Reports & Papers

Executive Summary

The European NewSpace sector is moving at rocket speed: Isar Aerospace’s and ICEYE’s recent nine-digit fundraises and Isar’s first rocket launch in March 2025 are the press releases behind extraordinary operational progress; a new generation of European space companies is proving what is possible for Europe’s future. SpaceX’s roughly $1.8 trillion IPO valuation should nonetheless (or perhaps precisely because of this progress) serve as a wake-up call. When capital markets value the largest U.S. NewSpace company at several hundred times its European counterparts,1 long-term competitiveness will be difficult to sustain without a proactive industrial policy at the Union level. The precedent is Airbus, a joint European effort that began from a comparable position relative to its American rivals and is now the market leader in large commercial aircraft manufacturing.

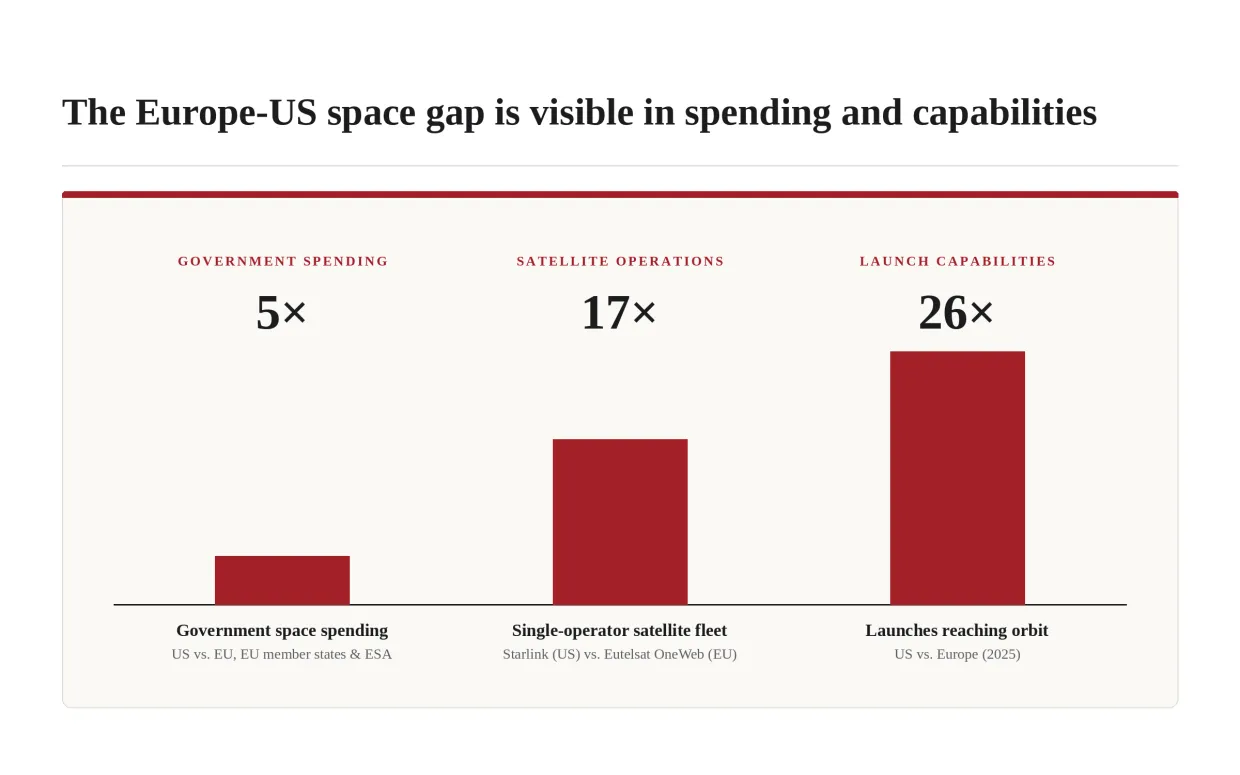

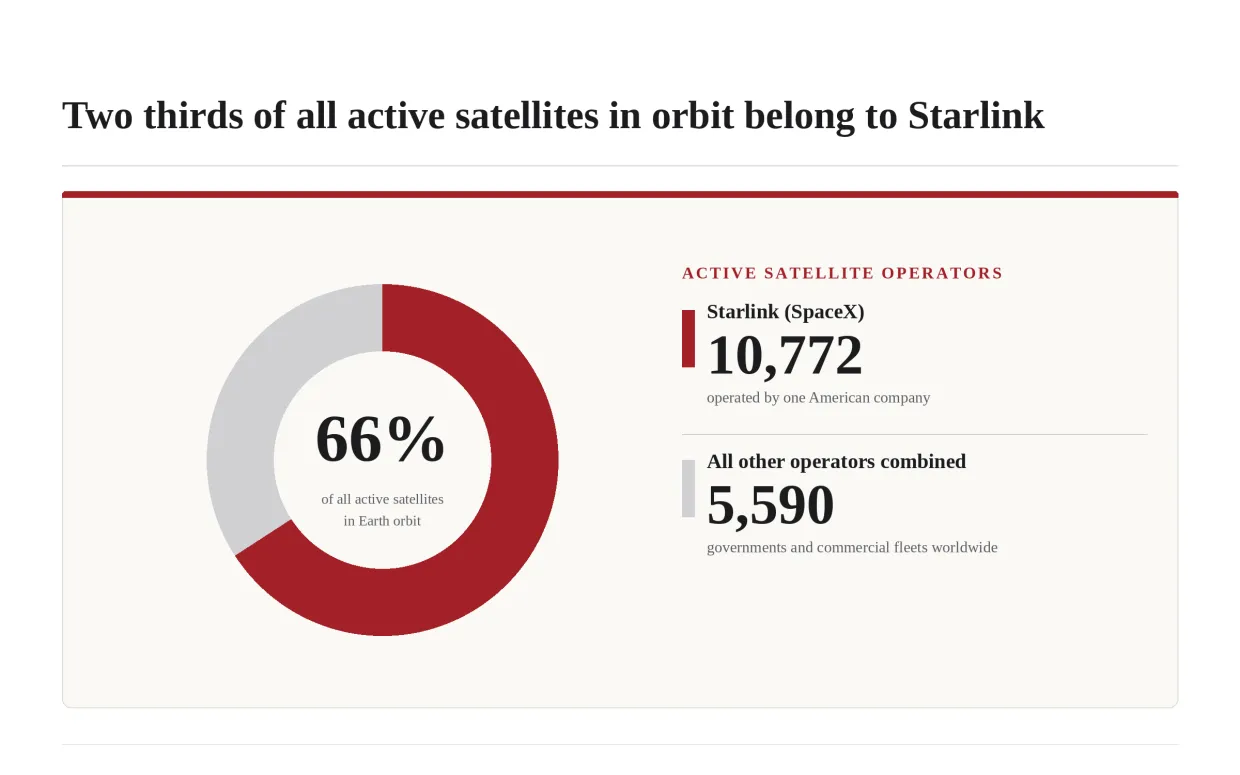

The structural gaps in the European Union (EU)2 are substantial: the United States (U.S.) outspends the EU and its Member States by about 5 to 1, out-launched Europe 179 to 7 in 2025, and a single American operator, Starlink, now runs two-thirds of all active satellites (17 times the largest European fleet). While EU and Member States’ space budgets sit at record highs, every additional euro spent in the last three years is met by a larger American multiple.

The effects will be felt in the civilian and the military domain since both share the same technological base: Earth observation satellites that allow for wildfire identification, crop yield forecasting, and methane leak detection are from the same class as those used for military reconnaissance.

Europe so far has failed to establish institutional structures for frontier research, interoperability, procurement and late-stage financing. These are, however, necessary for NewSpace companies to achieve operational maturity. Simultaneously, Europe’s dependencies on non-European launch and satellite services remain – a vulnerability the loss of Soyuz and the delayed operability of the European Ariane 6 launch system exposed in recent years.

This brief offers five recommendations that will enable President von der Leyen and Commissioner Kubilius, in partnership with Member States, to transform current public and private investments to accelerate frontier innovation and civilian autonomy by 2030. This would reduce Europe’s dependency on partners while preserving the international alliances that remain to serve European interests.

Key Assessments:

- Europe lacks the institutional capabilities to foster innovative frontier space research. Europe’s space institutions are fragmented and risk-averse. ESA operates half of Europe’s space budget, with cost-plus and geographic return rules, protecting national incumbents. The other half is administered by several national agencies and ministries running largely uncoordinated programs. Germany’s SPRIN-D is the only agency in an EU Member State running the DARPA logic (placing public bets on groundbreaking technologies) in practice but is not designed to invest in defense/space technology. The Commission should support the founding of “Space-RIN-EU”, a proposed intergovernmental frontier-research consortium modeled on Airbus with a €1-billion annual budget (recommendation 1).

- While both European private and public space investments are rising, 2025 data shows the gap relative to the U.S. continues to grow in the private late-stage segment. Even newly established European instruments cannot close this gap, as they remain too small and fragmented to lead €500-million+ NewSpace financing rounds. Additionally, European anchor demand procurement does not prioritize efficient delivery. Hence, the Commission should establish a €10-billion EU Late-Stage Space Investment Fund, modeled on the NATO Innovation Fund, paired with an innovation-friendly procurement framework based on milestone-based, fixed-price contracts as well as multi-year demand commitments (recommendation 2).

