for unpublished and other gray literature from the NGO community, private industry, governments, and multinational organizations. Third, we communicated with companies in the O&G sector, offset project developers, and NGO experts. Finally, we reviewed publicly available comments on EPA’s upstream O&G methane rule proposal and the methane fee implementation rule proposal.

In section 3 of the paper, we describe the results of our survey of the literature and other sources by providing brief descriptions of each of the available cost estimates, and summarize the key results. In section 4, we synthesize this information by scaling the available abatement cost functions so that they can be compared in a reasonable fashion. This enables us to portray three principal MAC functions in readily accessible form in common graphical presentations. We also examine the major reasons for the differences among the MAC functions. Finally, in section 5, we conclude with our key findings and their policy and research implications.

3. Abatement Cost Estimates

The costs of abating methane emissions at O&G extraction operations reflect the need to identify the source of emissions, invest in equipment, undertake process changes to reduce emissions, and train staff appropriately for the use and maintenance of new technology. A natural starting point for assessing the costs of various approaches for reducing methane emissions is then to build, from the bottom up, prospective estimates of the costs of these discrete actions. For an operator of an O&G drilling pad, learning the costs of specific interventions to reduce emissions is a natural starting point for how the operator responds to a regulatory performance standard or a methane fee.

A set of very different approaches to assessing the costs of reducing methane emissions is based on top-down, retrospective analysis, such as inferring abatement cost from econometric analysis of variations in natural gas prices and associated emissions responses. Related to this is inferring methane abatement from variations in regulation, gas flaring, and emissions.

