Expose new large loads to price signals

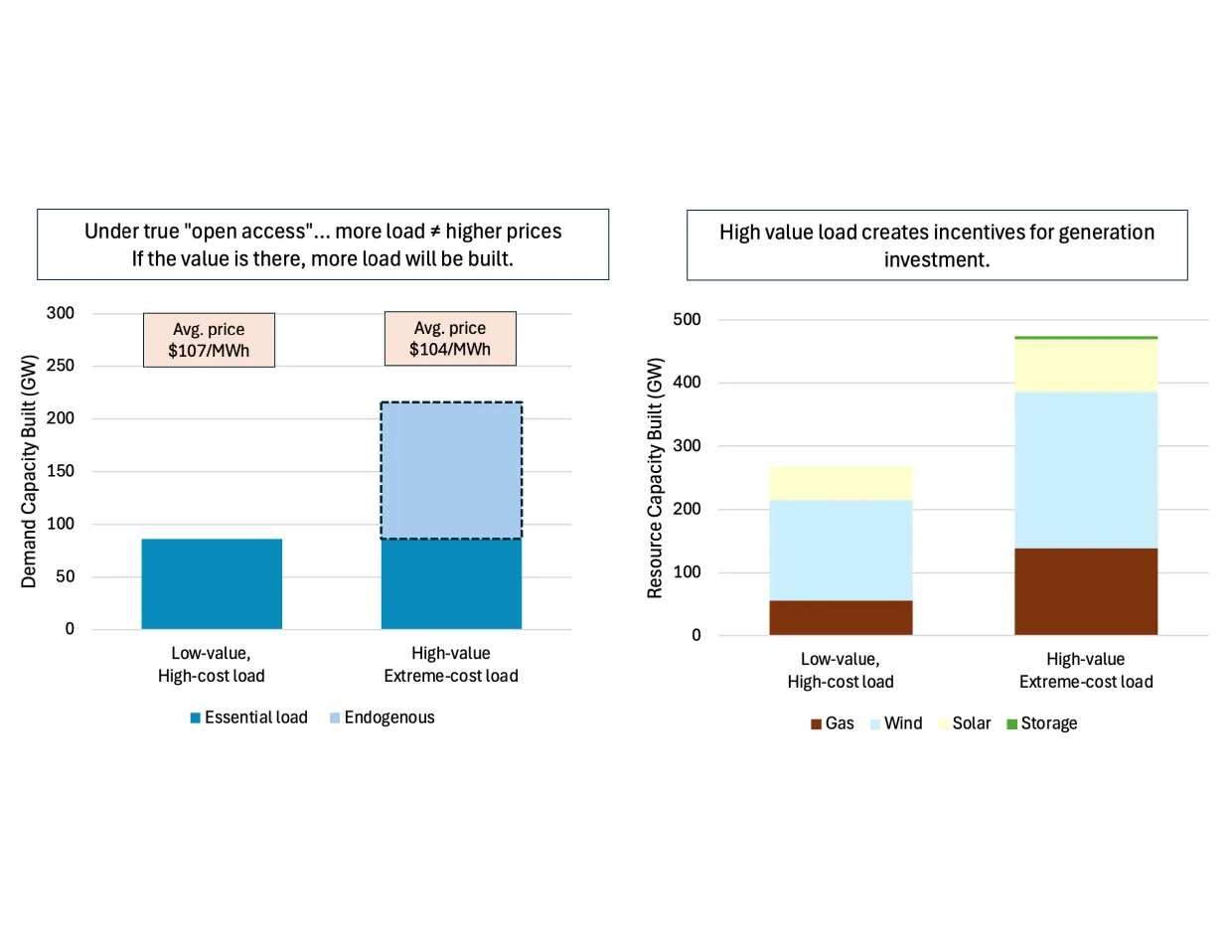

Regulators can expose new large loads to market price signals and encourage them to self-hedge. Exposing demand to market price signals incentivizes flexibility (e.g. spatio-temporal load shifting in a data center) and bidding with price-elasticity matching the actual value of load that can result in lower overall system costs. Consider that for a load to truly be inelastic, it must have a value of consumption of electricity on the order of $10,000 for each MWh consumed. For a residential consumer, the value of electricity consumption may be greater than the ability to pay. However, for a large industrial load like a data center, the value of consumption is the ability/willingness to pay; the business proposition is that the revenue generated is at least as great as the cost of the input. Even if most new load is inelastic/inflexible, it may not take much elastic load to materially impact price extremes and volatility. Loads will also be incentivized to enter into forward contracts with new supply resources or bring their own generation. The efficient price enables the discovery of the optimal mix of own-generation, new contracted supply resources, and flexible operation.