- Sustained and significant European public space investments depend on cross-country public support, which is currently politically fragile and failure-sensitive. European programs are framed and reported primarily as defense spending, even though most of the projected $1.8 trillion space economy by 2035 sits in downstream civilian services (e.g., flood monitoring, communications). This weakens their reputation in neutral Member States and military-skeptic, failure-averse populations. The Commission should improve visibility of civilian use cases and institutionalize a European failure culture that is crucial for failure-prone NewSpace launchers (recommendation 3).

- Europe’s dependency on non-European space services has become very clear recently but still has not been properly mapped or regularly tested. Europe still has no numerical account of how many Member State military channels route through commercial U.S. constellations, or what replacing each dependency would cost. The Commission should publish annual robustness tests of these dependencies (recommendation 4).

- The largest single source of inefficiency in European space procurement is fragmentation. Each national constellation comes with its own interfaces and its own encryption, which multiplies costs and slows any joint response in a crisis. The Commission should set binding cross-border technical interoperability standards for satellite platforms, ground segments, refueling, and secure data interfaces (recommendation 5).

I. Why Europe Is Behind in Space and Why the Window Is Closing

The Problem: Despite the Strategic Importance, Europe Is Behind

Space always was (and still is) a military domain, as the head of the Bundeswehr Space Command, Brigadier General Michael Traut, has put it.3 The change in recent years, however, is the profitable commercialization and industrialization of orbit, and its integration into civilian critical infrastructure at a scale that did not exist a decade ago.

The general importance of space for Europe can be exemplified along three pillars

(figure 1)4, 5, 6, 7, 8, 9, 10, 11:

Defense capabilities: Space has become an increasingly important warfighting domain. Positioning, communications, early warning, and reconnaissance satellites underpin modern military operations. States without access to these capabilities cannot credibly defend themselves.

Economic opportunity: Space is one of the fastest-growing industrial sectors in the world economy, which applies to the building, launch, and operation of satellites but also to the direct applications it enables and the greater industry benefits that are linked to progress in space technology. It furthermore builds on the advanced manufacturing and precision-engineering strengths existing in Europe already today.

Sovereign autonomy: As space technology has become crucial for defense but also for civilian economic activity, everyday life could not continue if access to these capabilities is cut off. Without its own launch, satellite, and constellation capabilities, Europe depends on non-European actors, both state actors and private companies.

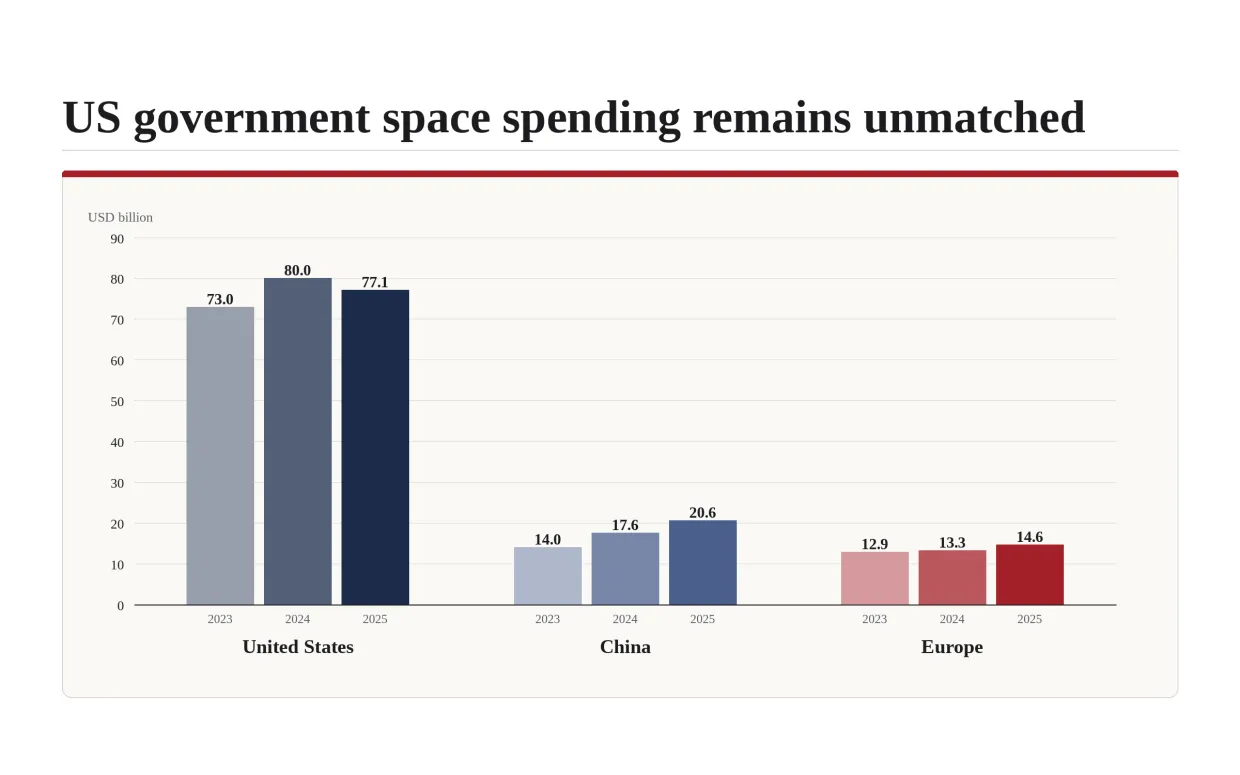

Yet, Europe is far behind in the space race, which becomes visible with government funding for space-related activities. The U.S., with a GDP 1.5 times larger than the EU’s, outspends the EU institutions and EU Member States12 combined space spending by roughly 5 to 1 (figure 2)13, 14, 15.

Europe has begun to take this seriously. At the 2025 ESA Ministerial Council, Member States committed a record €22.1 billion for 2026-2028, up roughly 30% from the previous three-year period.16

France’s 2025-2040 National Space Strategy treats space as a military domain and pillar of national sovereignty, and commits to strengthening military capabilities in intelligence, early warning, communications, positioning, space surveillance, and active defense.17 Germany’s first National Space Security Strategy, released in 2025, commits up to €35 billion until 2030 and also recognizes the significant role of private sector innovation for space and the utilization of space technology.18 Beyond Europe’s economic powerhouses France and Germany, however, Member State activity remains limited. Italy’s €1.07 billion IRIDE Earth-observation constellation, funded through the post-COVID national recovery and resilience plan and coordinated with the European Space Agency (ESA) and the Italian Space Agency (ASI), is the most important exception.

Orbit Is a Contested Space with 54,000 Satellites Projected by 2030

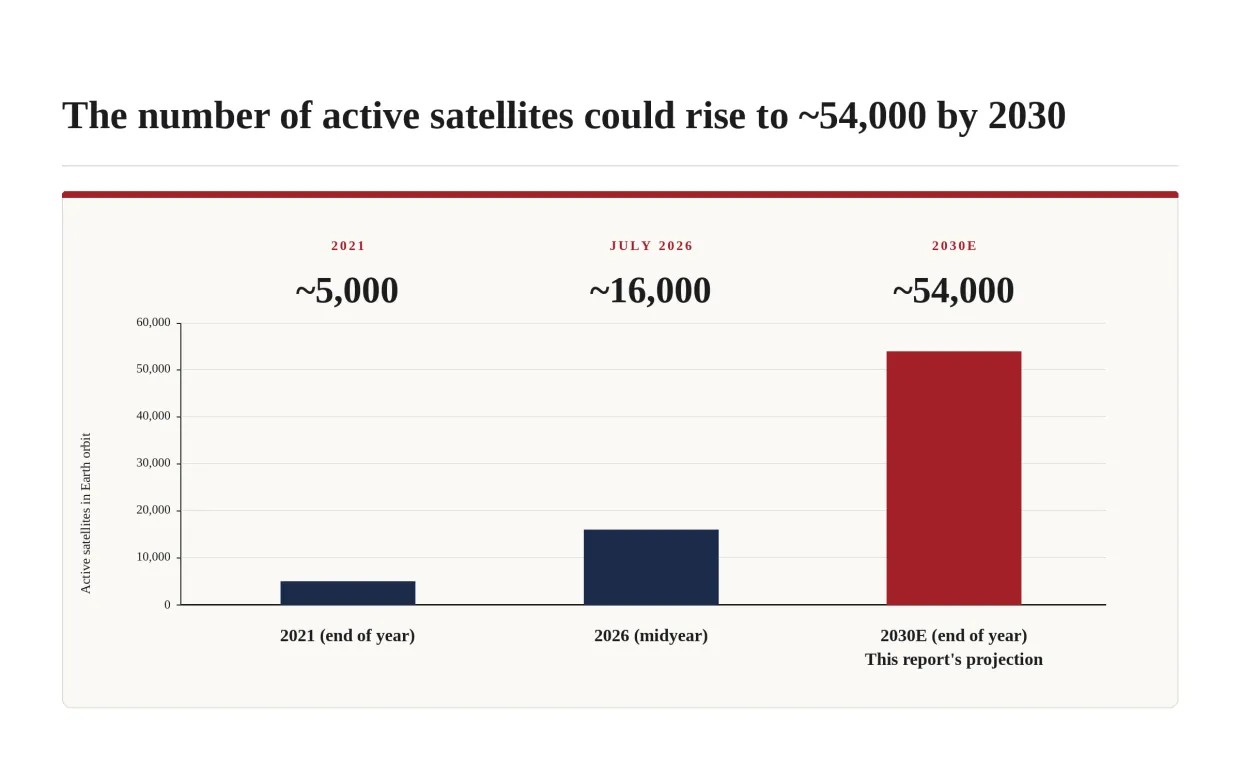

Orbit today can be compared to international waters with very few binding rules. Just as global freight shipping and thus the number of ships increased in the maritime space, the number of satellites is rising drastically: from about 5,000 by the end of 2021 to 16,000 by midyear 2026 toward 54,000 by 2030 according to our own projections (figure 3)19, 20. Even more than in the sea, the actual space in space is becoming contested as orbits and satellite radio frequencies are provided on a first-come, first-served basis and the risk of in-orbit collisions is exponentially rising. This leads to a first-mover advantage for those currently and soon-to-be in space. With satellite mega-constellations planned, especially in low earth orbit, some scholars call current developments the “de facto orbit occupation by single actors”.21 For Europe and other actors this might imply that if they are not using current momentum they could lose access to certain capabilities. Hence, as the window to claim orbits is closing, the time for Europe to act is now.

