Marcel Crozet/International Labor Organization via CC BY-NC-ND 2.0

A miner exits a tunnel at a titanium, niobium, and tantalum mine in Lovozero, in the Murmansk region of Russia.

Interest in Arctic rare earth elements (REEs) is growing as melting ice makes previously undiscovered mineral deposits and new shipping routes accessible, and due to increased geopolitical pressures. Driven by national security concerns and the energy transition, Western powers such as the United States, Canada, and the European Union are turning to the Arctic to secure alternative supply chains and reduce their reliance on China. Russia, meanwhile, is focused on building domestic processing capacity to protect itself from Western sanctions.

This explainer provides an overview of where rare earth elements can be found in the Arctic, the opportunities and challenges involved in mining them, and the tensions between geopolitical imperatives, environmental protection, and Indigenous self-determination.

What are rare earth elements?

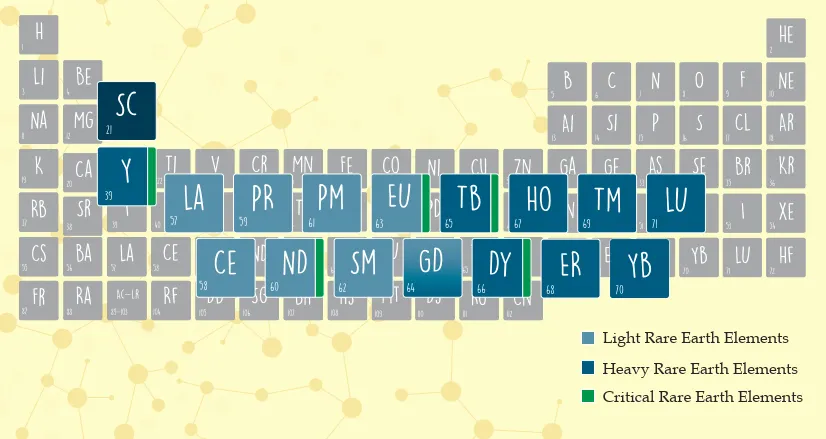

Rare earth elements (REEs) are a group of 17 critical minerals essential for modern industrial and technological development. All REEs share similar properties and tend to occur together in the same geological deposits. The group includes eight elements from the lanthanide series, seven from the actinide series, and scandium and yttrium (see Figure 1).

Figure 1. Rare earth elements in the periodic table.

Despite their name, REEs are abundant in Earth's crust. They are called "rare" because they are found in concentrations too low to mine easily, and separating them from other minerals is costly and environmentally damaging.1

While the terms “rare earth elements” and “critical minerals” are often used interchangeably, critical minerals encompass a list of roughly 30 to 50 strategically important materials, which changes continuously to reflect new market and technological developments. REEs are a subset of 17 chemically similar elements within the wider category of critical minerals.

Why are rare earth elements important?

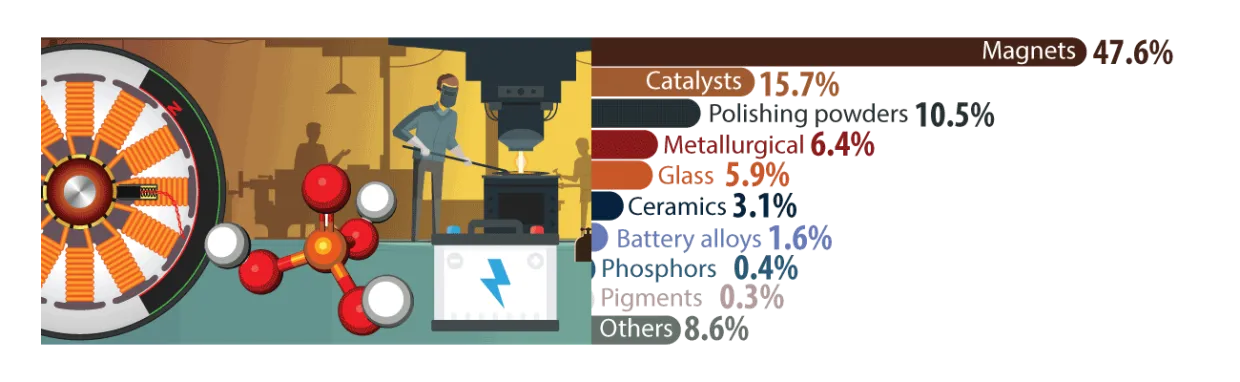

REEs possess unique magnetic, optical, and electronic properties that allow engineers to miniaturize technologies.2 REEs are irreplaceable components in many clean energy technologies, such as wind turbines, solar panels, and electric vehicle batteries (see Figure 2). Furthermore, they have military applications, acting as essential materials for radar systems, jet engines, and nuclear submarines.3

