Research, ideas, and leadership for a more secure, peaceful world

Reports & Papers

Critical and Emerging Technologies Index

Built with public and commercial data, this Index is a quantitative model presented through an interactive dashboard. It enables policymakers, strategists, and researchers to assess the national power of 25 countries across key technology sectors: Artificial Intelligence, Biotechnology, Semiconductors, Space, and Quantum. Move the sliders in the Dashboard below to test different analytic inputs, and read the country reports for in-depth analysis on different nations' tech trajectories.

News headlines often make sweeping claims about the geopolitics of technology today—for instance, suggesting that China has far surpassed the United States in advanced technologies, or that Europe is losing ground in technology competition. Yet it is difficult to find robust, cross-sector data to support such comparisons. The Critical and Emerging Technologies Index helps fill this gap by enabling policymakers, strategists, and researchers to assess the technological power of 25 countries. Built using thousands of public and commercial data points, the Index is a quantitative model presented through an interactive dashboard that benchmarks progress in Artificial Intelligence (AI), Biotechnology, Semiconductors, Space, and Quantum. The dashboard features adjustable indicators within each sector, allowing users to customize the model and gain insights into the relative strengths and shortcomings of each country.

This report provides context and analysis that help make sense of the data visualized in the Index Dashboard. It offers unique insights into the ways in which the geopolitics of technology are changing, both within and across sectors.

Key Judgments:

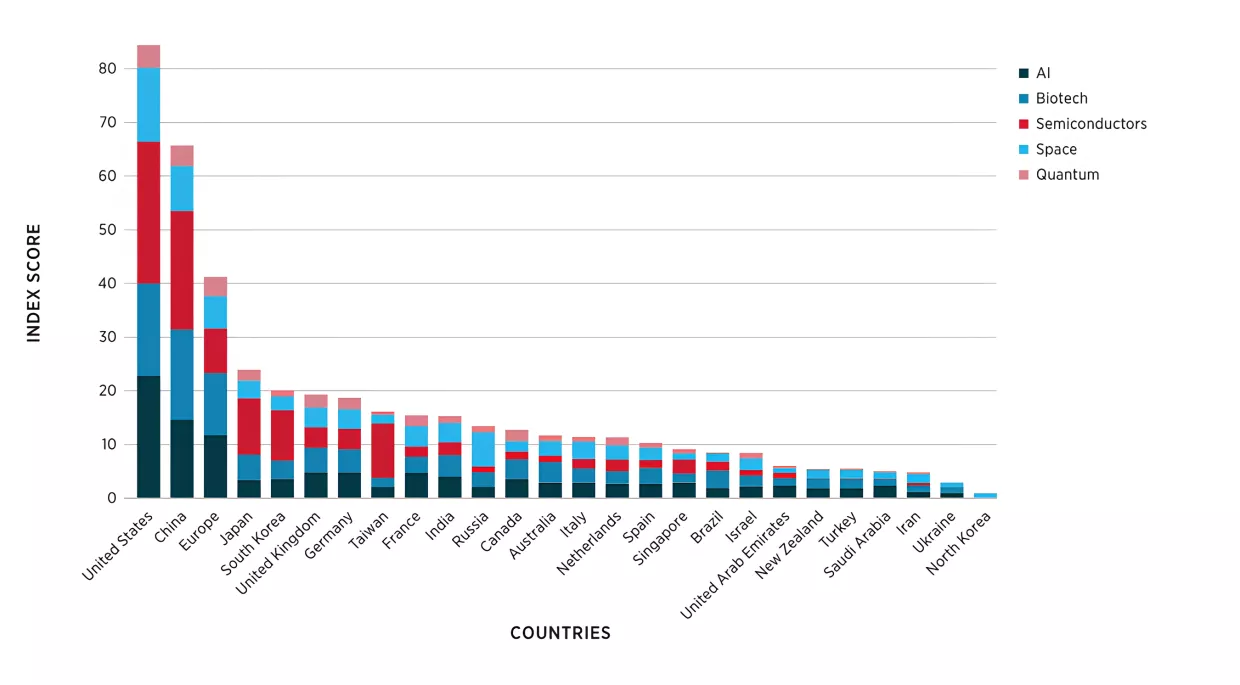

The United States leads China and Europe in all sectors of the Index, primarily because of the unique innovation ecosystem that it has developed over the past several decades. U.S. performance is largely powered by economic resources and human capital, reflected in the scale of American public and private investment and its heterogeneous research workforce. The country’s decentralized innovation ecosystem—where resources, ideas, and authority are distributed across a myriad of government entities, universities, start-ups, and corporations—enables actors to expediently pool expertise and scale innovations.

Although China still trails the United States, it remains competitive and is closing the gap across several sectors. China lags in semiconductors and advanced AI due to reliance on foreign equipment, weaker early-stage private research, and shallower capital markets, but it is far closer to the United States in biotechnology and quantum, where its strengths lie in pharmaceutical production, quantum sensing, and quantum communications. Backed by economic resources, human capital, and centralized planning, China is leveraging scale to reduce dependence on imports, attract innovation within its borders, and boost industrial competitiveness.

Europe is competitive in critical and emerging technologies relative to the U.S.-China duopoly. Europe is third in the context of AI, biotechnology, and quantum technologies. Yet China and Russia outpace Europe in space, and China, Japan, Taiwan, and South Korea eclipse Europe in semiconductors. Indeed, Europe’s shortcomings with semiconductors significantly lower Europe’s overall standing compared to the United States and China. The region’s ability to fulfill its technological potential will ultimately depend on the integration of governance and capital across the region.

Collaborative partnerships with Europe, Japan, and South Korea make the United States significantly more powerful in critical and emerging technologies, particularly in the context of quantum, semiconductors, and biotechnology. The United States is powerful across all sectors but does not have full supremacy; for instance, no country has complete, end-to-end control of a supply chain for advanced semiconductors. These gaps create critical chokepoints, limiting the ability of any one country to shape the global balance of power alone. To ensure that the West remains competitive and resilient, the United States must deepen collaboration with its allies and partners.

The United States has a considerable advantage in AI, but China and Europe have made significant progress and have unique advantages that will challenge the American AI lead in the next decade. The United States dominates in terms of its economic resources, computing power, and algorithms. The 2025 release of DeepSeek’s R1 model and Alibaba’s Qwen3 family of models, however, demonstrated that the U.S. lead in AI may be more vulnerable than previously assumed. China leads in terms of data and human capital; these advantages will help it close the U.S. edge in AI if it can overcome the obstacles presented by U.S. export controls. Europe’s strength in AI is largely derived from its strong data and human capital, giving it the potential to accelerate its AI capabilities if it improves its regulatory environment.

Among the technologies examined in this Index, China has the most immediate opportunity to overtake the United States in biotechnology; the narrow U.S.-China gap suggests that future developments could quickly shift the global balance of power. The United States and China perform similarly in biotechnology overall, with China’s strengths underpinned by its human capital.The United States excels in security, genetic engineering, vaccine research, and agricultural technology, bolstered by private-sector innovation and public-private partnerships. China has dominance in pharmaceutical production through extensive, large-scale public investments and state-backed manufacturing.

The dominance of the United States, Japan, Taiwan, and South Korea in semiconductors persists at critical chokepoints of the supply chain: advanced manufacturing and fabrication, chip design and tools, and equipment. These pillars have the greatest variance among all included in this Index due to high costs and technical barriers. While many countries are investing heavily to close these gaps, capital alone is unlikely to be sufficient to establish an end-to-end semiconductor production capability; if countries aim to break free from dependence on the current leaders, they will need to simultaneously secure equipment and design intellectual property.

The American private sector drives the United States’ strong lead in space, though its vulnerabilities in orbit to Chinese and Russian military capabilities increase strategic risk. Washington’s edge stems from productive public-private partnerships that have helped the United States dramatically increase its launch frequency and payload capacity while reducing per-mission costs. However, the United States is asymmetrically vulnerable in space, relying heavily on space-based systems for military operations and for supporting critical sectors of the American economy. China and Russia are also fielding formidable anti-satellite capabilities, offsetting the United States’ lead in space and increasing its strategic exposure.

Quantum technologies remain in an early research phase, with current efforts focused less on deployment and more on advancing early-stage concepts. This relative lack of investment has contributed to the fragmented and region-specific development of quantum ecosystems. In the United States and Europe, universities lead foundational research, startups develop specialized tools and systems, and large corporations scale engineering and infrastructure for quantum technologies. China takes a more opaque, state-led approach, with less separation between research, development, and industry.

This publication introduces the inaugural Critical and Emerging Technologies Index, designed to help policymakers and strategists assess national power in and across critical domains of technology. Built using public and commercial data, the Index is visualized through an interactive dashboard that benchmarks advancements across 25 countries in Artificial Intelligence (AI), Biotechnology, Semiconductors, Space, and Quantum. The Dashboard features adjustable indicators within each technological sector, empowering users to make custom changes and obtain insights into each country’s relative strengths and shortcomings.

Power is difficult to define and measure. While some policymakers see it primarily in terms of military might, others point to economic strength or ideational and cultural influence as more relevant indicators.1 This report defines power as the ability of a nation to achieve its national interests through the control of resources, material, and ideas.2 In a world increasingly defined by innovation, critical and emerging technologies are integral to national power. After all, technological evolution is a process largely shaped by geopolitics.3 Science, innovation, technology, and industry have catalyzed societal transformations throughout history; these developments subsequently influenced the ways that states developed and employed technologies.4 The most powerful nations have built advanced innovation ecosystems, supported by research and both public and private investment. These ecosystems form a critical foundation of their technological power: the capacity to harness innovation and employ new technologies to modify systems and catalyze change on the global stage. As geopolitical competition unfolds in an era of interdependence, technological power enhances sovereignty.