Europe Lacks Late-Stage Capital and NASA-Style Procurement

SpaceX proves what private space companies can deliver, both in terms of efficiency and in terms of speed. SpaceX’s success, however, is also a result of very benevolent institutional conditions in the U.S. SpaceX has raised over $10 billion in private late-stage capital before reaching commercial viability. The U.S. government has carried SpaceX across that late-stage “financing valley” through two specific procurement vehicles: NASA Commercial Resupply Services from 2008 and Commercial Crew from 2014. Instead of being cost-based, both programs were fixed-price, milestone-based, and provided funding for demonstrating capabilities. This created efficiency-focused incentives and drove innovation. Without that efficiency-focus, SpaceX would likely not have been able to secure further late-stage venture financing.

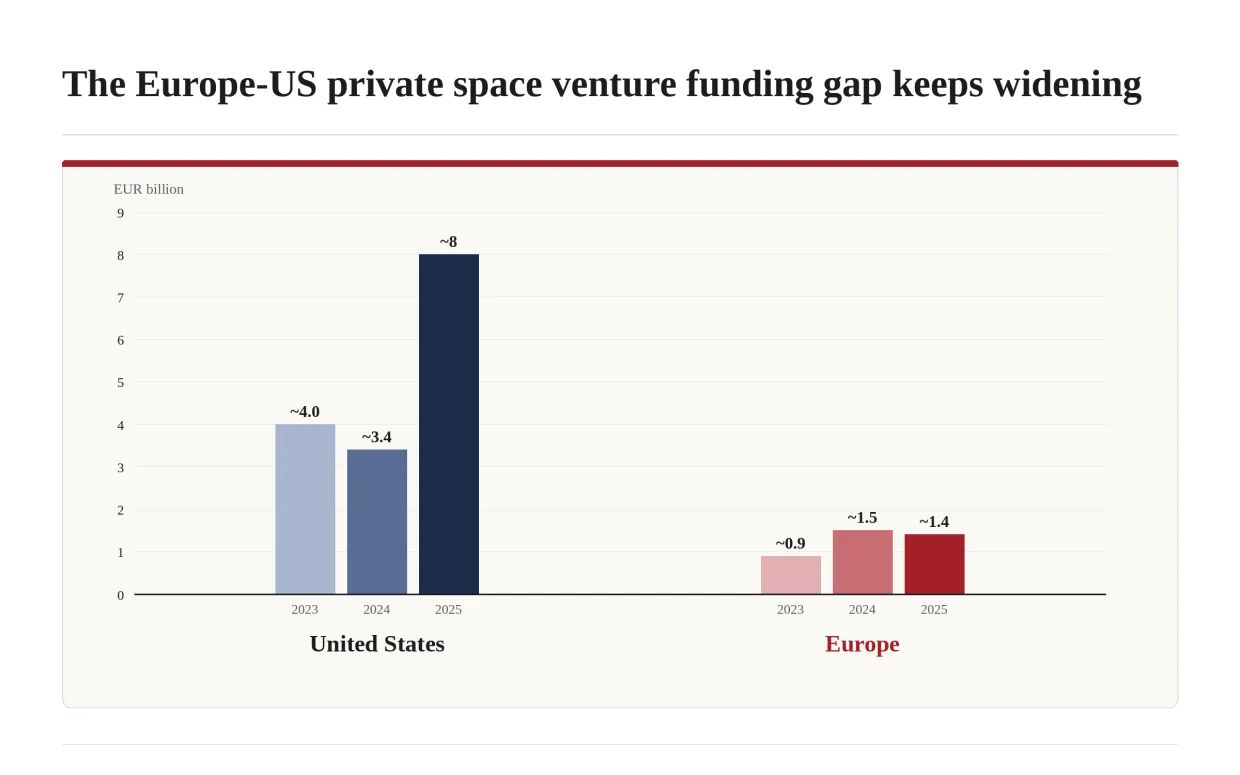

Europe lacks both sides of this equation. Despite a recent rise in European space venture funding, EU funding still runs at roughly one-sixth of U.S. levels in absolute terms (figure 4).22 Late-stage tickets of €200 million to €1 billion, which a launcher or large-constellation business requires to reach a minimum scale, are extremely difficult to assemble on the continent.

On the procurement side, ESA continues to operate primarily under cost-plus and geographic-return rules. ESA’s Boost! initiative23 and the European Launcher Challenge24 mark first steps toward milestone-based commercial procurement. However, both initiatives represent only a fraction of the multi-billion-dollar NASA procurement programs that carried SpaceX to commercial viability. Europe has several high-potential NewSpace companies, including Isar Aerospace, The Exploration Company, Rocket Factory Augsburg, MaiaSpace, Blackwave, PLD Space, and ICEYE. Under the current procurement regime, however, there is no institutional path to reliably carry those companies from Series B/C to operational maturity under European ownership, commercial viability, and IPO-readiness. Without that path, the most likely mid- to long-term outcomes are acquisition by U.S. or Asian buyers, relocation of headquarters, or commercial failure before product-market fit, as seen in the case of the failed German electric vertical take-off and landing (eVTOL) aircraft industry with companies like Volocopter and Lilium.

Taken together, the potential benefits of catching up in the space domain would be substantial. Europe could capture economic upside in the trillion-dollar bracket, with quality-of-life gains in disaster response, agriculture, climate monitoring, and connectivity. Additionally, improved sovereign independent space technology would create a defense capability that does not depend on single public and private U.S. individuals. For a real shift, however, a significant financial burden would need to be overcome. Closing the gap requires heavy and sustained investment in a field with very high entry barriers and failure risk.

The Urgency: The Europe-U.S. Capabilities Gap Is Widening

The urgency comes from the gap between Europe’s progress and what the U.S., and to a certain extent also China and Russia, are accomplishing on a different scale and tempo. Beyond the higher U.S. spending, the structural gap between the U.S. and Europe is even larger in actual capabilities such as satellite operations and rocket launches (figure 5).25, 26, 27 At the same time, a window is opening: Europe’s capabilities in advanced manufacturing, aerospace, defense, electronics, and high-precision engineering can also be used for launchers, satellites, ground systems, sensors, propulsion, and secure communications. As advanced manufacturing employment in Europe comes under increasing structural pressure,28 accelerating space market growth offers a high-value industrial transition path, especially for Germany, France, and Italy. NewSpace will not replace European manufacturing but offers a pathway to redeploy parts of the now increasingly freed-up engineering capacities into upstream space production.