Natural Resources Canada

Figure 2. Rare earth element uses.

Global demand for REEs is expected to grow dramatically, driven by their critical role in everything from consumer electronics and defense technology to clean energy transition. As China currently controls approximately 70% of world production and 87% of refining,4 discovering and developing new sources has become a major international priority.

Where are rare earth elements found in the Arctic, and how large are the deposits?

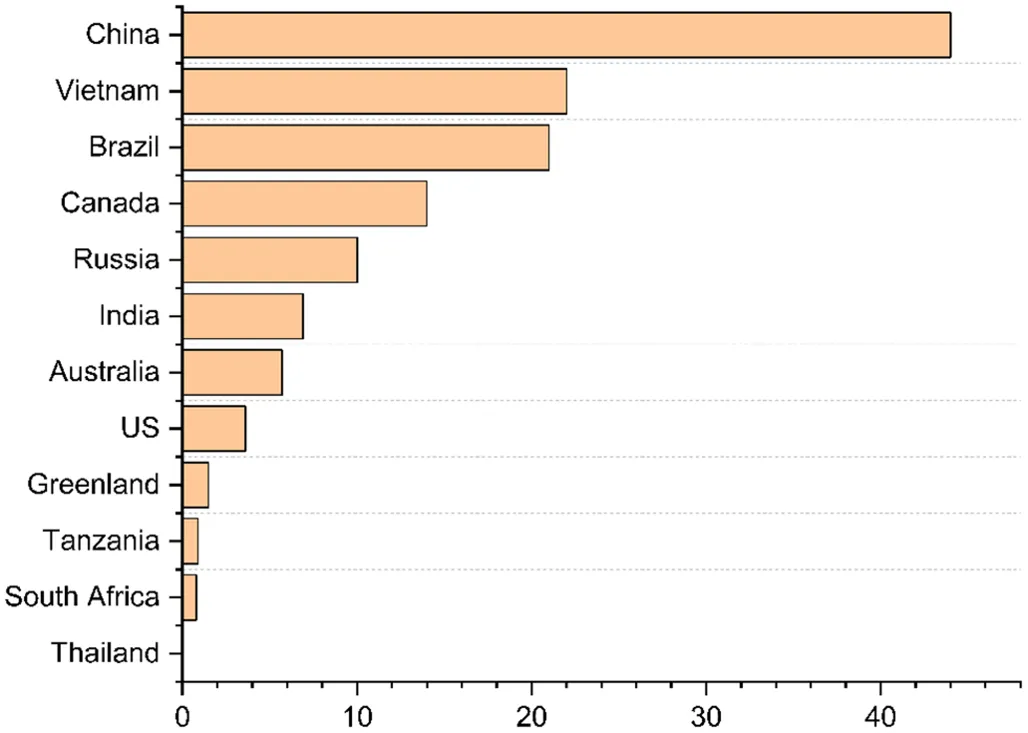

While Arctic nations hold significant REE reserves, they remain marginal players in global production as they lag way behind on processing and refining capabilities. Figure 3 illustrates world mine reserves of REEs by country in 2023 in million tons. China has the largest REE reserves, with the remaining potential supply spread across Vietnam, Brazil, Canada, Russia, and others.

These estimates come with an important caveat: to truly evaluate the quality, quantity, and accessibility of a specific REE deposit, these baseline volume estimates must be contextualized by analyzing the ore's grade and metallurgical complexity, co-location with radioactive materials, required infrastructure investments, and local social license to operate.5

Alexandra Middleton

Figure 3. World mine reserves of rare earth oxides by country in 2023 in million tons. Note: REEs almost never exist in pure form in nature. Instead, they naturally bond with oxygen to form rare earth oxides (REOs), the stable, processed compounds that the mining industry produces, trades, and uses as the standard unit to measure a country's reserves. Source: Created by Middleton (2026) based on data from U.S. Geological Survey's January 2024 Mineral Commodities Summaries. Reserves in Australia, Russia, Thailand, and the United States were revised based on company and government reports.

