Research, ideas, and leadership for a more secure, peaceful world

Reports & Papers

from

Middle East Initiative, Belfer Center

A Theory of Everything for the Middle East Political Economy

MEI Senior Fellow Ziad Daoud provides a comprehensive analysis of rentierism in the Middle East, documenting how rent-based economies are common across resource-rich and resource-poor states, and explores the implications this unifying theory has on the region's political futures and transitions.

The Nihran Bin Omar oil field flare stacks burn north of Basra, Iraq, Wednesday, March 22, 2023. In the wake of the US invasion of Iraq in 2003 and toppling of Saddam Hussein, foreign investors flocked to the country's abundant oil fields and contracts were doled out, filling Iraqi state coffers. The new constitution drafted in 2005 states that the country's oil wealth belongs to the Iraqi people. (AP Photo/Nabil al-Jurani)

Introduction

There’s a theme that unifies the seemingly disparate economies of the Gulf Cooperation Council, Iraq, Egypt, and Jordan, and likely other countries in the Middle East and North Africa. All of them rely on rents — income earned with relatively little work. Such windfalls shape not only economic relationships but also political systems.

Rents take five forms in the region. Oil and gas exports are the most obvious, but they’re far from the only example. Others include income from sovereign wealth funds, revenue from trade routes like the Suez Canal, foreign aid, and land sales.

The story of the Middle East and North Africa is often told as a tale of two regions. On the one hand, there are resource-rich states, mainly in the Gulf, flush with petrodollars and sovereign wealth funds. On the other are resource-poor nations like Egypt and Jordan, struggling to meet the needs of their large populations. Rents provide a unifying theme — a theory of everything — for these divergent tales.

The unifying theory of rents isn’t just a theoretical beauty; it also has two predictive implications.

First, many countries in the region dream of a future beyond rentierism — a future in which productivity and innovation drive growth. But these ambitions often ignore the political realities. Rentierism creates a web of patronage and privilege that resists change. Attempts to move toward a productive economy through technical policies alone, without addressing the underlying political structures, are unlikely to succeed.

Second, the doom-and-gloom predictions of the region's demise if the world moves away from fossil fuels are likely overstated. The Middle East has proven itself an innovator when it comes to generating new sources of rent, both historically and in the present. A transition to a productive economy remains a distant dream, but the region's capacity for survival, even in its current form, shouldn’t be underestimated.

From the Cradle to the Mediterranean: Rents Are Everywhere

So, what are rents, anyway? They’re an income that satisfies three conditions: First, the source is external. Second, it doesn’t require much work to generate. Third, the government is the main recipient of the income. A key figure in understanding rentier economies is Hazem Beblawi, an economist who later served as Egypt's prime minister.1

The classic example from Beblawi’s paper, “The Rentier State in the Arab World,” was rents from oil and gas, especially in the Gulf. In a more recent paper, the Emirati academic Abdulkhaleq Abdulla argued that these economies are now “post-oil and post-rentier.”2 My assertion here is that not only is the rentier model alive and well in the Gulf, but it's also a powerful force shaping the broader Middle East, and it goes well beyond fossil fuel.

Let’s start with Iraq — a textbook rentier state that’s almost entirely dependent on oil. Crude oil accounts for 97% of its exports,3 and it is the government’s main source of revenue, contributing 90% of state income.4 Oil extraction employs only a small proportion of the Iraqi workforce.

The distribution of oil is a different story. The government in Iraq employs about 40% of the workforce in the public sector and pays them twice as much as the private sector.5 This isn’t in return for productive work; instead, it serves as a blunt and inefficient way to distribute oil income, one that distorts the larger economy.6

Is the Gulf Post-Oil, Post-Rents?

In a recent paper on the “Gulf Moment,” Abdulla makes the bold claim that the Gulf Cooperation Council nations have moved beyond rentierism. His arguments? (1) Oil is no longer as pivotal to their economies as it once was. (2) The Gulf nations have introduced taxes, which are directly antithetical to the rentier-state model. (3) They are home to four of the world’s largest sovereign wealth funds.

Let’s unpack these arguments one by one.