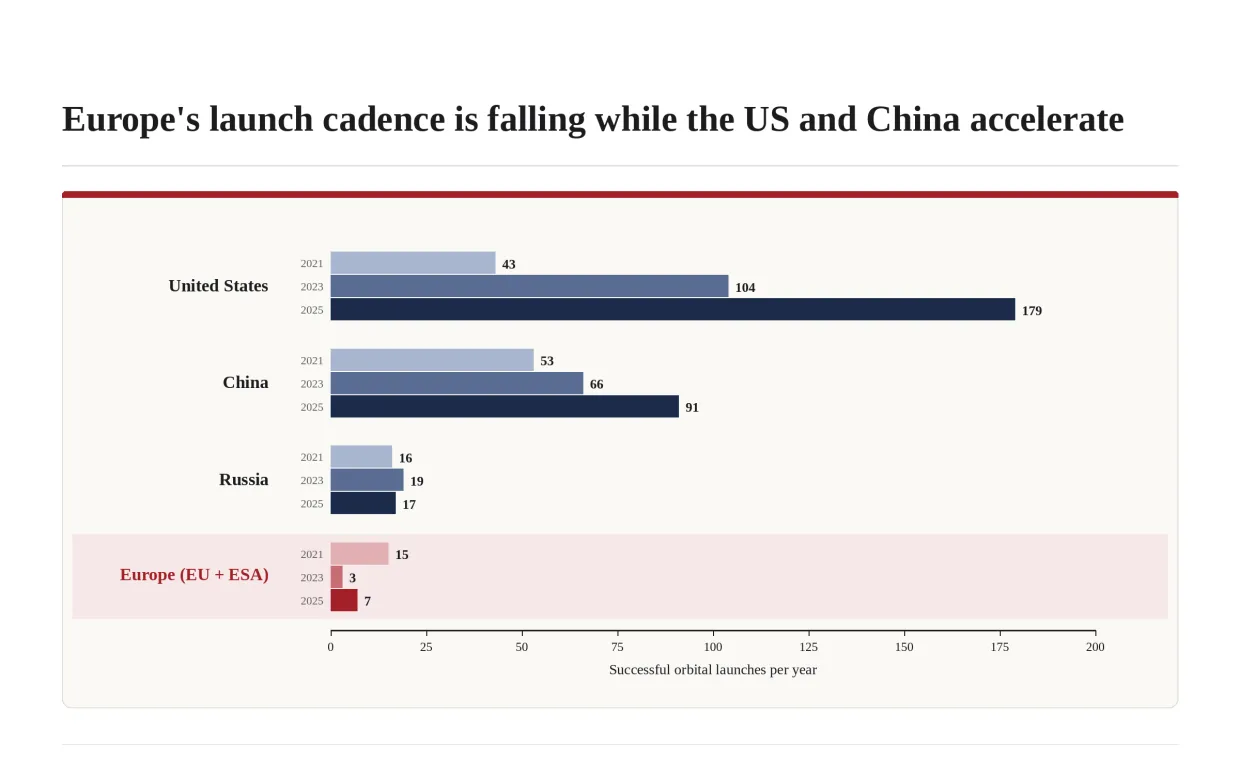

Europe Launches Fewer Rockets in Three Years Than the U.S. Does in a Month

The contrast became stark: Europe launched fewer rockets into orbit in the last three years (13 in 2023-2025) than the U.S. did in a month (15 on average in 2025). For 2025, the U.S. completed ~26 times as many successful rocket launches as Europe. In addition, figure 629 illustrates that this is an ongoing trend of a growing gap, as Europe is the only major launch power whose capacity has decreased since 2021, while the U.S. and China rapidly expanded and Russia stagnated. At the mid-point of the previous decade, Europe was successfully launching six to seven rockets per year via Ariane 5, whereas at the time the U.S. had not yet developed reusable launch vehicles (today the Falcon 9), and therefore was not outpacing European cadence by more than a factor of two. Since then, a steady decline occurred over the next ten years with the gap increasing rapidly since 2022, for three reasons: First, the lack of availability of Soyuz (which had been available as a backup vehicle for European access to space since the early 2000s) caused an immediate disruption beginning in late February 2022. Second, the retirement of Ariane 5 prior to the introduction of its replacement, Ariane 6, resulted in Europe being without a functional means to send payloads to orbit for nearly 12 months.30 Third, SpaceX transformed Falcon 9 into a reusable launch vehicle capable of performing a successful mission approximately every three days. Thus, the European launch capacity remains below the level required to compete.31

Europe Has No DARPA for Space

The Defense Advanced Research Projects Agency (DARPA) is currently funding work on space elevators, large bio-mechanical space structures, and other frontier capabilities that go well beyond procuring satellites.32 These programs place bets on entirely new ways of using orbit. Real European equivalents remain scarce: The privately funded Joint European Disruptive Initiative (JEDI) positions itself as a precursor to a European DARPA and lists space among its mission areas, but has so far only organized prize-style challenges at a fraction of DARPA’s scale. Germany’s Federal Agency for Breakthrough Innovation (SPRIN-D), the only public EU DARPA equivalent, has explicitly asked for more freedom to fund military and dual-use projects.33

Europe’s Launcher Costs and Dependence on U.S. NewSpace Keep Growing

Vulnerability due to external dependencies has increased dramatically over the past five years. This is particularly evident on three levels.

First, the Soyuz launcher cooperation with Russia collapsed in 2022 and will not return. With that collapse Europe has lost a launch option that had functioned for two decades as a load balancer for European missions, and several ESA payloads were postponed or canceled as a result.34

Second, Ariane 6, the successor of the discontinued Ariane 5, is operational but not price competitive, so that the European Commission is preparing a “European preference rule”, as former Internal Market Commissioner Thierry Breton signaled in 2024.35 Pushing European firms to choose the costlier rocket is a defensible short-term measure but does not substitute for (cost) innovation and might establish another burden for EU companies.

The third vulnerable dependency runs to the U.S., both in terms of volatile public-public and public-private relationships. Starlink operates two-thirds of all active satellites (figure 7)36, and delivers crucial connectivity services for both civilian life and military applications. This is not subject to European regulatory oversight, and IRIS² will not deliver similar services before 2030. Public-public dependencies are similarly problematic: The 2025 U.S. National Security Strategy ranks Europe below other regional partners and openly questions whether European partners are strong enough to remain reliable allies.37 Trump’s 2018 remarks about “American Dominance”38 in space have become an active strategy, undermining any potential role Europe could play. The European Council on Foreign Relations’ (ECFR) analysis “Defending Europe with less America” directly addresses the need for a wider U.S.-independent security architecture.39

What the European Commission Should Deliver by 2030

U.S. NewSpace dominance is a result of proactive industrial policies and market interventions that created the environment for innovation drivers like SpaceX to thrive. Europe now holds the same cards: It has extraordinary engineering talent, the production capacity, and – for the first time – the budgetary resources needed to create an environment where NewSpace thrives. The question therefore is: How can the Commission, together with its Member States, establish conditions by 2030 that enable European NewSpace businesses to reach (1) operational maturity, (2) independent access to orbit, and (3) commercial viability?

II. What Europe Has Already Done in Space, and Why It Falls Short

Military Space Commands, the SAFE Instrument, and the EU Space Act

Germany has built more institutional space-defense capacity in the last three years than in the previous thirty. The Bundeswehr Space Command in Uedem runs a satellite operations and control center and processes roughly 75,000 close-approach analyses per year for German military satellites.40 The Bundeswehr is also setting up a Space Academy, a Space Wargaming Center, and the European Space Component Command. In 2024, Germany and France joined Operation Olympic Defender, a U.S.-led space defense coalition.41 In November 2025, France inaugurated its new Space Command (Commandement de l'Espace) facilities in Toulouse, co-locating nine military space units alongside the French space agency (CNES) and the NATO Space Centre of Excellence.42 At the EU level, the European Defence Fund’s space window is growing. The European Council also endorsed the Readiness 2030 white paper in March 2025, and the Security Action for Europe (SAFE) €150 billion defense loan instrument gave Member States co-financing capacity.43 Moreover, the 2025 EU Space Act, now in the legislative process, would for the first time harmonize rules for all civilian and commercial operators in the Union market, addressing the issue of regulatory fragmentation.44

Galileo, Copernicus, and IRIS² on the Civilian Side

The EU Agency for the Space Programme (EUSPA) manages a set of programs that champion Europe’s civilian autonomy. IRIS² and the EU Government Satellite Communications program are the most recent and most strategically important.45 Galileo is technically more accurate than the U.S. Global Positioning System for civilian users. Copernicus is the world’s largest civilian earth observation program. While the Joint Communication on the EU Space Strategy for Security and Defence of March 2023 set the strategic frame for a common European space strategy, SIPRI’s analysis at the time identified the next implementation steps that are now under negotiation.46, 47

Isar Aerospace, ICEYE, and Europe’s Emerging Private Space Sector

The European space industry is no longer dominated only by primes such as Airbus Defence and Space and OHB. Isar Aerospace, PLD Space and Rocket Factory Augsburg are credible launcher companies. The Exploration Company and ICEYE represent the European NewSpace expansion. OroraTech in Munich detects single-tree forest fires from orbit and alerts local fire brigades within minutes.48 SuperVision Earth in Darmstadt monitors pipelines using EU satellite data and AI.49 In Rennes, Unseenlabs uses nanosatellites to track ships that have switched off their transponders, a tool against illegal fishing, ocean dumping and attacks against critical infrastructure.50 Institutional examples include the German Industry Association’s NewSpace initiative and the German Aerospace Center’s startup factory. In Spain, PLD Space’s launcher development is co-funded through the government’s PERTE Aeroespacial program. Despite being starkly behind U.S. levels, private investment in European space ventures has significantly grown in recent years as it more than doubled from 2021 to 2025, despite an 8% decline from 2024 to 2025.51 One way to address the general late-stage funding gap in the EU effectively is France’s Tibi initiative: launched in 2020 and renewed in 2023, it has mobilized roughly €31 billion of institutional capital from insurers and pension funds into French and European venture and growth funds.52

Why Record Space Budgets Do Not Close the Gap with the U.S.