Consider hedging over price caps to protect mass-market consumers

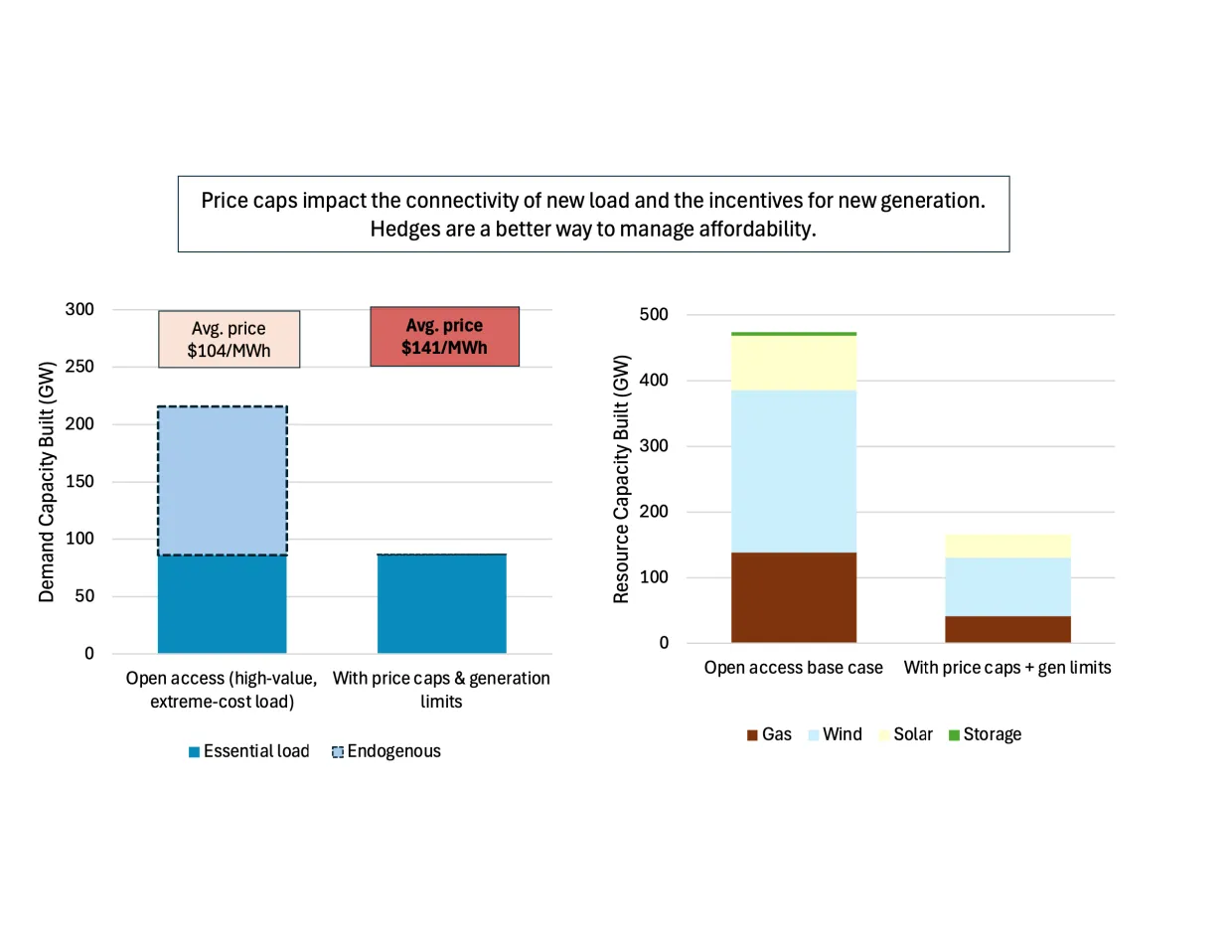

Regulators should focus on hedging arrangements rather than blunt price caps if measures are required to protect consumer bill exposure. However, hedging of consumers is itself a careful balance. On one hand, it can provide consumers with protection from the burden that arises from price volatility under extreme events (especially those who are vulnerable). On the other hand, such protections may mute or otherwise distort the natural price elasticity that may emerge from consumer flexibility and distributed technologies such as EVs and heat pumps. Hedges must be carefully designed to provide extreme rate protection while also preserving incentive compatibility. While many consumers are on fixed-rate tariffs, the period (e.g., annual) over which tariffs are reset could expose them to price volatility. Furthermore, with a fixed rate there are no incentives to respond to price. Tariff designs such as rate caps (or average-rate options) may provide alternatives for limiting exposure to high market prices, while maintaining incentives for price-based response. It is also important to note that currently a significant driver of high retail tariffs relates to transmission and distribution (and in some jurisdictions, capacity market) rather than energy charges.