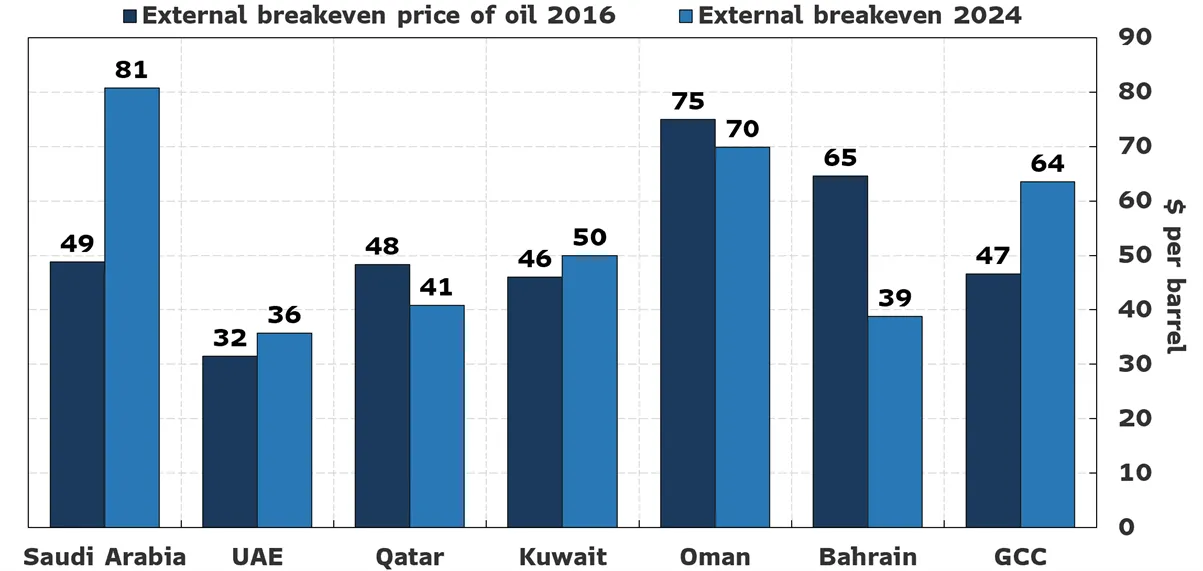

First, Abdulla argues that “the Gulf Moment is not oil driven” and that “the new [Arab Gulf States] are mainly post-oil.”7 Alas, data tell a different story.

One measure of oil dependence is the crude oil price needed to fund a country’s imports and offset outward remittances. Estimates by the International Monetary Fund (IMF) show this “external break-even price of oil” has risen in Saudi Arabia, the UAE, and Kuwait since 2016 — indicating more, not less, reliance on oil. True, the estimates are lower for Qatar, Oman, and Bahrain, but when weighted by the size of each economy, the Gulf’s aggregate external break-even oil price has risen from $47 per barrel in 2016 to $64 in 2024.

Another way to gauge oil dependence is to look at the oil price needed to balance government budgets. Here, IMF estimates paint a similar picture. Saudi Arabia, Kuwait, and Bahrain are increasingly reliant on oil to fund their budgets, while the UAE, Oman, and Qatar are less so. In aggregate, Gulf governments need a higher oil price to balance their books today than in 2016.

It’s hard to claim that the Gulf was post-oil in 2016. Just one year earlier, Saudi Arabia was on the brink of going “completely broke” in two years,8 forcing it to launch Vision 2030, with the principal aim of diversifying the economy from oil. The slump in energy prices that year caused an economic downturn across the Gulf — hardly a sign of post-oil dynamics. This episode shows not only that the Gulf wasn’t post-oil in 2016, but that its dependence on oil has deepened since then.

Second, Abdulla argues that the Gulf countries are “daring to introduce...taxes,” which are “antithetical to the rentier-state model.” It’s true that some Gulf countries have introduced a value-added tax. It’s also true that the UAE unveiled a 9% corporate tax,9 effective June 2023, and that Oman discussed introducing income taxes.

But magnitudes matter. And taxes in the Gulf are modest, generating less than 5% of gross domestic product (GDP), according to IMF calculations. By comparison, taxes typically account for about 25% of GDP in advanced economies and over 15% in emerging markets. The Gulf’s tax burden remains relatively light.10

Taxes also remain highly sensitive politically. Kuwait and Qatar have yet to introduce a value-added tax, even though it was a region-wide initiative. Oman intended to introduce income tax in 2022 or 2023,11 but its implementation has stalled. The recent rise in oil prices has eased pressure to impose unpopular tax measures.