While each of these initiatives shows genuine progress, none of them, on their own or together, are significant enough to nearly close the structural gap between the U.S. and Europe. IRIS² delivery is slipping. Ariane 6, after years of delay, finally flew its first commercial mission in March 2025, five years behind schedule, and still manages only a single-digit annual launch cadence, far below the demand of European institutional payloads, let alone military ones.53 Europe’s first dedicated commercial orbital launch site, Norway’s Andøya Spaceport, hosted its first orbital launch attempt only in March 2025. Several Galileo satellites were launched into orbit by SpaceX rather than by European launch vehicles, demonstrating the dependence at issue. ESA’s geographic return principle, under which industrial contracts to each Member State are awarded in rough proportion to its financial contribution, has historically exacerbated the problem of fragmentation. Following this principle, scarce engineering capacity is distributed across redundant national programs. 2025 NewSpace funding in Europe is roughly one-sixth of U.S. levels (figure 4). The Belfer Critical and Emerging Technology Index ranks Europe particularly far behind in space, and CSIS’s Europe Corner analysis of structural dependency reaches the same conclusion.54 Europe lacks both a procurement vehicle for high-risk frontier technology, equivalent to the U.S. DARPA, and a standards body for interoperability of operational constellations. The Draghi report also mentions that structural reform, strategic investment, and independent launch capability are the missing parts for a sovereign European space sector.55 While there is significant European investment by now, it stays fragmented across Member State programs, moves slowly, is still small compared to the U.S., and remains exposed to political volatility across the Atlantic.56

III. Lessons from Ukraine, Russian Gray-Zone Attacks, and Airbus

In Ukraine, Commercial Satellites Became Military Infrastructure

The war in Ukraine is the first large-scale war where commercial space services play a crucial role in combat. This novelty dramatically exposes the vulnerabilities of space dependencies. On the morning of February 24, 2022, for example, just before the first strikes took place, a Russian cyberattack against Viasat’s KA-SAT ground network disrupted the satellite communications relied upon by the Ukrainian military leadership and a number of civilian users in Europe.

Over the past years, commercial earth observation imagery from firms such as ICEYE, Vantor (formerly Maxar), and Planet gave Ukrainian forces real-time visibility of Russian dispositions, while Starlink terminals provided crucial constant connectivity. The line between commercial and military use cases has blurred even further, and the operator of a capability becomes more important as it is now a corporation or even an individual CEO who ultimately decides when and how an existential service is delivered.57

Jamming and Spoofing Have Become Routine

The Belfer Center’s February 2026 assessment of threats to NATO’s eastern flank documents in detail how orbital interference became a crucial part of Moscow’s gray-zone toolkit.58 The threshold for orbital escalation has dropped, as shown by persistent jamming and spoofing of Galileo and GPS signals over the Baltic and the Black Sea, suspected close-proximity operations against Western reconnaissance satellites, and Moscow’s reported work on a nuclear anti-satellite capability.59 The Bundeswehr Space Command in Uedem, for example, records weekly interference attempts against European systems.60 Europe right now has neither a doctrine for responding nor the capacity to properly attribute these attacks.

The Airbus Playbook for European Space

When the A300 entered service in 1974, Airbus was a marginal newcomer against American manufacturers who controlled more than 90% of the market. Fifty years later, Airbus dominates the commercial aircraft market with 56% share, 16 percentage points more than Boeing.61 This success story was only possible because of a shared European political effort. This required long-term public investment, stable demand from European flagship airlines, financing from the European Investment Bank (EIB), and procurement rules that gave a young industry room to grow. The same logic applies to space today. Bruegel’s industrial-policy work on the European space sector concludes that Europe’s binding constraint is institutional. Europe has exceptional engineering talent but needs the necessary financing instruments, procurement rules, and pooled demand to turn that talent into sustained and effective space innovation.62 The European Parliamentary Research Service’s (EPRS) 2050 scenarios assessment comes to a similar conclusion: in every long-run scenario short of decisive industrial-policy action, Europe ends up as a follower in space.63

These lessons show that the future of the European NewSpace sector is primarily a matter of industrial policy. Policy instruments that have been used to date in the fields of civil aviation, semiconductors, and electric mobility (e.g., anchor demand, joint procurement, or funding for groundbreaking research) can also – in an adapted form – be applied to the space industry.

IV. Five Recommendations for European Space Policy

The five recommendations below are sequenced in order. Recommendations 1 and 2 build the financial foundation for NewSpace to reach scale; Recommendation 3 establishes the political and cultural conditions for these reforms to survive their first failures by 2029; Recommendation 4 reduces the dependencies and addresses the robustness needed by 2029. Finally, recommendation 5 creates an integrated European – not multi-national – space sector by 2030.

1. Space-RIN-EU, a European DARPA for Space

Europe lacks an institutional vehicle for high-risk, mission-driven deeptech space research similar to U.S. equivalents like DARPA, the Advanced Research Projects Agency–Energy (ARPA-E), and NASA’s Space Technology Mission Directorate. ESA’s procurement frameworks (cost-plus and geographic returns) by design strongly advantage incumbents over NewSpace companies.64 The European Innovation Council Pathfinder funds early-stage research in all sectors but is not equipped with sufficient capital for the capital-intensive investments that frontier space technology requires. The result is that DARPA funds work on entirely new ways of using orbit (such as space elevators), while Europe has no equivalent answer.65 According to the Draghi report, this gap is one of the missing pillars of a credible European space strategy.66

The Commission should support the founding of “Space-RIN-EU”67 by 2028. The operating model should follow Germany’s SPRIN-D, the only EU agency that has implemented the DARPA logic in practice, with program-manager autonomy, hard kill criteria, milestone-based contracts, and a dual-use mandate.68 Governance should be modeled on the Airbus precedent: an intergovernmental consortium founded by the major European space powers Germany, France, Italy, and Spain, with a strategic council of Member States, and the Commission as co-financing partner. Funding should be pooled over a ten-year period at a rate of €1 billion per year, drawn from national contributions and the Multiannual Financial Framework (MFF).

Sites should be spread across Member States (following the Airbus model) but contracts should not be distributed based on a national quota. The headquarters could be located in Toulouse, with major program offices in Munich, an Italian site in Turin or Rome and a Spanish site in Seville or Madrid. Space-RIN-EU should focus on reusable launches, in-orbit assembly, satellite imagery, quantum-secured communications, and debris removal. To preserve the dual-use character of the program, civilian applications should carry at least the same weight as defense use cases.

2. A €10-Billion Late-Stage Space Fund and NASA-Style Fixed-Price Procurement

The Commission and the European Investment Bank should establish a €10-billion Late-Stage Space Investment Fund modeled on the NATO Innovation Fund, the first multi-sovereign deeptech fund of its kind, founded in 2022, with 24 Member State backers today. With check sizes of €100 million to €1 billion, the new fund should target Series C and later rounds in European NewSpace and dual-use orbital deeptech and be able to lead those rounds. It should operate at arm’s length from political institutions and have a private-sector investment committee as well as market-rate return targets. SpaceX’s IPO reached a valuation of ~$1.8 trillion; a European fund of this kind keeps the upside of the next equivalent in European hands.

The Commission is already investing in space: since 2022, the €1-billion CASSINI Investment Facility has already allocated capital to thirteen European venture capital funds69 and co-invested with them directly in ICEYE and Isar Aerospace.70 From autumn 2026 onward, the €5 billion Scaleup Europe Fund will invest in ten different deeptech sectors, including space.71 Those funds, however, are too small or fragmented to lead a €500-million+ NewSpace round. The same applies to the European Innovation Council’s STEP Scale Up scheme that invests up to €30 million. The proposed late-stage fund would take over at that point, setting terms and holding reserves for the follow-on rounds that carry a company from Series C to commercial maturity.

In addition to the late-stage fund, the Commission and ESA should establish a procurement framework to also address the early traction problem. Modeled on NASA Commercial Resupply Services (CRS), a European NewSpace procurement framework with milestone-based fixed-price contracts, multi-year demand commitments, IP retained by the contractor for parallel commercial use, and qualification timelines compressed to start-up reality should be developed. ESA’s Boost! and European Launcher Challenge initiatives provide a starting template but need to be enlarged by an order of magnitude. Procurement modes not only define early survival, company valuations, and funding probabilities, but also business model incentives of NewSpace launch companies: cost-plus rewards cost growth, while milestone-based fixed-price forces efficiency.

The two components are interdependent. Capital without anchor demand produces overvalued companies that miss product-market fit; anchor demand without capital produces companies that win contracts but cannot finance the build-out. Implementing both components could give European NewSpace firms like Isar Aerospace, EnduroSat, Aerospacelab, or Cailabs a path to operational maturity under European ownership.

3. A Culture Shift Toward More Civilian Focus and Failure Acceptance

European space culture has two main issues. First, it is too risk-averse (not accounting for the necessary failures of NewSpace ventures). While a benevolent procurement model and venture financing played an important role in SpaceX’s success, its institutional advantage also came from a culture of acceptance that frontier space programs fail before they succeed. Examples include Falcon 1, which failed three times before reaching orbit, and Starship, which had multiple losses in flight tests. Europe’s reflex is the opposite. As is typical for maiden flights, Isar Aerospace’s Spectrum was lost roughly 30 seconds after its first liftoff in March 2025. Instead of treating the test as a successful, data-rich engineering milestone, parts of the European political and media commentary framed it as evidence that European NewSpace cannot compete.72

To establish a European culture of failure tolerance, milestone-based contracts under the new “NewSpace Procurement” concept (recommendation 2) should explicitly provide funding for a specified number of failed tests as planned milestones rather than as contract breaches.

Drawing on NASA’s standard practice of treating losses as engineering data collection, the Commission should also publish a Frontier Space Programs Communication Protocol that specifies how Member State governments and EU institutions communicate test failures.