REEs are distributed across several nations within the Arctic region, with significant deposits becoming increasingly accessible as ice retreats. The sizes and specific locations of these deposits vary by country, as described below.

Canada

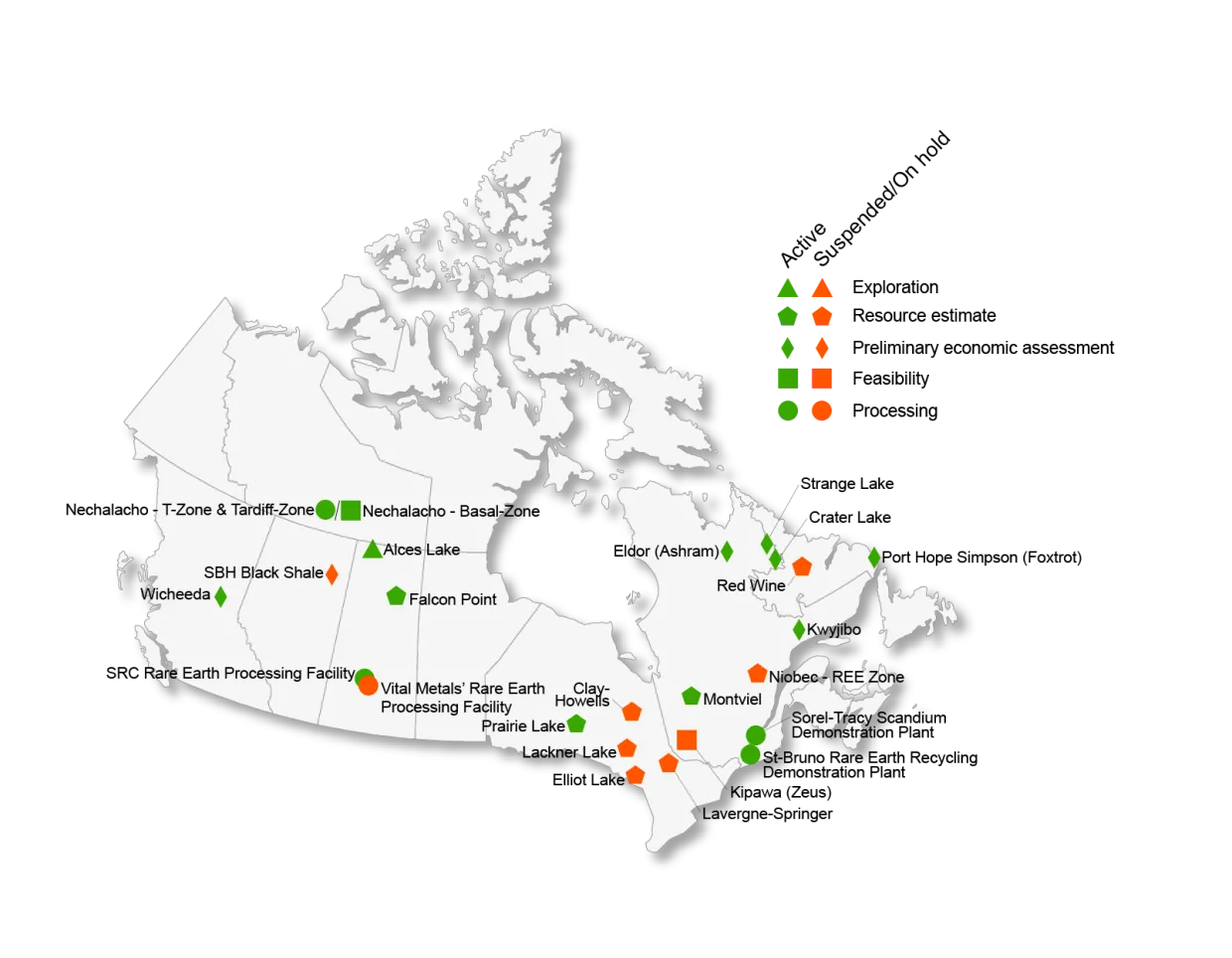

Canada holds over 10% of the world's known REE reserves (estimated at 15.2 million tons of rare-earth oxides), positioning it as a potential alternative to suppliers like China and Russia.