The Gulf Has Become More Dependent on Oil Since 2016

International Monetary Fund

Source: International Monetary Fund. Note: The external breakeven is the price of oil needed to balance the current account – a higher price indicates stronger oil dependence.

The Gulf leadership didn’t spin the introduction of taxes as “dismantling the old welfare state,” as Abdulla argues. Instead, they carefully positioned it as a way to recycle wealth from foreigners back to citizens. As the Saudi Crown Prince Mohammed bin Salman put it, the taxes aim to ensure that “the cash that the foreigner benefits from ... will go back to their government and the government will spend it in education, health, infrastructure, or even salaries [for citizens].”12

This isn't just a Saudi phenomenon. Caught between the pressures of the social contract and budgetary needs, Kuwait is planning to raise fuel prices — but only for expatriates, not citizens.13 It's a strategy that could be replicated for income taxes, if and when the Gulf countries decide to implement them.

Third, how about the Gulf’s sovereign wealth funds? Aren't they a sign that the region has moved beyond rentierism? Not quite.

It’s true that the Gulf is home to four of the world’s 10 largest sovereign wealth funds, a testament to its financial clout. It’s also true that it’s the only region in the world with three funds managing nearly $1 trillion each in assets.

But sovereign wealth funds aren't a sign of a post-rentier future. Instead, they're a tool to maintain the model for future generations. Crown Prince Mohammed bin Salman clearly explained his vision in a 2016 interview. The aim was to make “investments the source of Saudi government revenue.” How? By teaming up with private equity firms to invest holdings overseas and produce a steady stream of dividends unmoored from fossil fuels.14

Notice how the prince's vision aligns with the three key characteristics of rentierism: external income, minimal domestic labor, and government control. Even in its expanded form, the sovereign wealth fund employs only a small fraction of the Saudi workforce, while generating income for the government through overseas investments. It's a classic rentier strategy, but with a modern twist.

So, there we have it. The rentier model is alive and well among hydrocarbon producers in Iraq and the Gulf states. The latest iteration of this model involves leveraging sovereign wealth funds to generate income from overseas investments, ensuring a steady flow of wealth even as oil revenues fluctuate. The states may genuinely want to diversify away from oil, but the appeal of rentierism endures, even in the 21st century.

Why Isn’t Jordan in Crisis? Foreign Aid as Rents

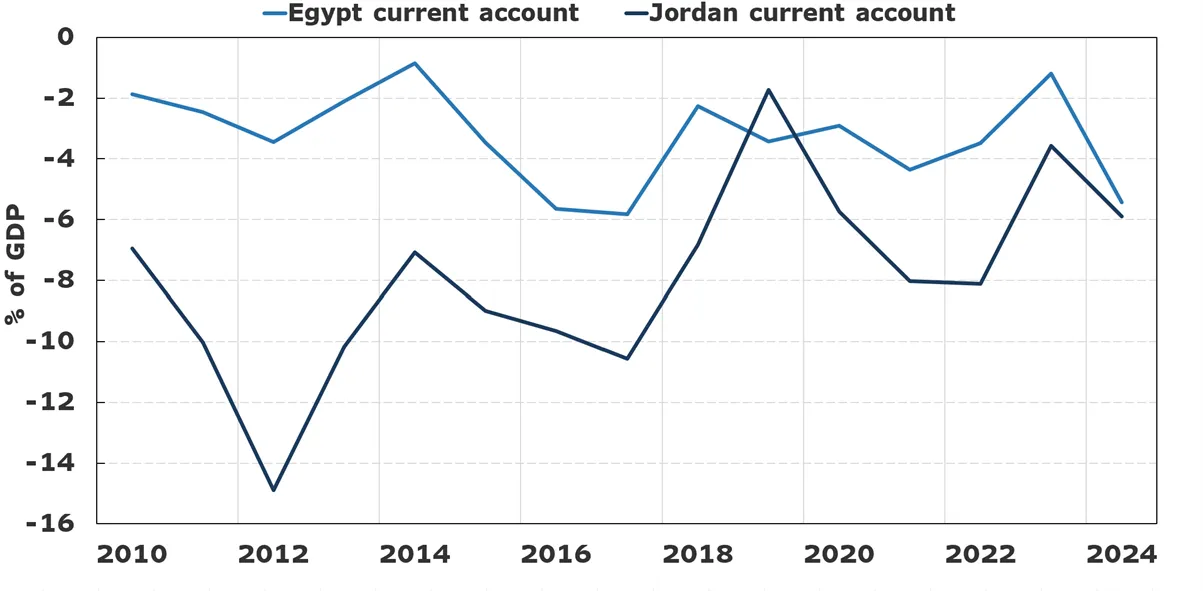

Jordan hasn’t faced a recent currency crisis like Egypt or Lebanon, but maybe it should have.