Additionally, drawing on NASA TV / NASA+, the Commission should partner with the European Broadcasting Union (EBU) to turn European launches into continent-wide media events, with live feeds, briefings, and contextual materials (including the meaning of potential failures) in all official languages distributed through the Eurovision network, and Member State public broadcasters.

The second main issue with European space culture is that it is too defense-focused (not highlighting important civilian use cases like ICEYE’s flood-monitoring services). Public support for public space investment in Europe is likely much stronger when the civilian dimension – climate monitoring, wildfire detection, agricultural yield modeling, search and rescue, broadband for underserved regions, disaster response – is clearly visible.

The Commission should therefore fund a €10-million EU space education package over the next MFF period. Most of that money would be invested into module development in the first two years, with a smaller annual budget for updates after that. Modules would be produced with ESA and adapted by Member States for their own science and civics standards, with Erasmus+ co-funding for states that take them up, by 2028. In geography class, Copernicus data behind wildfire alerts could be used to show how space affects our daily lives. The Isar Aerospace Spectrum flight – which was lost 30 seconds after launch – could be used in physics class to demonstrate how valuable data is collected even from failed launches.73

Every program funded under SAFE, the European Defence Fund, or the next MFF should be required to define and report against a measurable portfolio of civilian applications, with concrete outcome metrics. Part of the measurement infrastructure exists: EUSPA’s EU Space Market Report already focuses on quantifying downstream markets by application and region but falls short of showing the actual impact of the technologies on local populations.74 Modeled on the EU Climate Action Progress Report and published as a companion to the Market Report, an annual European Space Civilian Outcomes report should aggregate these metrics across Member States and feed back into future funding decisions by 2029. Measured Key Performance Indicators (KPIs) could include: the share of EU-funded programs with a defined civilian portfolio and their downstream volumes (hectares under wildfire watch, flood alerts issued, population covered by satellite broadband); a Eurobarometer item on public awareness; the count of test failures funded as planned milestones; and adoption of the ESA teaching modules with the share of secondary students reached.

4. Annual Public Robustness Tests of Europe’s Space Dependencies

The European Commission and the European Defence Agency should jointly publish, every twelve months, a classified and an unclassified version of a robustness test that maps the dependencies of European civilian and military capabilities on non-European space technology services. The exercise should answer, in numerical detail, for example: the exact number and share of Member State military communications channels that currently route through commercial U.S. constellations; the share of Galileo and Copernicus traffic that could be denied by known Russian electronic-warfare capabilities; the European industrial capacity that exists to replace each dependency within twenty-four months; and the resulting financing gap. The unclassified summary should be a public document. This would complement groundwork: since 2008, a Joint Task Force of the Commission, ESA, and the European Defence Agency (EDA) has mapped critical space technology dependencies at the component level,75 most recently in the 2024-2026 action lists, and the EU Observatory of Critical Technologies tracks the related supply-chain risks. Extending mapping with a technology focus is critical: the war in Ukraine has shown how costly unaddressed dependencies can be, and transparency research (e.g., on the effects of PISA study publications) has shown that the publication of performance gaps can trigger far-reaching political action, especially when gaps are not publicly well-known.76

5. Binding Technical Interoperability Standards

Fragmentation is now the largest single source of inefficiency in European space procurement. Any Member State constellation that has its own command interface, encryption stack, or ground segment design incurs duplicative costs and slows down response capabilities in case of crises. However, governmental and military constellations are the area the EU Space Act deliberately excludes. Hence, the EU should establish an interoperability standards package, modeled on NATO requirements but enforceable under EU law. This should cover satellite platform interfaces, in-orbit refueling and servicing standards, and encryption. EUSPA, in coordination with the European Defence Agency and ESA, should run a European Space Domain catalog. Member States should be required to contribute national space-surveillance data, with the catalog drawing on the close-approach work already performed by the Bundeswehr Space Command in Uedem and analogous national centers,77 and federated with the NATO Space Centre. These standards should apply not only across governments but also between governmental and commercial systems, for use cases in which commercial satellites need to communicate securely with governmental ones, a requirement already discussed in the U.S. debate.78 A standing public-attribution protocol should publish detected interference incidents on a regular basis, with classified details retained but aggregate statistics public, so that low-cost harassment becomes politically costly.79

The Politics of Implementation

In contrast to the U.S. or China, where decisions can be made relatively centrally, von der Leyen needs to address key challenges arising from a multi-state legislative system like the EU.

The most important challenge to be addressed will be “juste retour”, the principle that individual Member State contributions are roughly met by returns in the respective contributor states. Recommendations 1 and 2 break with this principle: Milestone-based procurement and a late-stage fund award money on performance and competitiveness, not on country of origin. Smaller countries may consider the recommended initiatives as transfers to the space hubs Toulouse and Munich, which effectively – to a certain extent – would also be true. The EU Commission should address this by deliberately including Member States that benefit less from funding opportunities in decisions over program offices, test infrastructure, and qualification facilities. Early access to the interoperability standards under recommendation 5 would give smaller-country suppliers a defined role in every future European constellation. While it will not fully solve the juste retour problem, it offers the Commission a valuable currency for the 2028 MFF negotiation, which would be the right place to put forward a proposal.

A second challenge is institutional: ESA answers to its own Member States, three of which (Norway, Switzerland, and the United Kingdom) are not part of the Union, and any move of procurement authority toward the Commission opens a dispute about competence. This is the reason Space-RIN-EU (recommendation 1) is institutionally designed as an intergovernmental consortium rather than an EU agency: its backbone is ten-year national contributions that do not expire with the 2028-2034 framework, topped up by a Commission share renegotiated with each MFF. This would secure Union leverage without triggering the treaty questions that a new agency would. Recommendation 2 applies the same logic to the EIB, following the NATO Innovation Fund, which was established by coalition, not unanimous decision.80

The third source of resistance is Member States with neutrality regimes and/or strongly anchored militarization opposition in their respective populations. Austria, Ireland, and Malta are likely to resist any initiative that reads as militarization through the EU budget. Civilian and dual-use requirements, as established in recommendations 1 and 3, are important levers to address these concerns. Civilian application reporting as suggested in recommendation 3 increases awareness about the civilian value proposition of space technology in the respective Member State populations. When civilian application use cases are still insufficient, the SAFE instrument already allows Member States to separate defense co-financing from the general budget. It is accordingly possible for a neutral Member State to abstain from the defense window without vetoing whole initiatives.

None of this removes the risk that a first launch failure or a cost overrun collapses the coalition. That makes a deliberate communication strategy as outlined in recommendation 3 essential. When Airbus was founded in 1970, it faced comparable problems. It ultimately succeeded because the founding governments engineered the politics as carefully as the aircraft.

V. Conclusion

The European Union is investing in space at a scale that did not exist three years ago. Readiness 2030 and the SAFE instrument provide crucial financing. IRIS² and Galileo show the institutional foundations that are already in place. A young EU NewSpace sector in cities such as Munich and Toulouse provides the technical base for space innovation at greater scale. Private space tech venture capital investments are accelerating even further in 2026, with the latest data suggesting that the total European funding in the second quarter of 2026 exceeds full-year 2025 funding.81 The missing piece for the EU is a unified, proactive industrial policy for the space sector.

The five recommendations in this brief can be acted on within forty-eight months. First, the Commission should establish the institutional and financial foundations through Space-RIN-EU and a Late-Stage Space Investment Fund and pair them with venture-friendly procurement. The next priority should be that reforms survive their first necessary setbacks. This happens through a cultural shift, reframing space as a civilian public-good mission and institutionalizing a European failure culture. Last, the EU should focus on establishing stable and sustainable capabilities, with annual robustness tests and binding interoperability standards. The whole package is built on the financing instruments that are already in place or imminent.

The cost of inaction is easily foreseeable. By 2030, Europe will depend on a single American company for satellite communications more than it has depended on any state or multi-state alliance at any point in the post-1945 order. At the same time, Russian and Chinese counter-space capabilities will be more developed, and the orbital commons will be more congested. Economically, the European share of the projected $1.8 trillion space economy will be smaller than it is today, missing out on a huge opportunity.82 The EPRS 2050 scenarios reach the same conclusion from a different angle: in every plausible long-run path short of decisive action now, Europe ends up as a follower in space.83

In 1974, it seemed far-fetched that Airbus, with hardly any market share, would eventually succeed against the overwhelming U.S. dominance in the commercial aircraft manufacturing sector. Its extraordinary rise since then was only possible because Europe institutionally designed the conditions through patient public investment, anchor demand, rules that gave a young industry room to grow, and a shared European spirit of cooperation. By applying both the joint intergovernmental efforts and the capacity to shape institutions – within the framework of President von der Leyen’s current mandate and Commissioner Kubilius’s first operational results – to the space sector, the conditions for a European counterpart to SpaceX can be created.

Recommended citation

Sedlmayr, Fabian and Robert Platow. “Europe’s Falcon Moment: Five Recommendations to Create the Conditions for Europe’s Own SpaceX.” July 28, 2026

Footnotes

- Following SpaceX's merger with xAI in February 2026, the company’s valuation also reflects non-space business lines. A like-for-like comparison with pure-play space ventures would therefore be somewhat lower, though the order of magnitude remains unchanged.

- For readability, this paper uses “Europe” and “the EU” interchangeably unless the distinction is relevant, in which case it is made explicit.