Natural Resources Canada

Figure 4. Rare earth elements projects in Canada, 2024.

Deposits in the Northwest Territories and Northern Quebec are rich in heavy rare earth elements (HREEs), high-value materials essential for powerful magnets and clean energy technologies. Because HREEs are scarcer than their light counterparts, they command significantly higher prices, making Canada's northern deposits strategically important and commercially attractive. Two projects, Nechalacho (NWT)6 and Strange Lake (Quebec),7 are undergoing advanced feasibility and environmental review and are expected to receive their final permits in 2026.

However, the vast majority of Canada's REE reserves remain unmined in the ground. Many reserves are considered commercially off-limits because they are too difficult to extract, pose severe risks of environmental degradation, or are located too close to Indigenous lands, where extraction is opposed or controversial. When Indigenous communities have the power to set the rules, reduce negative impacts, and secure real financial rewards through Impact and Benefit Agreements, it builds trust and support for minerals extraction.8 Overall, the process for developing mines has been slow due to several factors: long permitting, lack of capital, and/or conflicts over land use.

Only three sites are currently advanced enough to process these minerals into usable forms: the Saskatchewan Research Council’s rare earth processing facility, the Sorel-Tracy scandium plant, and the St-Bruno recycling facility.

The Canadian government recently announced a $12.1 billion federal investment aimed at building a complete domestic supply chain from mines to finished magnets.9

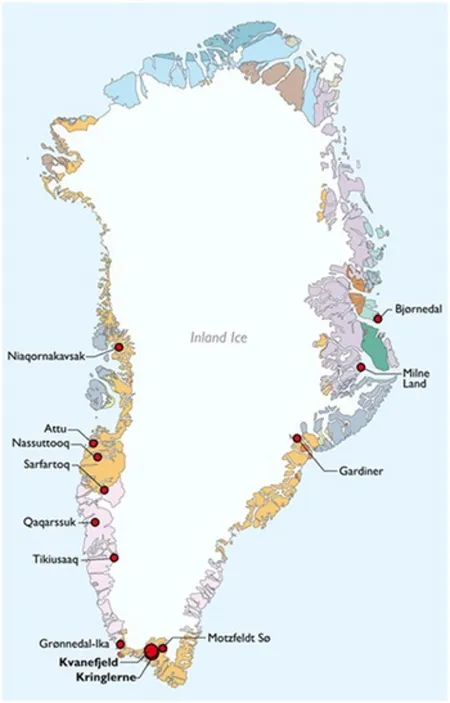

Greenland

EURARE/British Geological Survey

Figure 5. Known rare earth element deposits in Greenland.

Greenland holds approximately 1.5 million tons of REEs, totaling 2% of known global reserves, concentrated primarily in unique geological formations across the island's south.10 On one hand, Greenland’s reserves are much smaller than those of its Arctic neighbors, Canada, Russia, and the United States. On the other hand, Greenland has attracted disproportionate geopolitical attention because of the sheer size and concentration of some of its deposits, which rank among the largest on Earth.

Despite this substantial potential, commercial production remains in the developmental stage. Kvanefjeld, holding over 11 million metric tons, including 370,000 tons of high-value HREEs, remains stalled due to local political opposition and a uranium mining ban.11 Tanbreez (Kringlerne), potentially even larger at up to 45 million tons, is fully permitted and recently secured U.S.-backed financing to begin construction, targeting first ore production by late 2028 or early 2029.12

Additional deposits at Motzfeldt Sø, Grønnedal-Ika, and Sarfartoq are still at the exploration stage (see Figure 5). However, corporate operators are actively advancing these sites through updated economic assessments, bulk sampling, and feasibility studies to prepare for future exploitation licenses.13

On one hand, Greenland’s reserves are much smaller than those of its Arctic neighbors, Canada, Russia, and the United States. On the other hand, Greenland has attracted disproportionate geopolitical attention because of the sheer size and concentration of some of its deposits, which rank among the largest on Earth.