Yet, despite growing policy interest in countries’ advancements with critical and emerging technologies, there are few tools to facilitate comprehensive comparisons across interconnected technology sectors. Some notable efforts include the Stanford Institute for Human-Centered AI’s Artificial Intelligence Index Report 2024, the Australian Strategic Policy Institute’s Critical Technology Tracker, and the Lowy Institute’s Asia Power Index. The primary goal of the Index is to fill this gap, facilitating comparative, cross-sector technology analysis for informed geostrategic decision-making. It presents data through an interactive Dashboard with adjustable parameters, enabling users to generate tailored data visualization on the geopolitics of technology. A policymaker or strategist can use this Index Dashboard, for instance, to explore the sectors in which countries lead or lag, evaluate the strengths and weaknesses of countries across technology sectors, and assess changes over time as new data is incorporated.

The White House Office of Science and Technology Policy’s 2024 updated list of critical and emerging technologies guided the selection of the five sectors featured in this Index: AI, Biotechnology, Semiconductors, Space, and Quantum.5 Many countries and international organizations—such as Australia, the United Kingdom, the European Union, Germany, China, Japan, South Korea, and NATO—have also published technology lists highlighting similar sectors of interest.6 Innovation in these five areas helps drive progress across other technology sectors; advancements in one can facilitate greater efficiency, capability, and competitiveness across others. These sectors are also vital to the national security and strategic autonomy of states, helping governments navigate future geostrategic challenges and seize new opportunities.7

Actors Included in the Index

Australia, Brazil, Canada, China, Europe, France, Germany, India, Iran, Israel, Italy, Japan, Netherlands, New Zealand, North Korea, Russia, Saudi Arabia, Singapore, South Korea, Spain, Taiwan, Turkey, Ukraine, United Arab Emirates, United Kingdom, United States.8

The methodology behind the Critical and Emerging Technology Index can be broadly separated into three distinct parts.9 First, 48 key dimensions across all the technology sectors—referred to in this report as pillars—were identified, along with corresponding sub-metrics designed to capture a country’s proficiency in each sector. These pillars fall into two categories: four to five fundamental cross-sector pillars consistently applied across all critical and emerging technologies (including Economic Resources, Human Capital, Security, Regulatory, and Global Player), and three to five sector-specific pillars, which vary by sector and are tailored to reflect unique characteristics of the technologies and systems in question. In the Index’s space sector, for example, Economic Resources and Domestic Launch Capability serve as fundamental and sector-specific pillars, respectively. Second, over 3,375 individual data points were compiled, organized, and validated to comprise sub-metrics under each pillar. Third, the data was reviewed and normalized to meaningfully measure countries and preserve each sub-metric’s relative importance. Altogether, this process enabled the assignment of weights to sectors and pillars, which were multiplied by each country’s normalized scores and summed to generate either sector-specific scores or final composite scores for countries across all sectors. Using the Dashboard, users can personalize this process, inputting their own sector and pillar weights to create tailored assessments. (For more information on the methodology of the Index, see the Annex of this report.)

The default sector weights used in the Index were generated using a structured scoring method that reflects the relative strategic value of the different technology sectors. This method began with identifying six criteria that define each technology sector: geopolitical significance, systemic leverage, GDP contribution, dual-use potential, supply chain risk, and time to maturity.10 Technologies were then rated on a scale of one to five across these criteria; these ratings were multiplied by corresponding criteria weights, with the sum of these products yielding a comprehensive raw score for each sector.11 Raw scores were then normalized and rounded to generate the final default sector weights: 35% for Semiconductors, 25% for AI, 20% for Biotechnology, 15% for Space, and 5% for Quantum.12 Once again, rather than being a conclusive assessment of the sources of technological power, these sector weights are provisional and intended as a reference point for further analysis.

Main Themes

The Index shows that the United States is strong across all critical and emerging technology sectors, with a pronounced lead in space and artificial intelligence. The United States’ performance is largely driven by economic resources and human capital, reflected in the scale of American public and private investment and its heterogeneous, world-class research workforce. The country’s decentralized innovation ecosystem—where resources, ideas, and authority are distributed across a myriad of federal agencies, state and local programs, universities, start-ups, and corporations—enables actors to expediently pool expertise and scale innovations without being constrained by a single central authority. This decentralization remains a core driver behind American dynamism and technological power.13 However, cuts to academic research funding and growing political polarization are hindering the United States’ ability to strategically shape the public and private allocation of resources. The American innovation ecosystem has delivered strong results over the past several decades, but it currently stands to lose talent and funding due to changing federal policy. Washington must reverse volatile actions on trade and end clashes with academic institutions if it wants to preserve U.S. gains and further the American lead in critical and emerging technologies.

The Index also shows that while China largely trails the United States in critical and emerging technologies, it remains competitive and is steadily closing the gap across multiple technological sectors. Despite recent, high-profile advances in indigenous capabilities, China remains behind the United States in semiconductors and AI due to continued reliance on foreign equipment, a lack of early-stage private research ecosystems comparable to the West, and shallower capital markets than those in Western economies. The U.S. lead over China, however, narrows considerably when it comes to biotechnology and quantum. Both are newer, rapidly evolving sectors that operate largely outside traditional technology ecosystems. More specifically, China’s strengths in biotechnology stem from its dominance in pharmaceutical production and manufacturing. In quantum, its strength lies primarily in sensing and communications. China, like the United States, draws strength from its economic resources and human capital—two foundational pillars that are necessary to drive progress across all critical and emerging technologies. These strengths, combined with China’s narrowing gap in biotechnology and quantum technologies, illustrate how Beijing uses scale and centralized planning to seize and create new opportunities: cutting China’s reliance on imports, compelling foreign firms to produce and innovate within its borders, and boosting its industrial competitiveness.14 China’s rise as a technology powerhouse is also reflective of a growing consensus that strategic sectors need government backing to stay competitive, particularly when facing off against heavily subsidized rivals. Still, China remains constrained by large structural challenges: slowing growth, mounting debt, and industrial overcapacity, among others.15

No other nation rivals the United States and China in critical and emerging technologies. A second tier of countries follows well behind the U.S.-China duopoly, with scores steadily declining from one country to the next. These countries, in order, are: Japan, South Korea, the United Kingdom, Germany, Taiwan, France, India, Russia, Canada, Australia, Italy, the Netherlands, Spain, Singapore, Brazil, Israel, the United Arab Emirates, New Zealand, Turkey, Saudi Arabia, Iran, Ukraine, and North Korea.

This balance of power in critical and emerging technologies, however, shifts when Europe is treated as a unified whole. Aggregating the technological strengths of countries in Europe—France, Germany, Italy, the Netherlands, Spain, Turkey, and the United Kingdom—gives the region a collective standing that amounts to roughly half of the U.S. total and two-thirds of China’s. Sector by sector, Europe ranks third in AI, biotechnology, and quantum technologies, but continues to trail Japan, Taiwan, and South Korea in semiconductors, and Russia in space. Still, to foster technological power across Europe as a whole, the region must deepen market integration, coordinate and merge political institutions, and create innovation and capital markets that encourage greater dynamism.

In today’s current geopolitical landscape, even small advancements—particularly in biotechnology and quantum—could have significant ramifications for the future balance of power. After all, technological convergence means that advancements in one sector can create network effects that accelerate progress in other sectors and shape future technologies in ways that are not immediately clear.16 Powerful AI models, for instance, are already helping researchers accelerate drug discovery and predict protein structures, while quantum research is driving the development of improved semiconductor materials for next-generation computer chips. These positive feedback loops also embed first-mover advantages into the system, creating path-dependent gains that grow harder to dislodge as technologies interconnect and co-evolve.17

Technological convergence complicates efforts to govern or forecast the impact of critical and emerging technologies. It also means that countries seeking great power status must maintain an edge across a constellation of critical and emerging technologies.18 This does not mean that smaller states are out of the game. The countries that build on their strengths and coordinate with partners abroad can secure lasting economic prosperity and security within their regions or geopolitical blocs. For example, policymakers in Ottawa have helped Canada become a quantum powerhouse: although it represents just 0.5% of the world’s population, the country is home to five percent of global quantum talent, has authored over 1,000 of the 75,000 quantum research papers published on arXiv in 2023, and has committed $360 million Canadian dollars through its 2023 National Quantum Strategy to support talent development and international collaboration in quantum sensing, computing, and communications.19

Still, managed or emergent interdependence comes with external risks. Exogenous shocks—such as global pandemics or interstate wars—can abruptly sever cross-border supply chains, leaving countries that specialize too narrowly unable to secure critical inputs or export goods and services. To mitigate these risks, many governments are reshoring specific industries, friendshoring to allies and partners, and tightening export controls on critical and dual-use technologies. These changes are unfolding in both global and regional contexts; after all, most trade and investment is heavily regional, and so-called ‘global’ supply chains rarely stretch end to end.20 These are often used within broader national strategies to balance cost efficiency and resilience. Still, the challenges of enforcement, tensions between competition and innovation, and the complexity of global trade networks mean that no single policy can address every risk; tradeoffs are unavoidable.21 Governments must strike the right balance in how they use these tools.

While this Index and Report map the global landscape of critical and emerging technologies, they do not account for shorter-term developments. As technology evolves, the way that sectors and cross-cutting pillars are assessed should evolve with it. Readers should use the flexible modeling feature of the Index Dashboard to adjust weights, challenge underlying assumptions, and test different analytic inputs.