- Traut, M. (2025) “Der Weltraum war noch nie friedlich”. Available at: https://www.spiegel.de/wissenschaft/mensch/bundeswehr-bereitet-sich-auf-krieg-im-weltraum-vor-wir-haben-geld-aber-keine-zeit-a-e820db05-fe05-4f81-b02d-f2db59e5cae9 (Accessed: 20 July 2026).

- United States Space Force (n.d.) “Space Based Infrared System”, Fact Sheet. Available at: https://www.spaceforce.mil/about-us/fact-sheets/article/2197746/space-based-infrared-system/ (Accessed: 20 July 2026).

- Freedberg, S.J. (2025) “Close the gap: Turn the Franco-German missile early warning into measurable capability”, Breaking Defense, 2 October. Available at: https://breakingdefense.com/2025/10/close-the-gap-turn-the-franco-german-missile-early-warning-into-measurable-capability/ (Accessed: 20 July 2026).

- European Commission, Directorate-General for Defence Industry and Space (2023) “ODIN'S EYE II”, European Defence Fund 2022 project factsheet. Available at: https://defence-industry-space.ec.europa.eu/system/files/2023-06/ODINS'EYE%20II-Factsheet_EDF22.pdf (Accessed: 20 July 2026).

- McKinsey & Company (2024) “Space: The 1.8 Trillion-Dollar Opportunity”. Available at: https://www.mckinsey.com/industries/aerospace-and-defense/our-insights/space-the-1-point-8-trillion-dollar-opportunity-for-global-economic-growth (Accessed: 20 July 2026).

- Harrison, T. (2026) “Satellites”, AEI Space Data Navigator, American Enterprise Institute, data as of 11 July. Available at: https://spacedata.aei.org/space/satellites (Accessed: 20 July 2026).

- Maritime Executive (2024) “Maersk Gives its Seafarers Starlink Internet”. Available at: https://www.maritime-executive.com/article/maersk-gives-its-seafarers-starlink-internet (Accessed: 20 July 2026).

- Journal Aviation (2026) “Lufthansa Group Also Chooses Starlink Connectivity”, 14 January. Available at: https://www.journal-aviation.com/en/air-transport-news/connectivity-and-ife/lufthansa-group-also-chooses-starlink-connectivity-20260114.html (Accessed: 20 July 2026).

- Foust, J. (2024) “Europe signs contracts for IRIS² constellation”, SpaceNews, 16 December. Available at: https://spacenews.com/europe-signs-contracts-for-iris²-constellation/ (Accessed: 20 July 2026).

- EU Member States with relevant space spending: France, Germany, and Italy.

- Novaspace (2025) Defense spending drives government space budgets to historic high: 24th edition of Government Space Programs. Paris: Novaspace, 21 January 2025. Available at: https://nova.space/press-release/defense-spending-drives-government-space-budgets-to-historic-high/ (Accessed: 20 July 2026).

- Novaspace (2026) Global space spending reaches $137B, marking a defense-led era: 25th edition of Government Space Programs. Paris: Novaspace, 20 January 2026. Available at: https://nova.space/press-release/global-space-spending-reaches-137b-marking-a-defense-led-era/ (Accessed: 20 July 2026).

- European Space Agency (2026) ESA Report on the Space Economy 2026. Paris: European Space Agency. Available at: https://www.esa.int/About_Us/Business_with_ESA/ESA_releases_2026_Space_Economy_Report (Accessed: 20 July 2026).

- European Space Agency (2025) “ESA Member States commit to largest contributions at Ministerial”, European Space Agency, 27 November. Available at: https://www.esa.int/About_Us/Corporate_news/ESA_Member_States_commit_to_largest_contributions_at_Ministerial (Accessed: 20 July 2026).

- Secrétariat général de la défense et de la sécurité nationale (2024) “National Space Strategy”, Government of France. Available at: https://www.sgdsn.gouv.fr/files/files/Publications/National%20space%20strategy_ENG.pdf (Accessed: 20 July 2026).

- Bundesministerium der Verteidigung (2025) “Nationale Weltraumsicherheitsstrategie”. Available at: https://www.bmvg.de/de/aktuelles/erste-weltraumsicherheitsstrategie-der-bundesregierung-6042422 (Accessed: 20 July 2026).

- Harrison, T. (2026) “Satellites”, AEI Space Data Navigator, American Enterprise Institute, data as of 11 July. Available at: https://spacedata.aei.org/space/satellites (Accessed: 20 July 2026).

- Assuming a continued growth of active satellites over the next 4.5 years (midyear 2026 until 2030) at the same ~30.5% CAGR as in the prior period (2021 until midyear 2026). Calculations based on the unrounded figures.

- Boley, A. C. and Byers, M. (2021) “Satellite mega-constellations create risks in Low Earth Orbit, the atmosphere and on Earth”, Scientific Reports, 11(1), 10642. Available at: https://doi.org/10.1038/s41598-021-89909-7 (Accessed: 20 July 2026).

- ESPI (2026) “Space Venture 2025 - Global Investment Dynamics”, ESPI Report 102, April. Available at: https://www.espi.eu/wp-content/uploads/2026/04/Space-Venture-2025_Final_April.pdf (Accessed: 20 July 2026).

- European Space Agency Commercialisation (2026) “Boost! — Commercial Space Transportation Services Element”. Available at: https://commercialisation.esa.int/opportunities/boost-1-commercial-space-transportation-services-element/ (Accessed: 20 July 2026).

- European Space Agency (2026) “European Launcher Challenge”. Updated 12 March 2026. Available at: https://www.esa.int/Enabling_Support/Space_Transportation/European_Launcher_Challenge (Accessed: 20 July 2026).

- European Space Agency (2026) “Report on the Space Economy 2026”. Available at: https://www.esa.int/About_Us/Business_with_ESA/ESA_releases_2026_Space_Economy_Report (Accessed: 20 July 2026).

- Harrison, T. (2026) “Satellites”, AEI Space Data Navigator, American Enterprise Institute, data as of 11 July. Available at: https://spacedata.aei.org/space/satellites (Accessed: 20 July 2026).

- McDowell, J. (2026) “Space Activities in 2025”. Available at: https://planet4589.org/space/papers/space25.pdf (Accessed: 20 July 2026).

- Eurofound (2025) “Living and Working in Europe 2024”, EF25036EN. Available at: https://assets.eurofound.europa.eu/f/279033/513b319511/ef25036en_en.pdf (Accessed: 20 July 2026).

- McDowell, J. (2026) “Space Activities in 2025”. Available at: https://planet4589.org/space/papers/space25.pdf (Accessed: 20 July 2026).

- From July 2023 to July 2024.

- European Centre for International Political Economy (2026) “Europe's Space Strategy for the 21st Century”, Policy Brief, April. Available at: https://ecipe.org/publications/europes-space-strategy-for-21st-century/ (Accessed: 20 July 2026).

- DARPA (2025) “Novel Tech for Space Structures”. Available at: https://www.darpa.mil/news/2025/novel-tech-space-structures (Accessed: 20 July 2026).

- SPRIN-D (2025) “Position SPRIN-D-Mil”. Available at: https://www.sprind.org/worte/magazin/position-sprind-mil (Accessed: 20 July 2026).

- Center for Strategic and International Studies (2025) “Strategic Ambition vs. Structural Dependency: Why Europe Can’t Stand Alone in Space". Available at: https://www.csis.org/blogs/europe-corner/strategic-ambition-vs-structural-dependency-why-europe-cant-stand-alone-space (Accessed: 20 July 2026).

- Politico (2024) “How Europe Screwed Up Its Rocket Program”, 10 July. Available at: https://www.politico.eu/article/how-europe-screwed-up-its-rocket-program (Accessed: 20 July 2026).

- Harrison, T. (2026) “Satellites”, AEI Space Data Navigator, American Enterprise Institute, data as of 11 July. Available at: https://spacedata.aei.org/space/satellites (Accessed: 20 July 2026).

- The White House (2025) “National Security Strategy of the United States of America”, November. Available at: https://www.whitehouse.gov/wp-content/uploads/2025/12/2025-National-Security-Strategy.pdf (Accessed: 20 July 2026).

- The White House (2018) “Remarks by President Trump at a Meeting of the National Space Council and Signing of Space Policy Directive-3”, 18 June. Available at: https://trumpwhitehouse.archives.gov/briefings-statements/remarks-president-trump-meeting-national-space-council-signing-space-policy-directive-3/ (Accessed: 20 July 2026).

- European Council on Foreign Relations (2024) “Defending Europe with less America”. Available at: https://ecfr.eu/publication/defending-europe-with-less-america/ (Accessed: 20 July 2026).

- Bundeswehr Luftwaffe (no date) “Weltraumsicherheit”. Available at: https://www.bundeswehr.de/de/organisation/luftwaffe/aktuelles/weltraum-sicherheit-6005072 (Accessed: 20 July 2026).

- SpaceNews (2024) “France and Germany Join U.S.-Led Space Defense Coalition”. Available at: https://spacenews.com/france-and-germany-join-u-s-led-space-defense-coalition/ (Accessed: 20 July 2026).