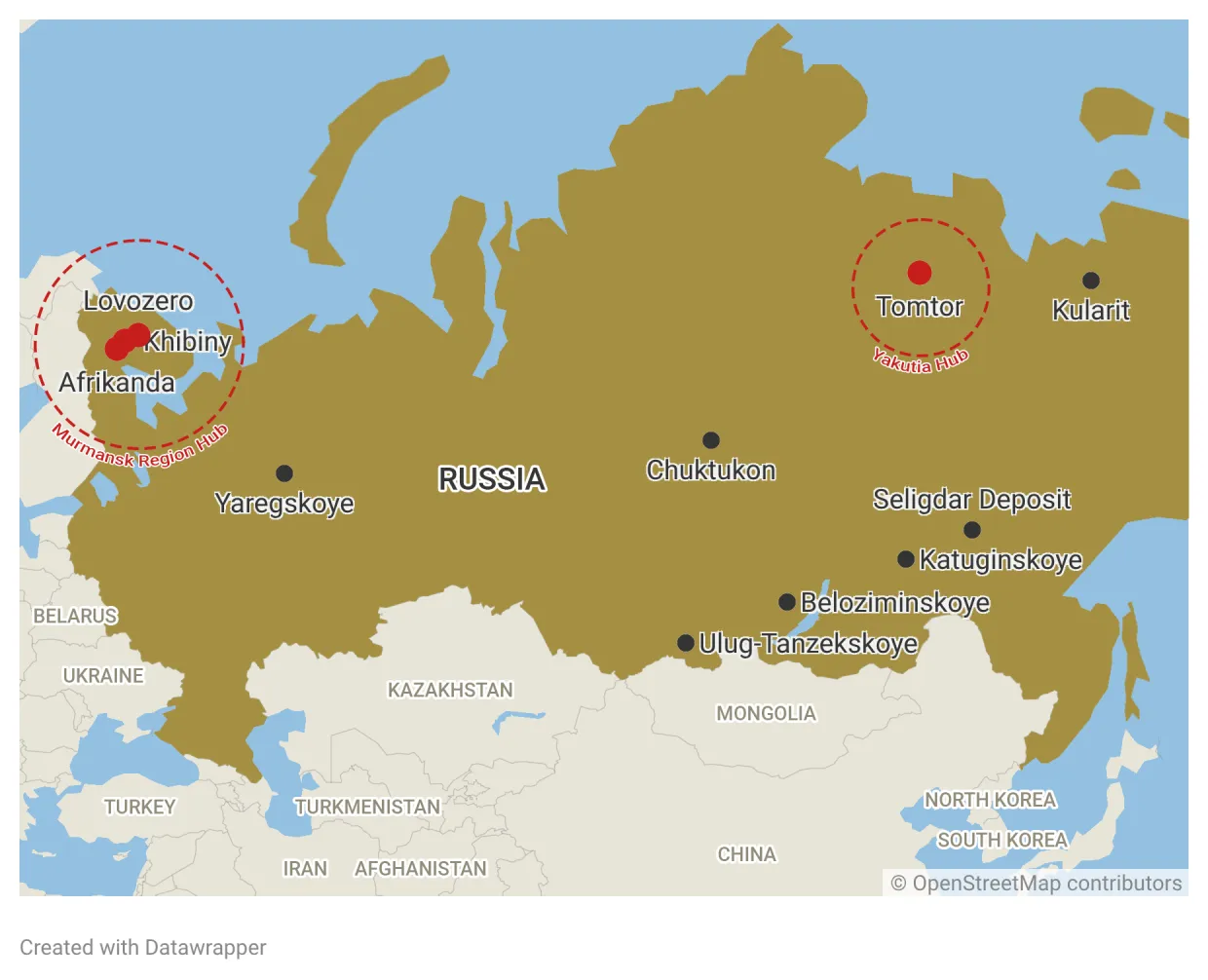

Russia

Russia holds over 10% of the world’s known REE reserves, 60% of which is concentrated in Russia’s Arctic zone. Development is focused on two major hubs: one located in the Murmansk region (Khibiny, Lovozero and Afrikanda deposits) and the other in Yakutia (Tomtor), marked by red dots on the map (see Figure 6).