3.1. Engineering Cost Estimates

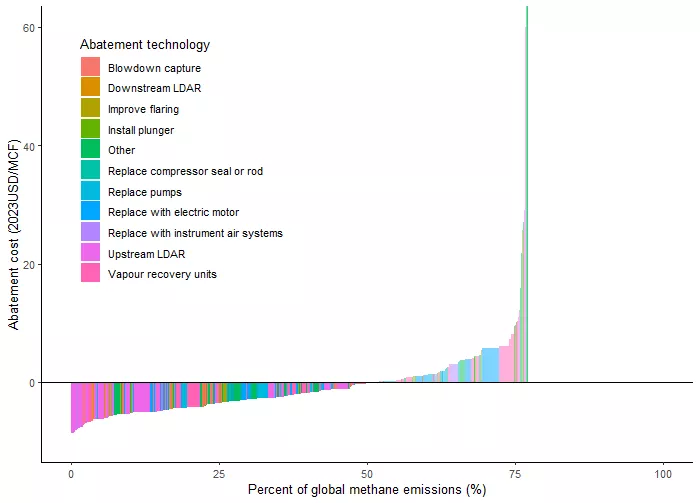

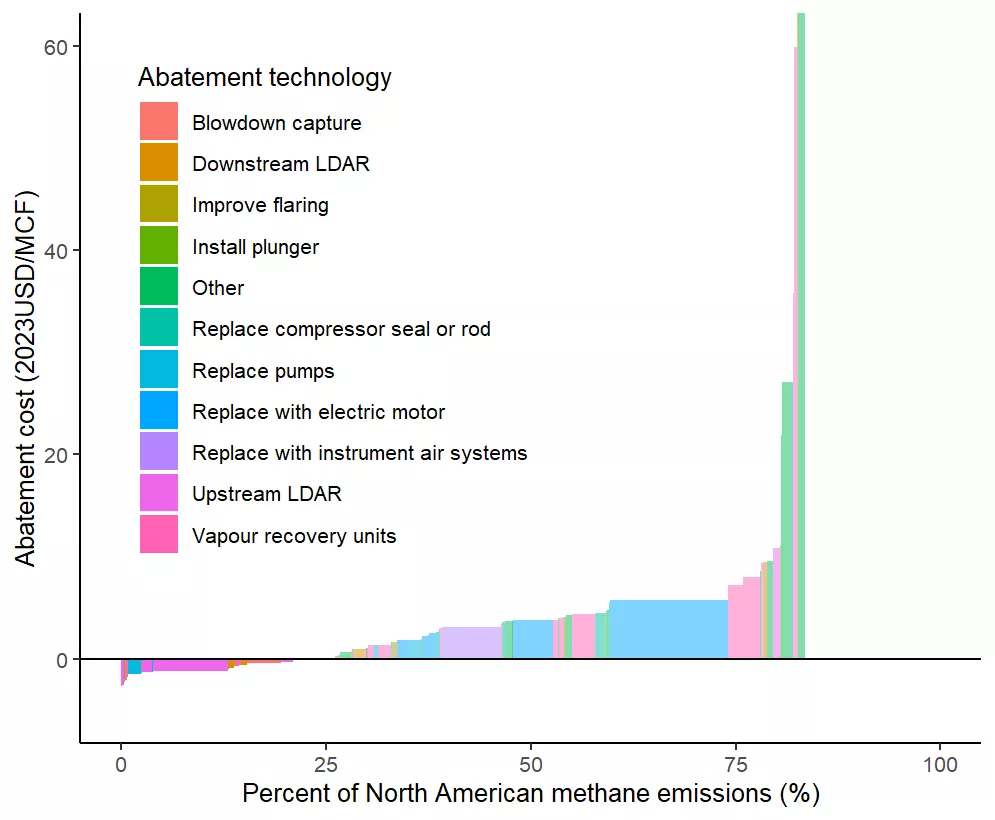

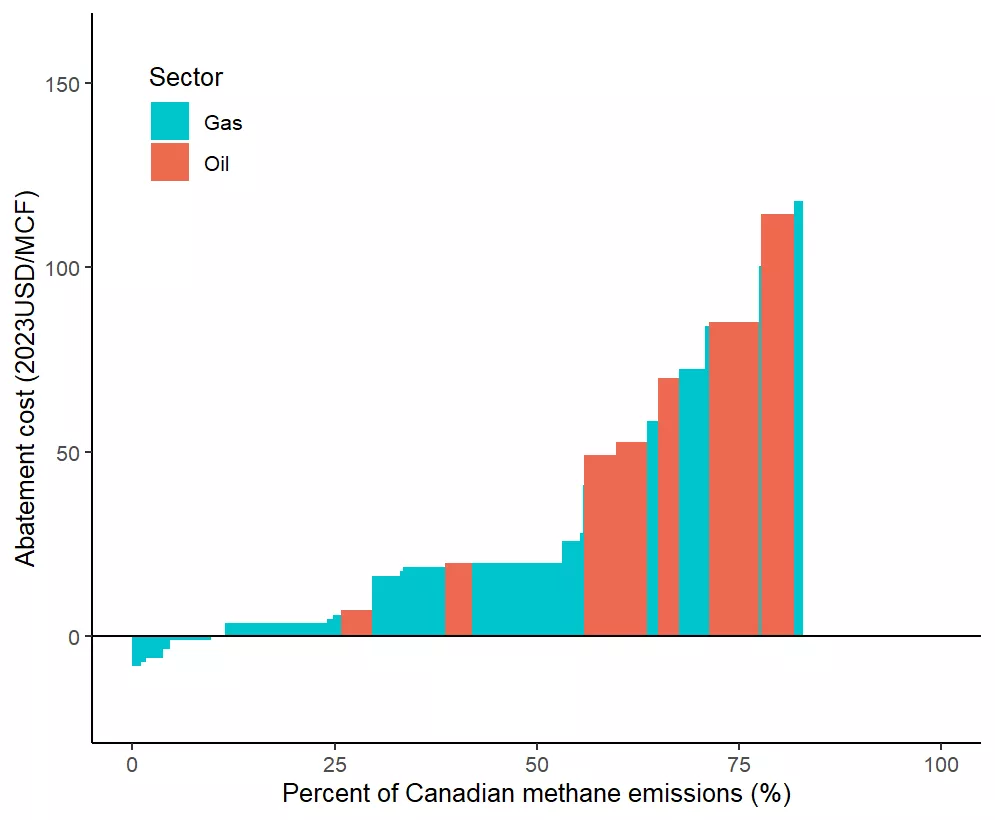

Engineering cost models can identify and depict low-cost to high-cost technology and process options for reducing emissions for a representative operation – a so-called “model plant.” These approaches require knowledge regarding the baseline methane emissions from O&G production activities. For example, the IEA (2024) presents estimated emissions from O&G activities on a global, regional, and, to a limited extent, national basis. IEA constructs these estimates by using U.S.-based methane emissions estimates published in the U.S. EPA Greenhouse Gas Inventory, and produces U.S. emissions intensity measures by hydrocarbon (natural gas, oil), segment of industry (upstream, downstream), production type (onshore, offshore, unconventional, etc.), and emissions type (vented, flared, fugitive), which are then applied to other countries, with country-specific scaling adjustments.

To evaluate the opportunities for reducing these estimated emissions, IEA examines 82 equipment-specific emission sources. They assess various abatement options – replacing equipment, routing captured emissions to a flare or storage tank, or employing leak detection strategies – in terms of their emission-abatement efficacy, capital costs, and operating costs. They produce region, hydrocarbon, and segment-specific abatement cost measures for these abatement options, reflecting the variation in both underlying emissions and technological costs. Many of these abatement cost options appear to be negative when accounting for the value of the captured methane which, in theory, can be sold into natural gas markets.

The net present value for an abatement option reflects the capital costs, operating costs, and revenues associated with selling captured methane at a country-specific well-head natural gas price, using an 8 percent discount rate. The abatement cost for this option then reflects the ratio of this present value to the expected quantity of methane emissions avoided, so in effect the benefit of the activity, that is, the methane emissions avoided, is not discounted.

The IEA arrays these O&G methane abatement options based on their estimated cost per ton through its Methane Tracker (converted into cost per thousand cubic feet, MCF, in Figure 1). IEA (2024) reports that the O&G sector produced about 77 million metric tons of methane in 2023. They posit that slightly more than half of this amount could be abated at no net cost, after accounting for the expected revenue from selling captured methane in gas markets. These cost estimates, however, do not account for the costs of detecting methane emission source in O&G infrastructure. Globally, the IEA analysis suggests that the O&G sector could reduce its emissions 74 percent by employing abatement options with net present value costs no greater than $10/tCO2e.