Artificial Intelligence

Background

Artificial Intelligence (AI) describes the ability of computers and machines to execute tasks that normally rely on human cognition: analysis, inference, problem-solving, interpretation, and decision-making. The development of AI models generally follows several key stages. After defining the task, data scientists collect, preprocess, and format relevant data. Engineers select or develop an appropriate algorithm based on the task and data type—whether supervised, unsupervised, or reinforcement learning—and pair it with a fitting model architecture. The model is then trained, evaluated, and tested on this data. This results in a version of the model ready to be deployed; the performance of the model, however, still needs to be regularly monitored and updated with new data over time.22

The current race for AI dominance, driven by both states and private firms, is about more than just computing power. AI is becoming a foundational capability across all sectors of society, boosting productivity and augmenting human labor and decision-making. In 2018, the U.S. National Security Commission on Artificial Intelligence stated that “AI systems will… be used in the pursuit of power,” and political leaders and scholars increasingly frame the development of AI systems as an integral competition shaping the future of governance and the balance of power in the years ahead.23

U.S. firms such as OpenAI, Google, and Anduril are leading in the development and employment of advanced AI systems, creating state-of-the-art models for applications ranging from language and data analysis to autonomy and robotics.24 In China, companies such as DeepSeek are setting new standards in cost efficiency, lowering development expenses through lean model architectures and optimized training pipelines.25 European firms, including France’s Mistral—best known for its open-source large language models—are also propelling innovation and contributing to European AI governance initiatives centered on transparency, ethical design, and regulatory compliance.26 Together, these international forces fuel a global market characterized by research and increasing adoption of AI systems for different commercial and military applications.

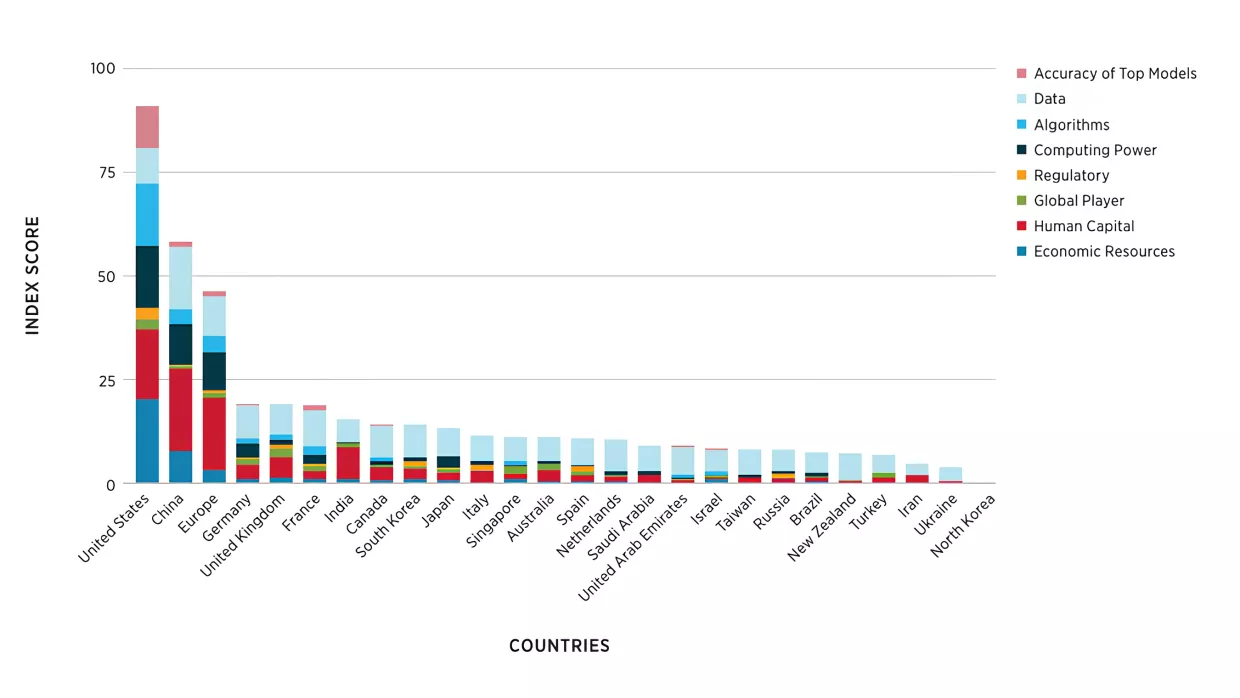

This report’s analysis of AI is based on eight pillars. The greatest weights were assigned to the Economic Resources and Human Capital pillars, since funding and skilled personnel form the bedrock of any AI ecosystem. Technical factors captured in the Algorithms, Computing Power, Data, and Accuracy of Top Models pillars are also crucial as determinants of AI performance and efficacy. Complementing these technical foundations, the Global Player and Regulatory pillars track the institutional environment shaping AI advancement, though with lower weights to acknowledge their supporting, rather than foundational, influence on AI capabilities.

Key Judgments

1. The United States is ahead in AI, with China and Europe roughly tied in the second tier. While China maintains an absolute lead in human capital and data and is far ahead of Europe in economic resources, it fares similarly to Europe in terms of computing power and algorithms.27 The result for overall scores is a far greater gap between the United States and China compared to China and Europe.Data, compute, and human capital largely determine competitive advantage—nations that amass quality datasets, deploy computing resources efficiently, and develop AI talent can leap ahead of other countries. Meanwhile, mid-tier and lower-ranked countries consistently struggle with minimal research and development, creating persistent bottlenecks to innovation and deployment.

2. The United States has a considerable advantage in AI, but China has made significant progress and enjoys unique advantages that will challenge the American AI lead in the next decade. The United States dominates in terms of its economic resources, computing power, and algorithms, while China leads in terms of data and human capital. The 2025 release of DeepSeek’s R1 model and Alibaba’s Qwen3 family of models, however, demonstrated that the U.S. lead in AI may be more vulnerable than previously assumed.28 Maintaining a lead in AI demands ongoing attention and financial commitment to develop, adopt, and integrate systems across both commercial and government applications.29 The great progress China has made in AI over the last two years, particularly with regard to model performance and cost-optimized training, underscores the importance of not only pioneering key technologies but also leveraging initial progress to advance growth in a variety of industries.30

3. Europe’s strength in AI is largely derived from human capital, but the region trails in algorithms, computing power, and economic resources. Fragmented innovation among national startups limits scalability compared to Silicon Valley, and although Europe has large amounts of raw data, European Union data protection regulations complicate large-scale model training.31 Without the establishment of greater incentives for cross-border commercial growth, coordinated initiatives such as a pan-European AI Moonshot Fund, or a more favorable regulatory environment, Europe risks continuing to export ideas while importing commercial models, marginally shaping the governance of AI without capturing the strategic value of adopting and integrating AI systems.

Additional Findings

The United States excels in terms of its large number of AI models with high accuracy; France and China follow, albeit at a considerable distance. U.S. models consistently outperform other countries’ models in mean win rate—the proportion of times a model performs better than others across a myriad of tests in subjects such as literature, media, science, and math.32 This performance edge is reinforced by the volume of accurate U.S.-based models, widespread user access, and strong underlying data pipelines. Together, these elements create a self-reinforcing cycle of model effectiveness, also aiding the integration and use of AI models by both government and commercial customers.

Countries with strong human capital or data but limited computing power harbor unrealized AI potential. For example, India and Brazil’s limited computing power are currently holding them back from taking advantage of their strengths in human capital and data. The increasing availability of cloud-based graphics processing units and open-source models, however, could help accelerate their progress in AI. How quickly these countries can advance is partly contingent on the policies the Trump administration develops to replace the Biden administration’s U.S. Regulatory Framework for AI Diffusion.33

China dominates in raw human capital for AI, followed by Europe, the United States, and India. Though the data used to calculate human capital in this Index represent the number of high-impact scientific publications rather than per capita measurements, scale still matters: a larger pool of competent individuals increases the chances of cutting-edge innovation and startup proliferation. Irrespective of disparities in compute access or regulatory readiness, this sheer volume of skilled personnel helps drive indigenous research output, model training, and domestic applications for commercial and government use.

Cloud computing infrastructure is fundamental to the development and deployment of AI systems, yet it remains difficult to measure. The United Arab Emirates is a prime example; while Abu Dhabi currently has relative weaknesses in terms of measured venture capital investment in AI, the emirate actually controls substantial computing power through G42, challenging conventional methods of assessing the economic resources ultimately being channeled toward AI development and deployment.34 Without policy approaches that adequately address cloud computing, current export control measures will likely fall short of their enforcement goals and objectives. Indeed, the U.S. Regulatory Framework for AI Diffusion attempts to address this gap, but without detailed intelligence on cloud-based AI computing operations and substantial penalties for compliance violations, Western powers will struggle to control the proliferation of advanced AI systems, especially among competitors and adversaries.35

No actors beyond the United States, China, and Europe have a full-spectrum AI stack, but other nations can still build meaningful advantages in AI through vertical or regional specialization. Displacing the United States, China, and Europe would require large, simultaneous progress in computational power, economic resources, and algorithms; this is an immensely difficult task for any single nation. China has yet to field viable alternatives to the dominance in graphics processing units and software that Nvidia (with its proprietary architecture) and Taiwan Semiconductor Manufacturing Company provide for the United States.36 Yet the modular structure of AI value chains—spanning data pipelines, foundation models, and domain-specific fine-tuning—creates opportunities for influence without comprehensive AI capabilities. Countries that are neophytes to the AI race can invest in their strengths to carve out durable niches, influencing global standards and capturing outsized benefits in terms of productivity in the private sector and government. Examples include Japan and Germany in robotics-AI integration, Canada in developing safety and alignment tools for industrial equipment, and Brazil in agricultural data.

Biotechnology

Background

Biotechnology refers to the systems enabling the modification of living organisms and their components for specific applications. While human societies have long used biological processes, such as fermentation and selective breeding, breakthroughs in the late 20th and early 21st centuries—such as the development of mRNA platforms and CRISPR-Cas9—have expanded biotechnology into a field capable of reprogramming life at its fundamental level.37 Today, biotechnology spans several domains: genetic engineering (altering nucleic acids through techniques such as gene editing); bioprocess engineering (using organisms to produce goods by leveraging metabolic pathways); biomolecular analysis and engineering (analyzing and manipulating biological molecules); environmental biotechnologies (employing living systems to clean or enhance ecosystems); and synthetic biology (designing entirely new biological parts or systems).38

Governments need biotechnology to understand and enhance the health of their societies.39 Their most visible applications span medicine, agriculture, energy, and sustainability; for instance, mRNA vaccines, aquaculture, and the development of bioengineered fuels. The COVID-19 pandemic demonstrated how nations with advanced biotechnology capabilities were able to better protect themselves: rapidly sequencing the virus, developing diagnostics, and deploying vaccines. This technological edge is contingent on the integration and convergence of different technological ecosystems, such as bioinformatics, AI, and high-throughput computing.40 These synergies are simultaneously accelerating the discovery of new biological compounds and widening the gap between nations that can integrate these tools and those that cannot. The growing accessibility of biotechnology also elevates the risk of accidental or deliberate misuse. In this respect, governments and private firms around the world are becoming more cognizant of the need to manage the risks that biotechnology poses; as much as biotechnology can be used to cure diseases, it can also be used to facilitate the creation of new and deadly pathogens.