Alexandra Middleton and Elizabeth Hanlon-Warren/Serdyuk et al.

Figure 6. Known rare earth element deposits in Russia. Source: Map created with Datawrapper by Elizabeth Hanlon-Warren based on information from Serdyuk et al., "The Chuktukon niobium-rare earth metals deposit: Geology and investigation into the processing options of the ores," Minerals Engineering, 113 (2017), 8-14.

Although the Murmansk region holds substantial REEs, its actual production remains globally marginal and is currently limited entirely to the Lovozero deposit.14 Meanwhile, the region's other major REE deposits remain untapped, as the actively mined Khibiny deposits leave their REE content unrecovered and the promising Afrikanda site is still in the exploration phase.

Much of Russia’s REE production used to go to Estonia for processing, but Russia is trying to become self-reliant by building its own processing and refining facilities.15 Deposits in the Murmansk regions are being developed as a full-cycle processing hub for refining and manufacturing REEs locally.16

Further east, Yakutia's highly concentrated Tomtor deposit represents a longer-term but potentially transformative asset, with planners projecting that it will develop into an entirely new Arctic industrial district comparable in scale to the Norilsk complex.17

Sweden

Sweden gained attention for its REE potential with the 2023 discovery of the Per Geijer deposit near the Kiruna iron mine, which holds over one million metric tons of rare earth oxides (see Figure 7). This makes it the largest reported deposit of its kind in Europe, with additional rare earths found mixed into iron ore in the nearby Malmberget and Svappavaara fields.

However, extracting REEs is not yet a reality because the REEs at the Per Geijer deposit are tightly bound within iron ore as a by-product, and complex processing infrastructure is needed before they can be commercially separated and sold. Furthermore, the discovery of the Per Geijer deposit has sparked conflict with Indigenous Sami reindeer herders,18 who have expressed deep concerns about the negative impact this mining expansion could have on their traditional lands.

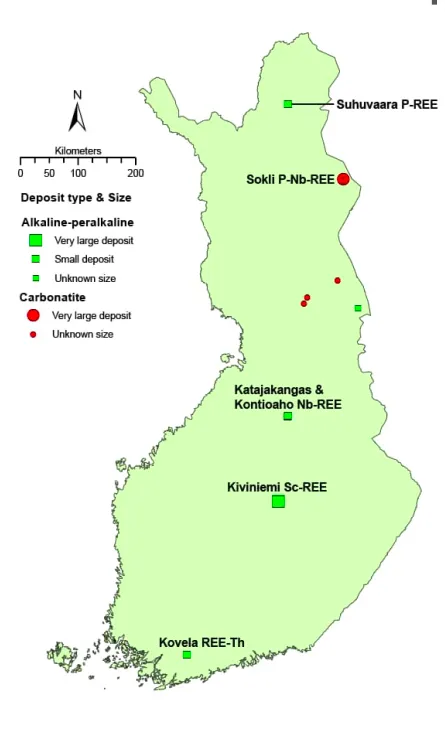

Finland

Coint et al./Geological Survey of Finland

Figure 8. Rare earth element projects and deposits in Finland, 2024. Source: Coint et al., "Rare Earth Elements in the Nordic Countries," Geological Survey of Finland, https://www.gtk.fi/app/uploads/2024/03/Rare-Earth-Elements-in-the-Nordics-Nolwenn-Coint.pdf

The Sokli deposit in Savukoski, located in Eastern Lapland (see Figure 8), contains a significant quantity of REEs with the potential to supply 10% of Europe's annual REE demand for permanent magnets.19 In February 2026, the Finnish Government allocated €65 million to the Finnish Minerals Group to advance the project to the prefeasibility study phase (2026–2028). This funding covers the construction of a pilot mine and concentrator, with test operations expected to begin in autumn 2026.20