Compare Jordan to Egypt, for example. Both countries struggle with a persistent trade deficit — where imports outstrip exports and remittances — but Jordan’s shortfall has been consistently larger. Yet, Egypt has faced two currency crises in recent years, while Jordan has remained relatively stable. Something doesn't add up. How can a country with a worse trade deficit avoid the economic turmoil that has plagued its neighbor?

Now, let's broaden our comparison to include Lebanon. Both Lebanon and Egypt have experienced crises recently, forcing them to sharply devalue their currencies. While the specific causes of their problems vary, there are four common factors that contributed to their downfall: high government debt, large trade deficits, reliance on commodity imports, and currencies fixed to the dollar.

Jordan’s Trade Balance Is Worse Than Egypt’s

Jordan ticks all four boxes above. Its debt and trade deficits are higher than Egypt’s, although not as severe as Lebanon’s. It imports food and energy. And it has a fixed exchange rate against the dollar.

So, why has Jordan avoided the fate of its neighbors? The answer lies in foreign aid. This support, which meets all the hallmarks of rentier income — external, government-controlled, and requiring minimal effort — has been a lifeline for the Jordanian economy.

Where does this foreign aid come from? There are three key sources.

First, the IMF. Jordan has received IMF loans almost continuously since 1989.15 But the fund alone can’t explain Jordan’s relative stability compared with Egypt. After all, Cairo has also received consistent assistance from the IMF and is currently the world’s second-largest borrower from the fund.

Second, the Gulf. According to data from Hasan Alhasan and Camille Lons at the International Institute for Strategic Studies,16 Jordan received about $9 billion in aid from the Gulf states between 2011 and 2022. This figure is smaller than the $48 billion Egypt received, but it's significant relative to Jordan's smaller economy. The $9 billion represents about 19% of Jordan's 2023 GDP, while the $48 billion Egypt received was just 12% of its GDP in 2023. Yet even with this difference, Jordan's relative stability remains puzzling.

The third major source of foreign aid for Jordan is the United States. Under a memorandum of understanding, the United States has pledged $1.45 billion a year in budgetary and military support to Jordan from 2023 through 2029. This represents a significant portion of Jordan's GDP — roughly 3% annually for seven years.

The United States often supplements its official aid pledges with additional support. For example, in December 2023, it provided an additional $200 million to Jordan on top of the annual aid package.

At a time when the geopolitical risks in the Middle East are rising and rating agencies are downgrading the credit score of countries such as Israel,17 Jordan has bucked the trend, receiving a credit upgrade from S&P Global Ratings in September 2024. The reason? “Despite an increase in geopolitical tensions, we think external support from donor [i.e., U.S. and Gulf] multilateral [i.e., IMF and World Bank] partners would be highly forthcoming in most scenarios,”18 S&P Global wrote.

The geopolitical price Jordan pays in exchange for this support is beyond the scope of this paper. The focus here is on the economic reality: Jordan needs foreign aid, and foreign aid is a form of rents.

So far, we’ve covered Iraq, the Gulf states, and Jordan. We've seen how oil and gas, sovereign wealth funds, and foreign aid manifest as different forms of rent. Now, let's turn our attention to another country and another manifestation of rentierism.

Egypt’s Unlucky Journey Through Rentierism

“Since the mid-1970s, Egypt has been a case of an authoritarian political system that relies for its stability on a semi-rentier state,” wrote the late Egyptian political economist Samer Soliman in 2006.19 Egypt’s journey through different forms of rents has been one of experimentation and a lack of good fortunes.

For a period, Egypt benefited from oil rents. Between the 1970s and early 2000s, the country was a net oil exporter. While the amount it produced never exceeded 1 million barrels a day — about a tenth of Saudi Arabia’s output — oil provided a valuable source of income for the state. That ended around 2010, when consumption outpaced production, bringing Egypt’s oil rents to an end.