Governments, companies, and research institutes are currently shaping the future of biotechnology. China’s BGI Group has grown from its origins as a small state-backed research institute into a far-reaching genomics powerhouse that now has a diversified portfolio in everything from animal cloning to diagnostic testing.41 Across the Pacific, American firms such as Moderna and Colossal Biosciences have introduced new innovations in genetic engineering, the former notably introducing a COVID-19 mRNA vaccine authorized for use in the United States in December 2020.42 Europe hosts its own biotechnology giants, including Germany’s BioNTech and Switzerland’s Novartis.43 The industry’s shifting global dynamics became particularly evident when Monsanto, once a dominant American agrochemical and biotechnology firm known for genetically engineered crops, fell under German ownership after Bayer AG acquired the company in 2018.44

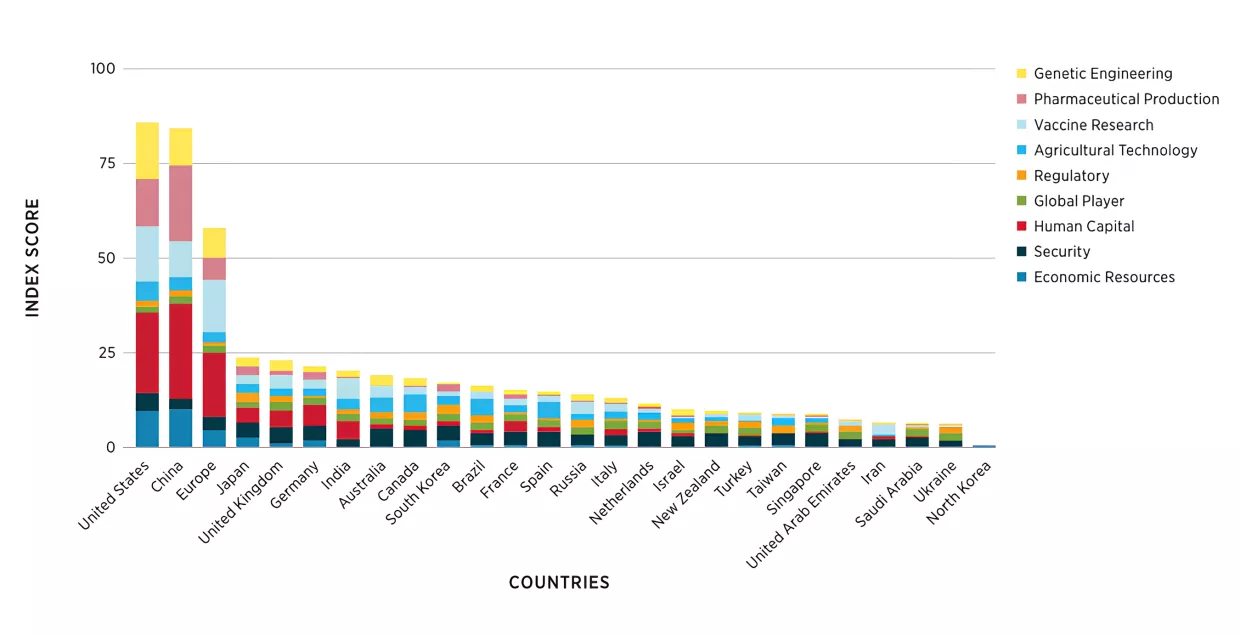

This report’s analysis of biotechnology is based on nine pillars. The greatest weights Analysis in this sector prioritizes Human Capital, Economic Resources, and other pillars representing key aspects of biotechnology capability (Pharmaceutical Production, Genetic Engineering, and Vaccine Research) with the highest weights. This is because of these pillars’ direct impact on innovation and crisis response, as demonstrated during the COVID-19 pandemic. Lower weights were placed on Agricultural Technology, Security, and the pillars representing aspects of biotechnology governance (Global Player and Regulatory) because they do not directly reflect the advancement and diffusion of these technologies.

Key Judgments

1. Among the technologies examined in this Index, China has the most immediate opportunity to overtake the United States in biotechnology; the narrow U.S.-China gap suggests that future developments could quickly shift the global balance of power. The United States and China perform similarly in biotechnology overall, with China’s strengths underpinned by its human capital.The United States excels in security, genetic engineering, vaccine research, and agricultural technology, bolstered by private-sector innovation and public-private partnerships. China has dominance in pharmaceutical production through extensive, large-scale public investments and state-backed manufacturing.

2. Cross-national gaps in human capital, pharmaceutical production, genetic engineering, and vaccine research highlight these areas as bottlenecks to building biotechnology power. These four areas show the highest variance among all measured pillars in the biotechnology sector and, based on the weighting used in this analysis, collectively contribute 75% to the total sector score.45 Advanced research cannot be developed or applied for real-world solutions without the necessary workforce or a strong biomanufacturing base, just as expertise in genetic engineering and vaccine development is essential for the rapid innovation needed during health emergencies such as the COVID-19 pandemic.

3. Europe trails the U.S.-China biotechnology duopoly not for lack of potential, but due to decentralized institutions and under-leveraged resources. While Europe performs well in vaccine research and security and reasonably well in human capital, the region continues to lag behind the United States and China, particularly in economic resources and pharmaceutical production. To avoid falling further behind and reach its full potential in the bioeconomy, Europe must strengthen the European Union Single Market, better integrate with non-European Union partners, coordinate cross-national public funding efforts, and implement centralized pathways for approving the testing and deployment of biotechnologies.

Additional Findings

Significant private sector funding provides the capital needed to make Japan a rising leader in the field; however, it struggles at the moment to turn this capital into biotechnology products. Japanese private-sector funding in biotechnology is nearly triple that of the United Kingdom and about double that of Germany, suggesting a healthy appetite in the country for startups and innovation. Given this large quantity of capital, however, Japan does not have a proportional lead in vaccine research, pharmaceuticals, and genetic engineering. This points to a bottleneck between investment and outcomes, stemming from regulatory delays, weak systems for technology transfer, risk-averse funding, and siloed industry actors—challenges that Japan needs to address to better translate biotechnology research into real-world therapies and products.46

Japan’s regulatory environment is uniquely amenable to rapid approval for human-based research, which is unusual compared to other nations with notable achievements in gene editing. The United States and the United Kingdom, for example, have placed high restrictions on human gene editing that only permit it in exceedingly rare cases. Germline gene therapy, specifically, is entirely prohibited in the United States. Meanwhile, stem cell therapy research has been accelerated by government-led national strategies to promote quick transitions to clinical trials since 2011 in Japan.47 Some of this pointed interest may be partially explained by Japan’s extreme demographic aging, which both domestic and international investors view as a unique research catalyst.48

South Korea has not yet converted its large public and private capital into equivalent biotechnology strengths, but this is a nation to watch, given Seoul’s renewed interest in the sector. Despite possessing one of the highest amounts of private sector funding, in addition to high government funding, South Korea has produced weaker research power compared to other similarly funded countries. In 2023, the South Korean government released several plans to improve the country’s biotechnology industry, particularly as related to agricultural biotech—new initiatives are likely in development.

Australia’s high score reflects years of targeted reforms to build a layered, risk-based biosecurity system; still, rapid response remains a persistent weakness both in Australia and worldwide. Canberra’s strength in early detection and reporting of epidemics contributes significantly to its biosecurity performance, accounting for over a quarter of its sector ranking in the Index.49 Other Western governments can take a page from Australia’s playbook of steady legislative reform and cross-sector coordination—evident in the establishment of the Health Protection Principal Committee in 2009, the passage of the Biosecurity Act in 2015, and release of its National Biosecurity Strategy in 2022.50 Yet all countries, including Australia, still fall short in their rapid response capabilities. Governments worldwide need to do better by conducting more comprehensive exercises, developing and deploying new risk communication mechanisms, and strengthening links between public health and security authorities.51