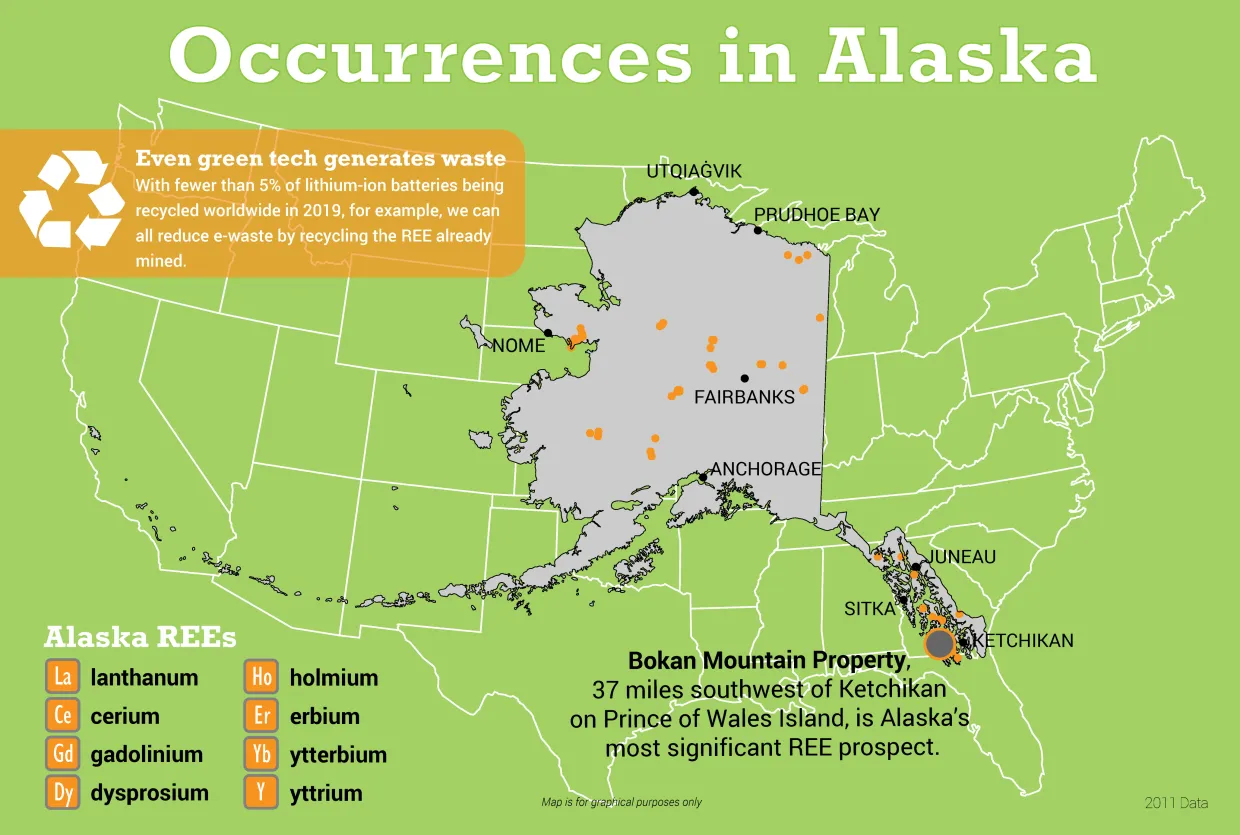

United States

Alaska’s Bokan-Dotson Ridge is home to one of the largest undeveloped primary U.S. sources of heavy REEs (see Figure 9). While national resources now exceed 8.6 million tons following discoveries in Wyoming,21 Bokan remains critical because of its high mineral concentration. According to Ucore Rare Metals the Bokan-Dotson Ridge deposit in Alaska is currently in the advanced development stage; project operators estimate that commercial infrastructure construction could commence within 30 months of securing final project funding.22

Supported by an $18.4 million DoD grant,23 Ucore Rare Metals is first establishing the Strategic Metals Complex processing facility in Alexandria, Louisiana, which will eventually refine the heavy rare earth feedstock mined from their Bokan-Dotson Ridge property in Alaska.

U.S. Department of the Interior Bureau of Land Management.

Figure 9. Rare earth element occurrences in Alaska. Source: U.S. Department of the Interior Bureau of Land Management.

Norway

Norway currently has no active REE or advanced projects in the Arctic because its major discoveries, including the largest deposit in Europe, are located far to the south.24

Iceland

Iceland holds no known REE deposits. The volcanic basalt geology of the island does not have rock formations where rare earth elements usually accumulate.