Egypt's experience with natural gas mirrors its oil story. In the early 2000s, increased gas production led to a brief period of export-driven rents. But rising domestic demand and declining production soon reversed this trend, making Egypt a gas importer once again. In the late 2010s, the discovery of the Zohr gas field offered hope, but it proved to be a temporary reprieve. Today, Egypt is again importing gas and competing with Europe for liquefied natural gas,20 highlighting the volatility of its energy resources.21

Historically, the Suez Canal has provided Egypt with a steady stream of rentier income. Nationalized in 1956, the canal generates revenue for the government from external sources with limited labor. But, again, luck was not on Egypt’s side. Since 2023, wars in the Middle East have led to a 70% decline in canal traffic, resulting in a $6 billion loss in the first eight months of 2024, according to President Abdel Fattah El-Sisi of Egypt.22

The disruption to the Suez Canal was a major setback, but Egypt quickly found a new source of rentier income: land sales. In February 2024, the government inked a $35 billion deal with a group of investors led by an Abu Dhabi sovereign wealth fund to sell a large tract of land on the North Coast, known as Ras El Hekma.23

This land sale checks all the boxes for rentier income: the funds originated from an external source, the transaction required minimal effort beyond a few officials signing documents, and the proceeds flowed directly to the government. It's straightforward rentierism.

Some might argue that this deal differs from other types of rent. Oil, gas, foreign aid, and trade routes provide a continuous stream of income. In contrast, land sales are one-time events that rarely recur. There are two responses to this objection.

The first is that the Ras El Hekma deal might not be a one-off. There are reports of potential land sales in other areas, such as Ras Gamila on the Red Sea, to Saudi Arabia.24 There was also the controversial transfer of the Tiran and Sanafir islands to Saudi Arabia in 2016. While not a direct sale, the transfer occurred amid significant financial support from the Kingdom and despite a court ruling in Egypt.25 These examples suggest that land deals could become a recurring source of rentier income for Egypt.

The second response is Bahrain.

An Island Too Straight to Be True

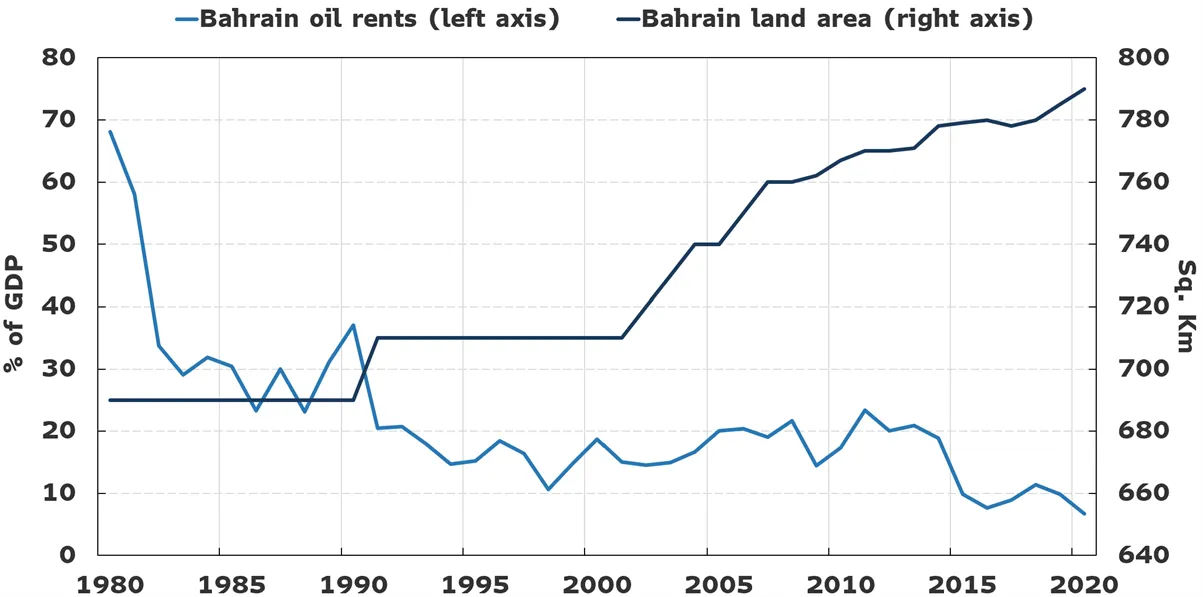

Bahrain, a small oil-producing monarchy, has found a new source of rent: land reclamation. As the importance of oil revenues has waned, the government has turned to expanding its territory and its income by reclaiming land from the sea.