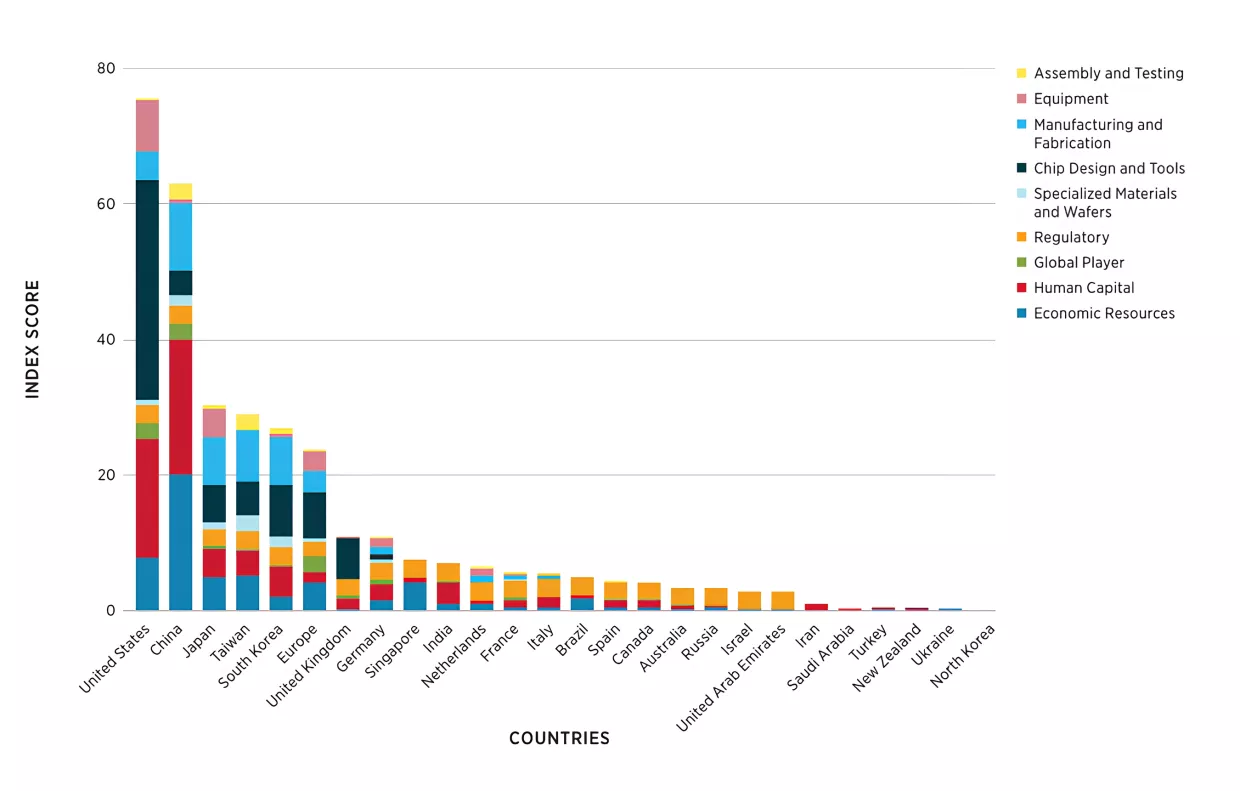

Semiconductors

Background

Semiconductors are materials that can conduct or block electrical current, though the term commonly refers to integrated circuits—compact chips containing transistors, resistors, and capacitors.52 These chips form the foundation of all modern computing systems by enabling the processing, storage, and transmission of data.53 The manufacturing of semiconductors relies on a series of highly specialized ecosystems and firms, starting with the advanced software and design needed to fit billions of transistors onto a chip. Then there are the actual silicon wafers themselves, along with the complex equipment that carves designs onto them. This is followed by the formation of transistors by fabrication facilities, using processes and techniques refined over decades and through the investment of billions of U.S. dollars in research and development. Lastly, the chips are packaged and distributed to device manufacturers for use in smartphones, vehicles, and other electronic devices.54

Although the complexity of the semiconductor supply chain ensures that they will remain part of a globally integrated industry, governments have increasingly come to view them as a critical aspect of national security. Recent geopolitical shocks have revealed the world’s heavy reliance on semiconductors and the vulnerability of its interwoven supply chains.55 Moreover, escalating U.S.-China tensions and Beijing’s increasing belligerence towards Taipei have prompted governments and companies to assess the risk of aggression against Taiwan—home to the Taiwan Semiconductor Manufacturing Company, which manufactures 70-90% of the most advanced transistors.56 At the same time, the race for more powerful AI capabilities has driven demand for advanced chips, particularly graphics processing units, thousands or even millions of which power the data centers used to train AI models.57 Indicative of this massive demand is the U.S. firm Nvidia, which produces high-end graphics processing units and saw its market capitalization more than triple from January 2023 to January 2024.58

Semiconductors have become a strategic priority for the United States since the Biden administration’s first series of expansive export controls targeting China in October 2022.59 Countries aim to have domestic control over semiconductors, spanning legacy and high-end devices, to protect themselves in case of foreign catastrophe.60 Washington and Beijing also want high-end chips to develop the AI systems both see as essential for gaining the upper hand in their intensifying security competition. Through U.S. export controls, Washington has leveraged its strengths in design and manufacturing equipment, alongside partnerships with Japan and the Netherlands, to limit China’s access to cutting-edge semiconductors. At the same time, many countries—China most notably—have shown that state subsidies and guidance are essential in fostering domestic industry amidst global competition.61

This report’s analysis of semiconductors is based on eight pillars. The greatest weights are assigned to Chip Design and Tools, Economic Resources, Human Capital, and Manufacturing. This is because these pillars represent the critical bottlenecks: sophisticated design software enables cutting-edge architectures, massive capital investment funds necessary facilities and critical infrastructure, specialized talent drives innovation, and advanced manufacturing techniques determine production quality and yields. Less weight is given to Equipment, Assembly and Testing, Specialized Materials and Wafers, Global Player, and Regulatory pillars to reflect their supporting role for a country’s semiconductor capacity.

Key Judgments

1. No country has complete, end-to-end control of a supply chain for advanced semiconductors. The United States excels in chip design and tools, as well as equipment, but lags in manufacturing and fabrication. China leads in economic resources, assembly and testing, and manufacturing and fabrication, with a significant edge in the mining and refining of the inputs for materials and chemicals. However, China remains relatively weak in equipment, specialized materials, and wafers.62 Taiwan dominates in specialized materials and wafers as well as manufacturing and fabrication, but depends on foreign equipment. Japan and South Korea are both strong in human capital, chip design and tools, and manufacturing and fabrication, but leading firms in both countries remain heavily reliant on the Chinese market.63

2. The dominance of the United States, Japan, Taiwan, and South Korea in semiconductors persists at critical chokepoints of the supply chain: advanced manufacturing and fabrication, chip design and tools, and equipment. These pillars have the greatest variance among all included in this Index due to high costs and technical barriers. While many countries are investing heavily to close these gaps, capital alone is unlikely to be sufficient to establish an end-to-end semiconductor production capability; if countries aim to break free from dependence on the current leaders, they will need to simultaneously secure equipment and design intellectual property.

3. Although China leads other countries in chip manufacturing by site capacity, it faces extreme challenges in overtaking global leaders Taiwan and South Korea in advanced chip manufacturing. Historically, countries that lead in advanced chip manufacturing have only been usurped when other countries already established in lower-end chip manufacturing make innovative breakthroughs.64 While China has lower-end chip manufacturing experience and lower operational costs than Taiwan and South Korea, it is trying to achieve breakthroughs in multiple segments of the industry while also being subject to U.S. restrictions on using leading designs or equipment—an unprecedented battery of barriers. Assessing China’s progress is hard, however, because U.S. export controls incentivize Chinese firms to downplay their advancements.65

Additional Findings

Countries that lead in semiconductor power have invested the most to keep their firms in the lead. After China and the United States, the countries that have pledged the most public funding for domestic semiconductor investment currently dominate the semiconductor value chain: Japan, South Korea, and Europe (led by Germany), with Taiwan ranking lower but still high among all 25 countries. Japan has announced over $11 billion U.S. dollars in subsidies for Rapidus, its domestic semiconductor startup aimed at producing leading-edge chips by 2027.66 South Korea last year published its plan to build the largest semiconductor cluster by 2047 and is investing in both its traditionally dominant sector of memory as well as logic, where Taiwan’s firms now lead.67 The European Union’s European Chips Act will mobilize around $20 billion U.S. dollars to attract foreign firms and promote domestic ones.68 Government support has always played a role in semiconductor power—something that the leading states recognize.

The United States’ semiconductor strengths were built up in a globalized economy, but export controls challenge this model. American producers of semiconductor manufacturing equipment, in particular, have suffered as U.S. export controls have limited access to the China market. While the cutoff from Chinese firms has also affected chip design firms—the sector of the semiconductor industry the U.S. most dominates in—the boom in sales of AI chips has more than recompensed leading design firms’ losses. Equipment manufacturers must wait longer to recoup losses since their customers, chip manufacturers, shop less frequently than chip manufacturers’ customers do. U.S. equipment manufacturers’ reliance on Chinese sales has fueled their opposition to export controls and strengthens the case for an American “tech fund,” which would share initial risk and support diversification away from China.69

Nvidia and Applied Materials Under U.S. Export Controls

The fates of U.S. chip design firm Nvidia and toolmaker Applied Materials illustrate the uneven impact of U.S. semiconductor export controls since October 2022. Between November 2024 and January 2025, Nvidia’s data center revenue grew 93% year-on-year, while full-year revenue rose 142%. Applied Materials, by contrast, posted a record quarter for the same period by growing just 7% year-on-year.70 This gap largely reflects Nvidia’s extraordinary growth over the past 18 months and underscores that soaring demand for AI chips does not translate into equivalent growth in demand for chipmaking tools.