Potential benefits

Arctic REE mining offers the strategic benefit of supply chain diversification, ensuring stable access to the critical minerals required for defense systems, wind turbines, and electric vehicles. Locally, mining promises economic revitalization, job creation, and tax revenues, which is particularly appealing to territories such as Greenland seeking economic independence. Furthermore, mining projects drive the construction of vital infrastructure—including roads, ports, energy networks, and housing—delivering long-term developmental benefits that extend well beyond the mining sector to support the Arctic region.

Potential risks

Arctic ecosystems are highly fragile and poorly equipped to withstand industrial disruption. Mining carries serious environmental risks, including toxic wastewater contamination, as illustrated by the Talvivaara multimetal mine disaster in Arctic Finland, where repeated leaks devastated surrounding waterways.25 The risks associated with REE mining include the release of radioactive byproducts, such as uranium, which frequently occur alongside REE deposits.

Mining sites in the Arctic frequently overlap with traditional lands, directly threatening the subsistence livelihoods, culture, and reindeer herding practices of Indigenous Peoples.

Economically, Arctic mining presents substantial challenges. The biggest obstacle is the lack of infrastructure: roads, ports, and electricity generation. Furthermore, the harsh climate severely restricts the operating windows and logistics. Because of these extreme conditions and the complex processing technology required to separate REEs, extracting these minerals requires substantial upfront capital, making many projects difficult to finance.

Antti Lankinen/CC BY 2.0

Figure 10. Aerial photograph of the waste water pond at Talvivaara mine in Sotkamo, Finland, June 2013. Repeated leaks devastated surrounding waterways.

What is getting lost in the current conversation about Arctic rare earth elements?

Environmental Baselines: Within this charged geopolitical landscape, scientists are raising an important and frequently overlooked concern: the need to establish environmental baselines before large-scale REE extraction begins in the Arctic. Much of the Arctic still requires mapping and assessment, leaving researchers a closing window to measure naturally occurring rare earth levels in ice cores, marine sediments, and the atmosphere. These baselines enable scientists to distinguish natural geological phenomena from minerals released by hydrothermal vents, crustal dust, or thawing permafrost from industrial contamination. Baselines also serve as indispensable legal and scientific instruments for proving industrial negligence and resolving transboundary pollution disputes once large-scale extraction operations commence.

Reality vs. Potential: While the Arctic holds large, estimated deposits, the reality is that few are currently operational. In Greenland, despite vast reserves, there are zero active REE mines.26 A handful of projects are beginning to advance, but all face the same structural barriers: the capital and infrastructure required to mine in remote Arctic conditions, and the unresolved social conflicts surrounding Indigenous land rights and local community acceptance.

Although the Arctic might contain the reserves the world seeks, extracting them in a way that is both sustainable and beneficial to Arctic communities presents a distinct challenge.

Recommended citation

Middleton, Alexandra. “Mining Rare Earth Elements in the Arctic: Reality Versus Potential.” Belfer Center for Science and International Affairs, July 7, 2026

Mining Rare Earth Elements in the Arctic: Reality Versus Potential

Duchna, M., & Cieślik, I., "Rare earth elements in new advanced engineering applications," in Rare earth elements - Emerging advances, technology utilization, and resource procurement, ed. Aide, M., (IntechOpen, 2022). 10.5772/intechopen.109248

Prno, J., Pickard, M., & Kaiyogana, J., "Effective community engagement during the environmental assessment of a mining project in the Canadian Arctic," Environmental management, 67:5 (2021), 1000-1015.

Middleton, A., "Geopolitics of Rare Earth Elements (REE) in the Arctic: Study of evolving strategic, scholar, and media discourse," Polar Record, 62:e3 (2026), doi:10.1017/S0032247425100193

Schwartz. M. & Baskaran, G., "Greenland, Rare Earths, and Arctic Security," Center for Strategic and International Studies, January 8, 2026, https://www.csis.org/analysis/greenland-rare-earths-and-arctic-security

Middleton, Alexandra. “Mining Rare Earth Elements in the Arctic: Reality Versus Potential.” Belfer Center for Science and International Affairs, July 7, 2026