Since 1991, Bahrain has expanded its area by an impressive 14% through land reclamation. This artificial expansion is visible from the air — the island's straight lines and geometric shapes betray their unnatural origins.

The decline of oil rents in Bahrain, from around 30% of GDP in the early 1990s to less than 10% in the early 2020s, coincided with a period of intense land reclamation. As oil revenues dwindled, the government sought to compensate by expanding its territory and generating new revenue opportunities through reclaimed land.

Bahrain Rents: From Oil to Land

Land expansion meets all the criteria of rentierism. The government benefits financially from selling reclaimed land to foreign developers, and the process is relatively easy and requires minimal labor input.

So, Egypt's land sale wasn't an isolated incident. Similar deals have occurred in the past, more may follow, and Bahrain's experience with land reclamation demonstrates that such transactions can provide a continuous source of revenue rather than a one-time windfall.

Problems With Rents

Rents are undeniably appealing. Who doesn’t want to earn significant income with little effort? After all, isn’t that what we work toward as individuals — the ability to live off rents in retirement?

But countries are different from individuals, and rentier economies tend to face at least three problems.

1. Rentier income is notoriously volatile. Oil and gas exporters are all too familiar with the boom-and-bust cycles of the energy market. Sovereign wealth funds are also susceptible to financial market fluctuations. Even seemingly stable sources of rent, like trade routes, can be disrupted by geopolitical events — the recent plunge in Suez Canal revenue being one example. When a country depends heavily on a single source of rent, it becomes vulnerable to its inherent volatility.

2. Rentier economies often suffer from low productivity. Why? Governments in these economies tend to distribute rentier income to citizens, often in the form of low-productivity, high-wage public sector jobs. This strategy is designed to buy political loyalty and maintain social stability.

Empirical evidence supports this claim. A report by the International Labour Organization finds that “labour productivity has declined since the 1980s in Arab economies in general, and in the Gulf Cooperation Council (GCC) economies in particular.” The report also “found a more accelerated decline in productivity over the past two decades. When compared to other regions, the Arab States region is now the worst performing globally in terms of productivity growth.”26

And lagging productivity is problematic. The only way to sustainably raise economic growth over years and decades is by working more productively. Rents undermine this essential ingredient of long-term success.