Still, recent U.S. export controls have arguably impacted Nvidia more than Applied Materials. In April 2025, the U.S. government announced that Nvidia would need licenses to export its H20 chip to China. Nvidia projected a $5.5 billion loss from this restriction—about 4.2% of its revenue of $130.5 billion U.S. dollars in fiscal year 2025. By comparison, Applied Materials estimated that export controls introduced at the end of the Biden administration cost it approximately $400 million U.S. dollars in China-related revenues, roughly 1.5% of its $27.6 billion U.S. dollar revenue for the year ending January 31, 2025.71 This is despite the fact that U.S. export controls on Nvidia-designed AI chips have not been airtight; for example, as first reported in October 2024, Huawei obtained controlled chips from the Taiwan Semiconductor Manufacturing Company through a third-party Chinese chip design firm.72

India is working to establish itself as a semiconductor manufacturing hub, leveraging its market size and labor force, but still lags behind leading states in critical infrastructure. Though ranking below established players in semiconductor power, the Modi government has put money and effort into the industry since declaring its aim in April 2022 “to establish India as one of the key partners in global semiconductor value chains.”73 India, already responsible for one-tenth of global chip consumption, wants to become less reliant on foreign suppliers as domestic consumer demand for chips rises. It is also growing more attractive for firms looking to shift production away from China, given its rising labor costs and geopolitical tensions with the West.74 Even though India hosts only 7% of chip design facilities, it has nearly 20% of the world’s design engineers (many working for U.S. or European firms). New Delhi has subsidized a semiconductor park in Dholera, Gujarat, as well as foreign low-end chip manufacturing and assembly, test, and packaging operations in India in the hope that India can grow their expertise in new segments of the semiconductor supply chain, but packaging leaders China, Taiwan, and Malaysia maintain a critical lead in public infrastructure.75

Germany, the biggest semiconductor power outside of the United States and East Asia, maintains chip manufacturing leadership in the European Union because of its leading role in other manufacturing-heavy industries. Germany already manufactures many of the European Union’s chips and relies heavily on legacy chips for its auto industry.76 Berlin has recently offered more subsidies to foreign semiconductor firms to make advanced chips at home as part of the European Union’s push to reduce exposure to faraway producers in East Asia, with a goal of doubling the European Union’s market share in chip production from 10% to 20% by 2030.77 The prospect of making chips alongside German automotive and advanced equipment customers is attractive, but recent delays in proposed U.S. and German fabrication facilities call into question how badly manufacturers want to set up in Germany. Following the February 2025 election, Germany’s new coalition government faces critical decisions regarding semiconductor subsidies, with significant uncertainty about future funding.78

Singapore, like Germany, is using its comparative and geographical advantages to maintain a strong position in global semiconductor markets and expand into new segments. Due to methodological limitations, Singapore’s performance in fabrication and packaging is not reflected in the Index.79 Yet for its size, Singapore commands substantial global market shares in chip manufacturing and semiconductor manufacturing equipment. Leaning on its highly skilled workforce, existing capabilities in chipmaking, and convenient location for distribution to East Asian producers, its government has rolled out training programs as well as tax incentives and refunds in the last few years to move into chip design and advanced packaging, two other segments of the supply chain.80

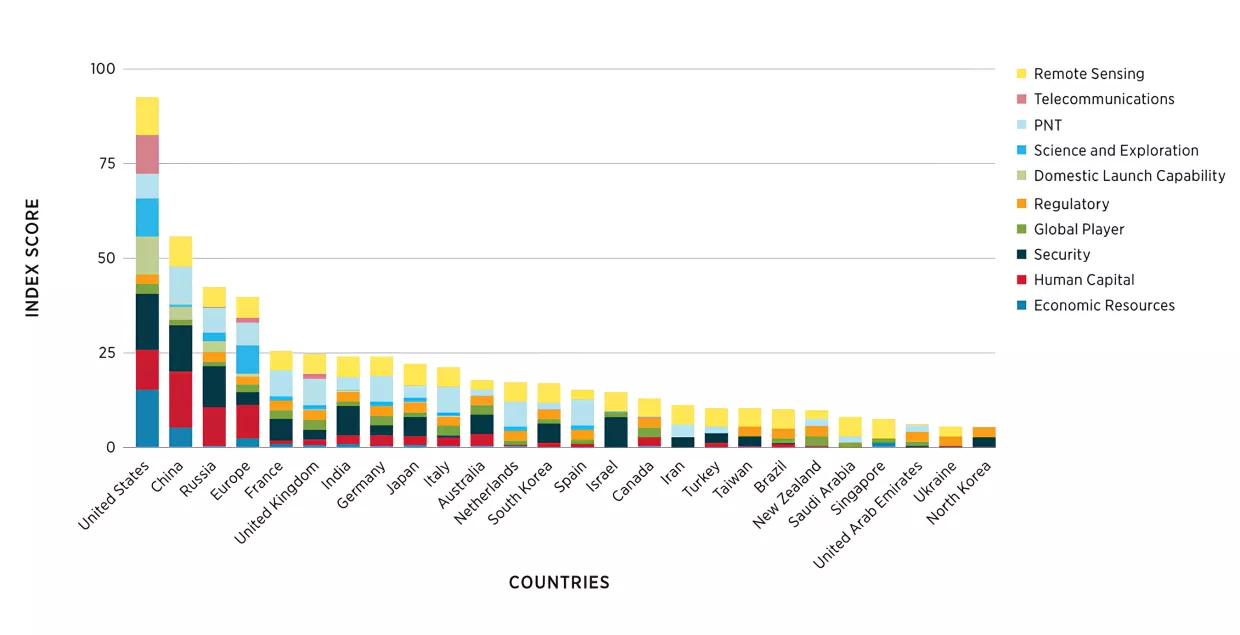

Space

Background

Space technology encompasses the systems that enable access to, operations within, and utilization of the space environment. The development of powerful rockets in the mid-20th century initiated physical space exploration, ushering in the current era of geopolitical competition, scientific discovery, and commercial opportunity.81 Space technology can broadly be divided into two categories. The first includes foundational technologies that make access to and activity in space possible, such as launch systems, propulsion, power generation, and re-entry vehicles. The second includes technologies that capitalize on space’s unique properties—from satellites that direct terrestrial radio navigation to space-based infrared sensors that observe the Earth and distant galaxies.

Governments now turn to space-based systems for a strategic edge, much as they once turned to new maritime technologies during the Age of Sail and aeronautical technologies in the early 20th century. Space can provide military advantage, support modern economies, advance science and scientific leadership, and underpin policy agendas to shape the future of international governance.82 Policy leaders and military commanders rely on space-based assets—from communications satellites to missile-warning systems—for command and control, as well as intelligence, surveillance, and reconnaissance. In this respect, military capabilities in space are important not only for fighting wars, but also for deterring them. Commercial space services, including navigation, timing, and Earth observation, constitute critical infrastructure and fuel growth across a myriad of economic sectors. On the scientific front, exploration missions and research in both pure and applied science lay the groundwork for discovery and the advancement of dual-use technologies, including in robotics, advanced materials, and remote sensing. Diplomatically, engagement in new international forums and agreements presents an opportunity for countries to shape the rules and institutions governing how societies engage with space, the final physical frontier for humanity.

Governments, multinational programs, and private ventures now share the stage in driving space activity. In the United States, NASA partners with private firms such as SpaceX—pioneering reusable rockets and the Starlink broadband constellation—while the U.S. national security establishment flies and increasingly relies on a mix of military and commercial satellites.83 China has stepped up its launch schedule and set its sights on the Moon, backed by private ventures such as iSpace.84 It has also independently launched and currently operates Tiangong, a permanently crewed space station in low Earth orbit. While Moscow’s prominence in space has faded since the Soviet era, Russia’s Roscosmos continues to operate crewed Soyuz missions and sustain its longstanding presence in orbit.85 Europe continues its activities in space through the European Space Agency, which pools resources from 23 member states to field the Ariane series of space launch vehicles.86 Meanwhile, private companies worldwide, such as Eutelsat OneWeb’s satellite broadband network, are introducing new sources of commercial innovation into the space industry.87

This report’s analysis of Space is based on ten pillars. The greatest weights have been assigned to Economic Resources, Human Capital, and Defense and Security Assets. The pillars Domestic Launch Capability; Positioning, Navigation, and Timing; Science and Exploration; Telecommunications; and Remote Sensing pillars are all weighted slightly lower. This reflects their critical roles in enabling independent access, strategic services, and innovation. Global Player and Regulatory each have the lowest weights; after all, leadership in multilateral forums and strong legal frameworks support—but do not drive—a country’s overall competitiveness in space.

Key Judgments

1. The American private sector drives the United States’ strong lead in space, though its vulnerabilities in orbit to Chinese and Russian military capabilities increase strategic risk. Washington’s edge stems from productive public-private partnerships that have helped the United States dramatically increase its launch frequency and payload capacity while reducing per-mission costs. American public-private collaborations also strengthen the United States’ human capital, telecommunications, and economic resources. However, the United States is asymmetrically vulnerable in space, relying heavily on space-based systems for military operations and for supporting critical sectors of the American economy. China and Russia are also fielding formidable anti-satellite capabilities, offsetting the United States’ lead in space and increasing its strategic exposure.

2. A large capability gap distinguishes the top three space powers—the United States, China, and Russia—from all other nations. The United States has a clear overall edge in space, followed by China with its ambitious state-led programs and burgeoning commercial space development. Russia occupies the third position in the Index, though much of its strength comes from Soviet-era systems and infrastructure rather than new innovation. Europe ranks fourth, followed by India, whose remarkable progress has enabled it to compete with legacy space powers through increasingly complex missions.88

3. Wide gaps in human capital, remote sensing, and position, navigation, and timing indicate that these three areas are the main bottlenecks to building space power. There is little variation in pillar scores measuring regulatory and legal frameworks, as well as participation in global norm-setting. Likewise, economic resources alone are not enough; major investments only translate into launch infrastructure, for example, when paired with sufficient human capital and research and development. On the contrary, the wide variance in countries’ systems based in orbit (such as satellites for position, navigation, and timing) demonstrate that these are among the hardest capabilities to acquire; they often require indigenous launch capability, management over sensitive and classified payloads, and resilient ground-based networks capable of facilitating data transfers in austere conditions.

Additional Findings

By pooling Europe’s resources, the European Space Agency significantly influences the global balance of power in space. Individually, countries such as France, Germany, and the United Kingdom fall behind global leaders, but the combined capabilities of European countries are almost on par with those of Russia and approach those of China. Europe’s strength is in telecommunications, as well as science and exploration, although it falls short in terms of security and domestic launch capability. These weaknesses compel European states to rely on foreign space launch systems. Closing these shortfalls will require more extensive collaboration to develop reusable, indigenous launch systems, as well as coordinated European security initiatives.

The United States and Russia retain a lasting advantage from their early space race, which continues to underpin their dominance in science and exploration. American space missions demonstrate an unmatched range and depth, while Russia and the former Soviet Union similarly achieved a high volume of missions, many during the 20th century. Although emerging players such as India and China are advancing notable missions—such as the Chandrayaan-3 and Chang’e-6 lunar probes, respectively—the institutional memory and established capabilities of legacy programs continue to confer decisive advantages, given their decades-old, world-class ground and launch infrastructure, extensive archives of mission data, and deep pools of specialized talent. As the scientific landscape broadens and drives greater international collaboration, the United States and Russia will nevertheless maintain a unique advantage.

