Sanctions relief are at the core of the P5+1 (United States, United Kingdom, Russia, China, France, and Germany) and Iran nuclear negotiations, and although negotiators are somewhat tight-lipped about the details of lifting sanctions, expectations for Iran’s return to economic normalcy are running high. Although reports indicate that there has been some movement over the “snapback” provisions—that is, the protocols to reinstate multilateral sanctions should Iran fail to uphold its commitments—Iran’s aim to regain economic normalcy will take more than lifting US, EU, and UN sanctions. Many unilateral and non-nuclear sanctions will remain in place despite successful negotiations; and until Iran institutes major legal and structural reforms within its financial sector—to fall in line with international standards—banks and other global financial institutions will continue taking a cautious approach to reengagement. Consequently, non-nuclear sanctions and banks’ continuing fear of criminal and civil penalties could keep Iran largely frozen out of international financial markets even after a nuclear deal.

Iran has steadfastly maintained that without sanctions relief, there will be no deal. And for good cause— reaching a nuclear deal that provides complete sanctions relief will be a game-changer for Iran—a necessary step to begin recovering from years of economic mismanagement and to begin normalizing global ties. At the 2014 World Economic Forum in Davos, Iran’s President, Hassan Rouhani, gave a broad-stroke agenda for addressing Iran’s economic woes, which are largely a result of years of economic mismanagement, as well as sweeping unilateral and multilateral economic sanctions. Mr. Rouhani’s strategy includes reopening trade with its neighbors, furthering privatization, increasing lending to its private-sector, and ramping up revenues from non-oil exports.

In light of a possible deal, Iran has already started adjusting its monetary policy to absorb the effects of lifting sanctions. Curbing high inflation is a number one priority of the Central Bank of Iran, and in an important step, Iran’s Central Bank will unify the official and “black market” exchange rates once negotiators reach an agreement. This structural adjustment, although it will likely contribute to accelerated domestic inflation, will be good for Iran’s business environment—reducing corruption and rent-seeking that occurs with separate exchange rates. Externally, Iran has been laying the ground work for increasing its regional and global economic and political ties. Earlier this year, China accepted Iran as a founding member of the new, China-led Asian Infrastructure Investment Bank. As a competitor to Western-dominated lenders like the World Bank, membership in the Asian Infrastructure Investment Bank strengthens Iran’s economic and diplomatic footing with Asia. The Shanghai Cooperation Organization, which is a regional group with a long-term objective to improve economic stability and free-trade in Asia, has also promised to upgrade Iran’s status should negotiations prove successful.

Challenges remain. Nevertheless, deficiencies in Iran’s financial rules and regulations could make normalizing economic ties difficult. In a statement this past February, the Financial Action Task Force (FATF)—an inter-governmental body responsible for setting standards and promoting policies to protect the integrity of the international financial system— reaffirmed its call on member states to, “…advise their financial institutions to give special attention to business relationships and transactions with Iran, including Iranian companies and financial institutions.” According to FATF, Iran has failed to make meaningful progress towards addressing its anti-money laundering and terrorism financing deficiencies. The lack of criminal laws addressing terrorist financing and requirements for its financial institutions to file suspicious transactions reports is particularly troubling considering Iran’s top regional and global trading partners all have similar laws and regulations.

Since 2009, as a result of the deficiencies in Iran’s financial sector, FATF has called on its 36 member states to apply “effective counter-measures” and maintain vigilance when conducting transactions with Iran. Although FATF leaves it up to its members states to determine what the “counter-measures” will entail, the US has designated Iran’s entire banking sector—including the Central Bank of Iran— as a “jurisdiction of primary money laundering concern,” using authorities under Section 311 of the USA PATRIOT Act. Regardless, then, of whether or not the P5+1 and Iran reach an agreement, this designation against Iran will stay in place, and other FATF members are obligated to maintain similar measures.

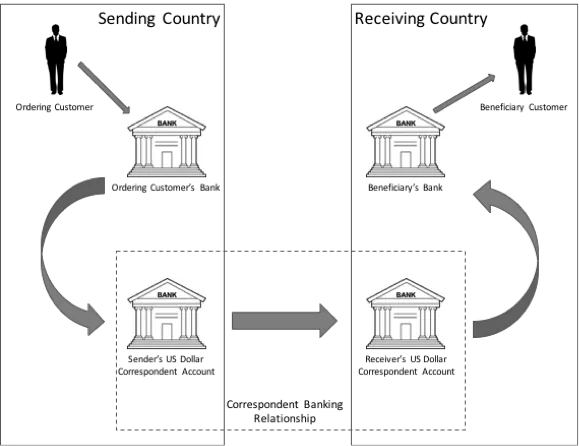

The other nuclear option. Dubbed by Washington insiders as Treasury’s “nuclear option,” a Section 311 designation effectively prevents targeted entities from using the US financial system and transacting in US dollars. More specifically, the finding prohibits US banks and financial institutes from opening or maintaining correspondent accounts with Iranian institutions, and also requires US banks to take special measures to ensure Iran does not indirectly use the US correspondent banking system. Only used eleven times, the Economist points out that, “a 311 designation is more often than not a death sentence.”

International trade and finance depends heavily on correspondent banking, and the US financial system plays a central role. Domestic banks, for example, may have limited access to foreign financial markets, but require a means to service their customers. This is where correspondent banking comes in. These accounts essentially act as the domestic bank’s agent abroad. For reference, Figure 1, illustrates the basic premise of a correspondent banking transaction.