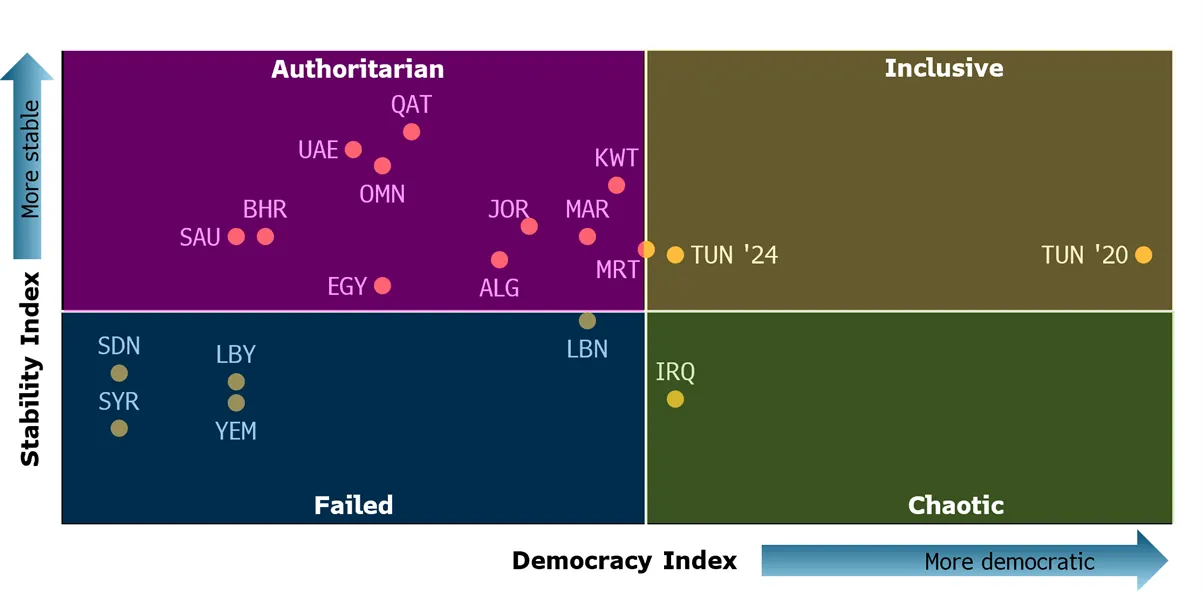

Middle East Political Institutions Are Mostly Authoritarian

3. Rentier economies often breed authoritarianism. When a government doesn’t need to tax its citizens, it also tends to provide less political representation. A scan of the political institutions in the Middle East shows a pervasive lack of pluralism. Even Tunisia, a brief beacon of expanded political representation after the Arab Spring of 2011, has now firmly reverted to authoritarianism.27

Not Just a Pretty Theory

Rentierism isn’t just an academic curiosity. It provides a unified framework for understanding the political economy of the Middle East. It also makes two predictions about the region’s future.

The Middle East is awash with initiatives to transform economies. Examples include Saudi Vision 2030, Qatar National Vision 2030, Egypt Vision 2030, UAE Vision 2031, Kuwait Vision 2035, Oman Vision 2040, Jordan’s Economic Modernisation Vision, and Iraq’s 2020 White Paper. The common theme? Make economies more modern, vibrant, diversified, and productive.

Given our understanding of rentierism, what are the chances of success for these reform initiatives?

Rents aren’t just a source of income; they also shape political and social structures. They often lead to authoritarian political systems and create social contracts that trade economic benefits for political acquiescence. But these initiatives tend to focus on technical economic solutions, such as encouraging private sector growth, reducing deficits, cutting subsidies, and introducing taxes. They often neglect the underlying political dynamics.

Technocratic approaches that shy away from politics are unlikely to succeed. Any successful attempt to transition from a rentier to a productive economy will likely involve political changes, including greater openness and broader participation. Ignoring this political dimension is a recipe for failure.

There’s also a second prediction: don't write off the region's ability to continue generating rents. The narrative of impending political or economic doom for the region’s energy producers once the age of fossil fuels wanes is likely oversimplified. This paper challenges that notion, highlighting the region's ability to innovate and find new sources of rent. From traditional forms like oil and gas to newer mechanisms like sovereign wealth funds, foreign aid, trade routes, and even land sales, the Middle East has demonstrated a surprising capacity for adaptation.

This innovation has prolonged the life of governments in the region and delayed the democratic openings. Authorities would rather use their ingenuity to find new sources of rents than disrupt the social contract or share power more widely. After all, it's easier to give up money than power.

Innovation can mitigate some problems associated with rents. For example, adding sovereign wealth fund returns to oil revenues reduces the volatility of rents. But it doesn’t eliminate the low-productivity issue or the likelihood of authoritarianism. In fact, these innovations often serve as tools to maintain authoritarian rule more than to promote economic development.

It’s in this context that the development of new trade routes has gained attention in the region. Initiatives like the India-Middle East-Europe Economic Corridor and the Iraq Development Road aim to position the Middle East as a key transit hub between Asia and Europe. While these projects may have economic benefits, they’re also appealing as potential new sources of rent. As I’ve heard one regional politician put it, the India-Middle East-Europe Economic Corridor could be as transformative for Jordan as the Suez Canal has been for Egypt.

In 2006, Samer Soliman wrote that the Egyptian government tended to “look up to the sky, hoping it would rain gold.” This rentier mindset persists to this day and applies beyond Egypt to the wider Middle East.

Statements and views expressed above are solely those of the author(s) and do not imply endorsement by Harvard University, Harvard Kennedy School, the Belfer Center for Science and International Affairs, or the Middle East Initiative.

Recommended citation

Daoud, Ziad. “A Theory of Everything for the Middle East Political Economy.” Middle East Initiative, Belfer Center, May 2026

A Theory of Everything for the Middle East Political Economy

Samer Soliman, al-nizam al-qawi wal-dawla al da’ifa, Idarat al azma al maliya fi misr[The Strong Regime and The Weak State: The Management of the Fiscal Crisis in Egypt] (Cairo: General Organisation for Cultural Palaces: 2006).