Regionally, Asia presents more potent individual players. While many European countries ranked within the top half of the Index, most countries' scores are aided by European Space Agency achievements rather than domestic ones, whereas China, Russia, India, Japan, and South Korea all possess strong independent space programs with high scores.

Ukraine’s low ranking reflects the current state of conflict in the nation and the consequences of intertwined space partnerships. Historically, Ukraine has possessed a robust and active space program that launched several satellites into space; nearly all space activities have been brought to a halt as a result of the Russo-Ukrainian war and the loss of access to Russian facilities and supplies, and a presumed allocation of funds entirely towards the war effort. Other international partnerships have also been halted as a result of the conflict. This shows that human capital is not enough without access to manufacturing, fabrication facilities, and equipment.

Israel’s strengths in space disproportionately lie in its security capabilities. With its fleet of 12 military satellites and an arsenal of cutting-edge interceptors capable of targeting objects outside the atmosphere, directed energy systems, and jamming technology, Israel clearly prioritizes military applications in space over scientific endeavors. This specialized focus limits Israel’s overall ranking, despite significant strength in the security domain.89

Despite ranking at the bottom of the Index, North Korea’s increasing activities in space demonstrate that it possesses notable capabilities in space. Pyongyang’s public commitment to space development and technological partnership with Russia resulted in four launch attempts in 2023 and 2024; however, since the Index only includes successful launches, North Korea received just one launch count. This, combined with a general lack of public data available on North Korea, potentially leads to an underestimation of North Korean space capabilities within this Index.

Iran has focused on building homegrown space surveillance and navigation systems to support its strategy of technological autarky. Despite near-zero scores in economic resources and human capital, Tehran has been funneling talent and scarce funding into its space surveillance and positioning programs. And with the launch of the Islamic Revolutionary Guard Corps’ Noor satellites and deployment of the Russian-built Khayyam Earth-observation platform, Iran now ranks with Taiwan and the Netherlands in remote sensing. Though diminutive in the overall space sector data as of now, Iran’s pursuit of security and modernity—along with deepening ties to Russia, China, and North Korea—could fuel the future growth of its indigenous space capabilities.

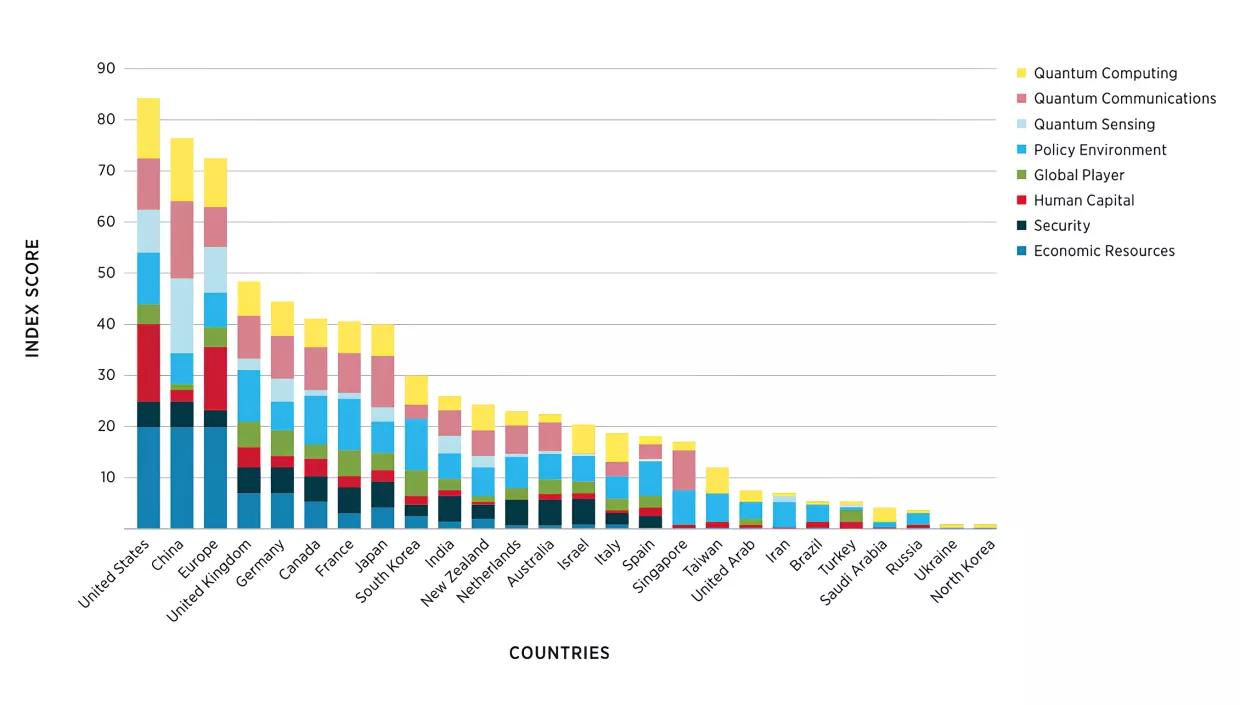

Quantum

Background

Quantum technology refers to systems that harness quantum mechanics, the behavior of particles at the molecular, atomic, and subatomic levels. Scientists in the early 20th century discovered that, at the smallest scales, particles do not follow the rules of classical physics. Rather than acting as discrete entities with definable states, particles do not settle into one configuration until measured by an external observer; until then, they can simultaneously be in a multitude of configurations, a phenomenon known as superposition.90 Because of superposition, quantum processors with the ability to maintain coherent quantum states for sufficiently long periods of time can have the capability to pursue optimal computational paths in parallel rather than exhaustively checking every possibility, as needs to be done when using a classical computer. This could enable the employment of novel algorithms to solve previously intractable optimization and cryptographic problems.91 In addition, technologies that take advantage of superposition will likely enable extremely accurate computational simulations of complex systems, such as those involving molecules and materials, thereby facilitating new breakthroughs in the development of next-generation superconductors, batteries, and pharmaceuticals.92

Quantum technology also hinges on two other fundamental phenomena of quantum mechanics: entanglement and interference. Unlike classical physics, where interactions between objects rely on direct, local contact, entanglement describes the linkage of two or more quantum systems such that an action on one affects the other(s).93 Interference describes how the myriad of quantum possibilities can amplify or cancel each other out.94 For quantum computing, entanglement can connect systems so that they process information simultaneously, with interference being used to highlight productive computational pathways while suppressing vitiating alternative pathways.95 For quantum communication—characterized by ultra‑secure, low‑latency networks—entanglement provides the basis for methods of theoretically unbreakable cryptographic communications.96 And by using entanglement and interference to amplify genuine signal patterns and suppress random background noise, quantum technology will likely be fundamental to the next generation of sensing and metrology systems—for instance, stealth-defeating radars, ultra-precise atomic clocks, and long-range magnetic anomaly detectors.97

By introducing powerful new forms of computation, the nascent quantum revolution has the potential to disrupt the global balance of power. The United States has built its quantum advantage through a multi-pronged strategy: corporate innovation from firms such as IBM and Google, academic research at institutions such as MIT and Stanford, and federal investment through programs under frameworks such as the National Quantum Initiative Act.98 Through centralized development, China has built major quantum research centers, including the Hefei National Quantum Laboratory, while also launching the world’s first integrated quantum communication network.99 Furthermore, European nations are tapping into strong research institutions through collaborative initiatives such as the European Union’s Quantum Flagship.100 The international dimension of this field is illustrated by the U.K. startup Cambridge Quantum Computing merging with the US giant Honeywell to become Quantinuum, and the technological concept of “cat qubits” being instigated by the French firm Alice and Bob now being adopted by Amazon in the United States.101

This report’s analysis of Quantum is based on eight pillars. The greatest weights were assigned to Economic Resources, Human Capital, Quantum Communication, Quantum Computing, and Quantum Sensing. These pillars form the essential foundation and technical capabilities currently shaping a country’s potential to lead in the development and application of quantum technology. Although valuable for aligning national strategies and funding, the Policy Environment pillar was assigned less weight for this analysis compared to the technical domains, while the Global Player and Security pillars have the lowest weights due to their indirect influence on quantum development.