Consider mandatory forward hedging where appropriate

Outcomes with contracting depend on who is risk-averse and the role of financial intermediaries. If demand is risk-neutral, then the existence of third parties that are willing to trade risk with the risk-averse producer are critical; in the absence of these financial risk-trading intermediaries, less generating capacity will be built. This study also shows that forward contracting is critical to high-welfare market outcomes. However, in many jurisdictions the the threat of high prices is not credible due to expected regulatory intervention, and consumers are indiscriminately curtailed during outage events — both factors create an incentive to under-hedge. Market designers may consider that assuming no risk of political intervention is unrealistic. This motivates mandatory or centralized forward energy markets/contracting as a way to ensure hedging and efficient capacity investment. However, efficiency losses should be expected with more reliance on administratively-determined mandatory quantity hedges rather than credible exposure to scarcity price signals that lead market participants to determine their own optimal hedging arrangements.

Capacity markets have downsides

Resource adequacy approaches relying on capacity markets or mechanisms may have downsides. A capacity market is a limited type of centrally administered forward contract around estimated capacity availability rather than energy, typically accompanied by energy market price caps. First, capacity markets may favor gas over renewables and storage. We find that even in an idealized version of a capacity market (a call option) in which energy prices are not suppressed, the portfolio mix tends to shift toward lower capital expenditure, higher variable-cost technologies like gas over renewables and storage. Second, in more realistic implementations of capacity markets with energy price caps, the capacity auction would have to administratively determine and encode the true value of lost load, as the contract market would otherwise not see the real scarcity value. Even so, there would not be a real-time market to settle residual quantity risk at the efficient price. Furthermore, recent price spikes in the PJM capacity auction indicate that capacity markets settled on an annual basis do not necessarily reduce consumer exposure to high prices.

Demand differs in risk appetite

Different types of demand (mass-market vs large industrial/data centers) have different risk preferences and care about different downside risks. Large industrial consumers may have greater risk appetites and not be as concerned with hedging against their own high demand scenarios corresponding to when business is good. These differences can result in significantly different generation capacity investment and demand investment decisions when appropriate market signals exist. Regulators concerned about protecting existing and small-scale consumers should seek to expose new large loads to market signals such that they are incentivized to hedge appropriately; the alternative, and often status quo, is to assume that all new demand is exogenous (completely indifferent to price signals) with the same risk profile as commercial and residential consumers. This can lead to socializing the risk across all customer classes.

Don’t cross-subsidize with electricity rates or transmission

Regulators should be wary of cross-subsidizing new large loads at the expense of mass market consumers. These cross-subsidies could come in the form of implicit time- and locational-hedges by not charging data centers the wholesale locational marginal price. If we externalize the externalities of local pollution, another cross-subsidy can occur with onsite generation of natural gas that negatively impacts the surrounding community. Another implicit subsidy is transmission and distribution upgrades that disproportionately benefit data centers socialized across all consumers. Regulators should use a more granular approach to beneficiary pays cost allocation. In the United States, FERC Order 1920 seems to provide the basis for more granularity, but this to date has been resisted by big data companies on the grounds of treating all consumers the same despite vast differences in risk appetite and capital between mass market consumers and large industrial load.

Restricting renewables raises prices

Limiting solar and wind does not mean that the same demand will be necessarily be served by more gas, and all else being equal, average prices will rise. Recent energy policy that has introduced constraints or blocked permitting for wind and solar may therefore result in less overall demand being built and served at higher prices.

Create environments for optimal supply and demand investment

Regulators should create environments that lead to optimal supply and demand investment decisions. This entails an efficient price at the core of the system from which investing and contracting decisions are made. It also requires a timely permitting and interconnection process. While optimal, this pathway is challenging, and short-run considerations must also be made to protect existing consumers from demand shocks where appropriate. We advocate this be done via hedging arrangements around the efficient price rather than blunt price caps. New large loads like data centers have the ability in the long-run to choose their size and location, and they should be incentivized to enter into their own hedging arrangements with producers. This can result both in greater demand investment and supply investment while preserving reliability and affordability.

This policy brief represents the authors’ work only and does not represent the views of any organization, company or institution. Any errors or misstatements remain our own. Contact: conleigh.byers@fticonsulting.com, farhad.billimoria@oxfordenergy.org