Key Judgments

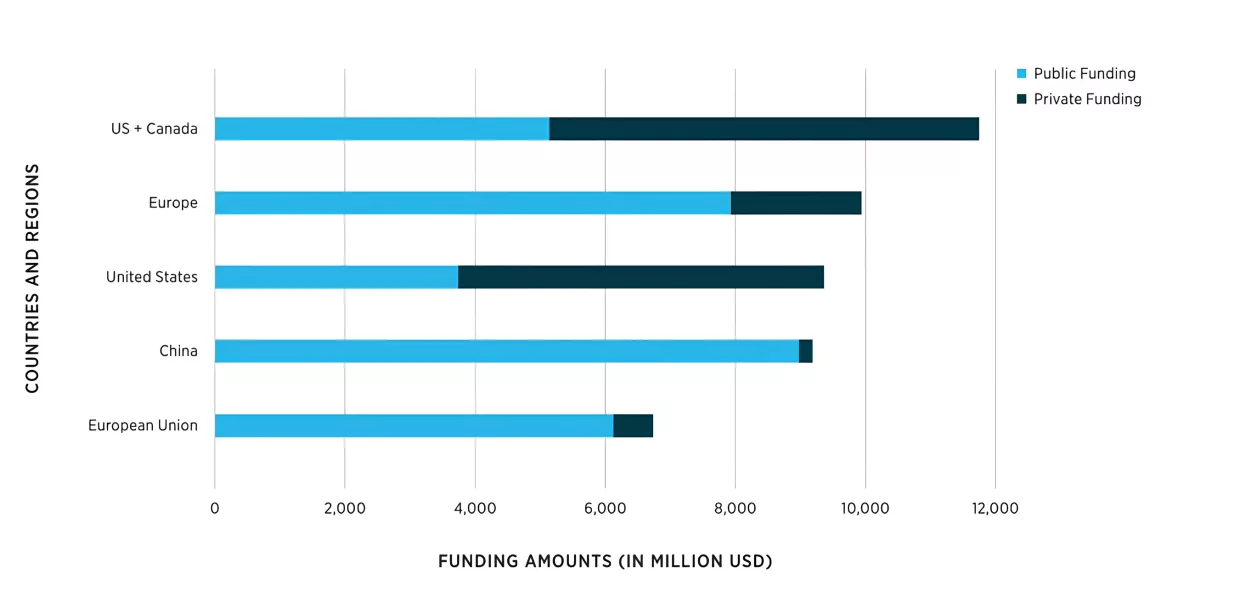

1. Quantum technologies remain in an early research phase, with current efforts focused less on deployment and more on advancing early-stage concepts. This is highlighted by the funding gap between quantum and other technology sectors; from 2008 to 2023, for example, American public and private investment in quantum technology totaled about $9.4 billion U.S. dollars—far less than the $52 billion U.S. dollars allocated under the CHIPS Act alone for semiconductor manufacturing, research and development, and talent development.102 This relative lack of investment has contributed to the fragmented and region-specific development of quantum ecosystems. In the United States and Europe, academia generates ideas and leads foundational research, startups enable emerging technologies to be explored which may be considered too high risk for large corporations, and large corporations carry out the engineering to scale up well-vetted technologies. China takes a state-led approach, which bridges research, development, and industry. In this context, progress in quantum technologies will largely depend on how countries open or restrict the flow of talent, tools, and ideas.

2. The United States, China, and Europe lead in quantum, though each draws strength from different areas. All three have strong human capital and substantial economic resources; each has invested over $9 billion U.S. dollars in quantum technologies, while all other countries remain at or below $3 billion U.S. dollars.103 China’s funding in quantum is primarily fueled by public investment. In the United States, funding is more evenly split between public and private sources, though large firms such as Alphabet and IBM remain the primary contributors. Europe has laid strong foundations for regional quantum growth and drives cohesion through Horizon Europe, the European Union’s research and innovation funding program, which now includes the United Kingdom again, as well as Turkey.104 If levels of funding prefigure future dominance, then the degree of Western unity—particularly the pooling of resources for quantum research, development, and deployment—will largely shape the global balance of quantum power.

3. Although the United States leads in quantum overall, China has a substantial edge in quantum sensing and communications. Beijing’s advantage in quantum sensing and communications is attributable to its prolific research output in these domains and its successful test of quantum communication technology in orbit.105 To close the U.S.-China gap in applied quantum, the United States and Europe must increase investment in applied research to lay the groundwork for more ambitious projects. This could include developing components for full-stack, multilayer quantum communication networks: technologies that catch and amplify weakened quantum states for long-distance transmission, portable ground units capable of sending and receiving entangled photons from satellites, and atmospheric-resilient networks designed to preserve quantum coherence despite interference from weather or light conditions.106

Additional Findings

The United Kingdom, Germany, Canada, France, and Japan each have roughly half the strength of the United States and China in quantum, but collectively they are well-positioned to influence the future of the field in meaningful ways. These countries share a similar profile: they are strong in quantum security, global governance, and domestic policy, but relatively weaker in terms of economic resources and human capital. They are also democracies integrated into the U.S. alliance architecture, with similar domestic institutions and strong, interlinked academic networks. These shared strengths position them to develop joint quantum infrastructure and shape technical standards for deploying quantum technologies. But to truly lead in quantum, these countries need more than just alliances and partnerships—they must carve out niches that make them indispensable to future quantum technologies and supply chains.

Economic resources, quantum sensing, and quantum communications show the widest disparities, underscoring that these areas are the main barriers to building a robust national quantum base. There is relatively little variation across countries in the pillars tracking engagement in global and domestic quantum policy. By contrast, economic resources, quantum sensing, and quantum communications vary widely across countries, showing how difficult it is for governments to develop or acquire these foundational elements of a viable quantum ecosystem. Indeed, there are very few countries that have amassed long-term public and private investment, high-quality research laboratories and programs, indigenously conducted foundational experiments, or developed prototypes of next-generation quantum systems. If states want to improve their quantum standing by spurring domestic growth, they need to develop and execute multilayered strategies built on a mixed assortment of policy tools: straightforward regulatory roadmaps, subsidies and tax credits for private firms, fast-tracked grants, and direct public investment in areas of core research and development.

France, Germany, the Netherlands, and the United Kingdom stand out for their highly collaborative quantum ecosystems. These countries are active participants in multilateral quantum research and development efforts such as the European Quantum Flagship, the International Council of Quantum Industry Associations, the Entanglement Exchange, and QuantERA. Given how nascent quantum technologies are, active participation in such organizations is especially critical. At this early stage, no single country possesses the full range of capabilities needed to achieve major breakthroughs independently. Collaborative research enables scientists to pool resources, compare findings, and accelerate progress across diverse subfields. The ability to engage in open, sustained scientific exchange will remain one of the most important accelerators of innovation as countries work to create practical and commercially viable quantum systems.

Recommended citation

Rosenbach, Eric, Lea Baltussen, Eleanor Crane, Ethan Kessler, Lukasz Kolodziej, Ethan Lee, Alexandre Meyer, Cynthia Tong, Britney Tran and Delaney Wehn. “Critical and Emerging Technologies Index.” June 5, 2025

Critical and Emerging Technologies Index

In this article

Footnotes

Kenneth N. Waltz, “The Emerging Structure of International Politics,” International Security 18, no. 2 (1993): 50, https://doi.org/10.2307/2539097; International Institute for Strategic Studies, “Chapter One: Defence and Military Analysis,” The Military Balance 125, no. 1 (2025): 6–11, https://doi.org/10.1080/04597222.2025.2445473; Joseph S. Nye Jr., Bound to Lead: The Changing Nature of American Power (New York: Basic Books, 2016); Joseph S. Nye Jr., Soft Power: The Means to Success in World Politics (New York: PublicAffairs, 2009).

Donald W. White, “The Nature of World Power in American History: An Evaluation at the End of World War II,” Diplomatic History 11.3 (1987), 181–202; Gavin Wright, “The Origins of American Industrial Success, 1879–1940,” American Economic Review 80, no. 4 (1990): 651–68, https://www.jstor.org/stable/2006701; John A. Thompson, A Sense of Power: The Roots of America’s Global Role (Ithaca: Cornell University Press, 2015), 4–8.

Stephen Kotkin, Stalin: Paradoxes of Power, 1878–1928 (New York: Penguin Books, 2015), 63.

Thomas P. Hughes, “Technological Momentum,” in Does Technology Drive History? The Dilemma of Technological Determinism, ed. Merritt Roe Smith and Leo Marx (Cambridge: MIT Press, 1994), 101–14; Henry John M. Culkin, “A Schoolman’s Guide to Marshall McLuhan,” The Saturday Review, 51–53, 70–72; G. John Ikenberry, A World Safe for Democracy: Liberal Internationalism and the Crises of Global Order (New Haven: Yale University Press, 2020), 14–15. A fuller treatment of the conceptual framework for measuring technological power is beyond the scope of this project, but it is important to note that there is a conceptual difference between innovation, application, and diffusion. For more, see Chris Miller, Chip War: The Fight for the World’s Most Critical Technology (New York: Scribner, 2022); Jeffrey Ding, “The Innovation Fallacy: In the U.S.-Chinese Tech Race, Diffusion Matters More Than Invention,” Foreign Affairs, August 19, 2024, https://www.foreignaffairs.com/china/innovation-fallacy-artificial-intelligence.

Critical and Emerging Technologies List Update, Fast Track Action Subcommittee on Critical and Emerging Technologies of the National Science and Technology Council, February 2024, https://www.govinfo.gov/content/pkg/CMR-PREX23-00185928/pdf/CMR-PREX23-00185928.pdf.

List of Critical Technologies in the National Interest: 2022 Update, Australian Government Department of Industry, Science and Resources, August 22, 2022, https://consult.industry.gov.au/critical-technologies-2022; Economic Security Critical Technology Development Program: Research and Development Vision (First Edition), Government of Japan Cabinet Office, 2022, https://www8.cao.go.jp/cstp/anzen_anshin/2_vision.pdf; Research and Development Vision (Second Version), Economic Security Critical Technology Development Program, Government of Japan Cabinet Office, August 28, 2023, https://www8.cao.go.jp/cstp/anzen_anshin/siryo1.pdf; UKRI Strategy 2022 to 2027: Transforming Tomorrow Together, UK Research and Innovation, March 17, 2022, https://www.ukri.org/publications/ukri-strategy-2022-to-2027/ukri-strategy-2022-to-2027/; “Emerging and Disruptive Technologies,” North Atlantic Treaty Organization, last updated August 8, 2024, https://www.nato.int/cps/en/natohq/topics_184303.htm.; European Innovation Council and SMEs Executive Agency, Identification of Emerging Technologies and Breakthrough Innovations, EIC Working Paper, January 2022, https://op.europa.eu/en/publication-detail/-/publication/7c1e9724-95ed-11ec-b4e4-01aa75ed71a1; Research and Innovation that Benefit the People: The High-Tech Strategy 2025, Federal Ministry of Education and Research, 2020, https://www.bmbf.de/SharedDocs/Publikationen/DE/FS/31538_Forschung_und_Innovation_fuer_die_Menschen_en.pdf; “Korea to Announce National Strategy to Become a Technology Hegemon,” Ministry of Science and ICT, October 28, 2022, https://www.msit.go.kr/eng/bbs/view.do?sCode=eng&mId=4&mPid=2&pageIndex=&bbsSeqNo=42&nttSeqNo=746.