- Ministère des Armées (2025) “Inauguration of the Space Command Facilities — Inaugural Declaration”, Commandement de l'Espace, 12 November. Available at: https://www.defense.gouv.fr/en/cde/actualites/inauguration-installations-du-commandement-lespace-12-novembre-2025-declaration-sa-premiere (Accessed: 20 July 2026).

- European Council (2025) “Readiness 2030 / SAFE proposal”. Available at: https://defence-industry-space.ec.europa.eu/eu-defence-industry/white-paper-european-defence-readiness-2030_en (Accessed: 20 July 2026).

- European Commission (2025) “Proposal for a Regulation of the European Parliament and of the Council on the safety, resilience, and sustainability of space activities in the Union”, 25 June. Available at: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex:52025PC0335 (Accessed: 20 July 2026).

- EUSPA (no date) “IRIS² (Infrastructure for Resilience, Interconnectivity and Security by Satellite)”. Available at: https://www.euspa.europa.eu/eu-space-programme/secure-satcom/iris2 (Accessed: 20 July 2026).

- European Commission (2023) “Joint Communication on a European Union Space Strategy for Security and Defence”, March. Available at: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex:52023JC0009 (Accessed: 20 July 2026).

- Portela, C. and González Muñoz, R. (2023) “The EU Space Strategy for Security and Defence: Towards Strategic Autonomy?”, EU Non-Proliferation and Disarmament Paper No. 83, June. Stockholm: SIPRI. Available at: https://www.sipri.org/publications/2023/eu-non-proliferation-and-disarmament-papers/eu-space-strategy-security-and-defence-towards-strategic-autonomy (Accessed: 20 July 2026).

- OroraTech (no date) “Wildfire Solutions”. Available at: https://ororatech.com/all-products/wildfire-solution (Accessed: 20 July 2026).

- SuperVision Earth (no date) “Our Company”. Available at: https://www.supervision.earth/ourcompany (Accessed: 20 July 2026).

- Roukoz, J. (2026) “Successful Launch: BRO-21 expands Unseenlabs' Satellites Constellation for Radio Frequency Detection”, EDR Magazine, 4 May. Available at: https://www.edrmagazine.eu/successful-launch-bro-21-expands-unseenlabs-satellites-constellation-for-radio-frequency-detection (Accessed: 24 July 2026).

- ESPI (2026) “Space Venture 2025 - Global Investment Dynamics”, ESPI Report 102, April. Available at: https://www.espi.eu/wp-content/uploads/2026/04/Space-Venture-2025_Final_April.pdf (Accessed: 20 July 2026).

- Reuters (2026) “France mobilises €13 billion for tech sovereignty funding push”, 19 June. Available at: https://www.reuters.com/business/media-telecom/france-mobilises-13-billion-tech-sovereignty-funding-push-2026-06-19/ (Accessed: 24 July 2026).

- Politico (2024) “How Europe Screwed Up Its Rocket Program”. Available at: https://www.politico.eu/article/how-europe-screwed-up-its-rocket-program (Accessed: 20 July 2026).

- Belfer Center (2025) “Critical and Emerging Technology Index”, June. Available at: https://www.belfercenter.org/critical-emerging-tech-index (Accessed: 20 July 2026).

- Draghi, M. (2024) “The future of European competitiveness”, Report to the European Commission, September. Available at: https://commission.europa.eu/topics/eu-competitiveness/draghi-report_en (Accessed: 20 July 2026).

- Center for Strategic and International Studies (2025) “Strategic Ambition vs. Structural Dependency: Why Europe Can’t Stand Alone in Space”. Available at: https://www.csis.org/blogs/europe-corner/strategic-ambition-vs-structural-dependency-why-europe-cant-stand-alone-space (Accessed: 20 July 2026).

- Radin, A., Holynska, K., Tretter, C. and Van Bibber, T. (2025) Lessons from the War in Ukraine for Space: Challenges and Opportunities for Future Conflicts. RR-A2950-1. Santa Monica, CA: RAND Corporation. Available at: https://www.rand.org/pubs/research_reports/RRA2950-1.html (Accessed: 20 July 2026).

- Belfer Center (2026) “Russian Threats to NATO's Eastern Flank”, February. Available at: https://www.belfercenter.org/research-analysis/russia-nato-baltics-scenarios-europe-security (Accessed: 20 July 2026).

- Der Spiegel (2026) “Bundeswehr bereitet sich auf Krieg im Weltraum vor”, 6 April. Available at: https://www.spiegel.de/wissenschaft/mensch/bundeswehr-bereitet-sich-auf-krieg-im-weltraum-vor-wir-haben-geld-aber-keine-zeit-a-e820db05-fe05-4f81-b02d-f2db59e5cae9 (Accessed: 20 July 2026).

- Bundeswehr Luftwaffe (no date) “Weltraumsicherheit”. Available at: https://www.bundeswehr.de/de/organisation/luftwaffe/aktuelles/weltraum-sicherheit-6005072 (Accessed: 20 July 2026).

- Spray, A. (2025) “How Airbus & Boeing Aircraft Production Has Changed Over The Past Decade”, Simple Flying, 19 April. Available at: https://simpleflying.com/how-airbus-boeing-production-changed-over-past-decade/ (Accessed: 24 July 2026).

- Bruegel (2025) “Satellites and space races: the role of Europe in the space economy”. Available at: https://www.bruegel.org/podcast/satellites-and-space-races-role-europe-space-economy (Accessed: 20 July 2026).

- European Parliamentary Research Service (2025) “Space 2050: Scenarios for the European Union”. Available at: https://www.europarl.europa.eu/RegData/etudes/IDAN/2025/765792/EPRS_IDA(2025)765792_EN.pdf (Accessed: 20 July 2026).

- European Centre for International Political Economy (2026) “Europe's Space Strategy for the 21st Century”, Policy Brief, April. Available at: https://ecipe.org/publications/europes-space-strategy-for-21st-century/ (Accessed: 20 July 2026).

- DARPA (2025) “Novel Tech for Space Structures”. Available at: https://www.darpa.mil/news/2025/novel-tech-space-structures (Accessed: 20 July 2026).

- Draghi, M. (2024) “The future of European competitiveness”, Report to the European Commission, September. Available at: https://commission.europa.eu/topics/eu-competitiveness/draghi-report_en (Accessed: 20 July 2026).

- The suggested name builds on the German SPRIN-D template. “RIN” stands for “Consortium for Radical Innovation” translating consistently as radikale Innovation (GER), innovation radicale (FR), innovación radical (SPA), and innovazione radicale (ITA), and lends itself to a shared “space rhino” brand identity and mascot.

- SPRIN-D (2025) “Position SPRIN-D-Mil”. Available at: https://www.sprind.org/worte/magazin/position-sprind-mil (Accessed: 20 July 2026).

- European Commission, Directorate-General for Defence Industry and Space (2024) “OBSERVER: Exploring the CASSINI Space Entrepreneurship Initiative”, EU Space Policy, 16 August. Available at: https://eu-space.europa.eu/news/observer-exploring-cassini-space-entrepreneurship-initiative (Accessed: 20 July 2026).

- Jonsson, T.S. (2023) “CASSINI Space Entrepreneurship Initiative 2021-2027”, European Commission, Directorate-General for Defence Industry and Space, presentation, October, slide 7. Available at: https://commercialisation.esa.int/wp-content/uploads/2023/10/Jonsson_Space-Entrepreneurship.pdf (Accessed: 20 July 2026).

- European Innovation Council (no date) “Scaleup Europe Fund”. Available at: https://eic.ec.europa.eu/eic-fund/scaleup-europe-fund_en (Accessed: 20 July 2026).

- On the Isar Aerospace Spectrum test flight of March 30, 2025, the vehicle was lost approximately 30 seconds after liftoff from Andøya. Both the company and ESA classified the test as a successful first attempt that delivered substantial flight data.

- Spectrum Flight 2 (“onwards and upwards”) is scheduled for late July or early August 2026.

- European Union Agency for the Space Programme (2026) EU Space Market Report 2026, Issue 1. Luxembourg: Publications Office of the European Union. Available at: https://doi.org/10.2878/6211309 (Accessed: 21 July 2026).

- European Commission, Directorate-General for Defence Industry and Space (no date) “Technological Non-Dependence”. Available at: https://defence-industry-space.ec.europa.eu/technological-non-dependence_en (Accessed: 24 July 2026).

- Martens, K. and Niemann, D. (2013) “When Do Numbers Count? The Differential Impact of the PISA Rating and Ranking on Education Policy in Germany and the US”, German Politics, 22(3), pp. 314–332. Available at: https://doi.org/10.1080/09644008.2013.794455 (Accessed: 24 July 2026).

- Bundeswehr Luftwaffe (no date) “Weltraumsicherheit”. Available at: https://www.bundeswehr.de/de/organisation/luftwaffe/aktuelles/weltraum-sicherheit-6005072 (Accessed: 20 July 2026).

- Machi, V. (2021) “US Military Places a Bet on LEO for Space Security”, Space Development Agency, 25 May. Available at: https://www.sda.mil/us-military-places-a-bet-on-leo-for-space-security/ (Accessed: 20 July 2026).

- Der Spiegel (2026) “Bundeswehr bereitet sich auf Krieg im Weltraum vor”, 6 April. Available at: https://www.spiegel.de/wissenschaft/mensch/bundeswehr-bereitet-sich-auf-krieg-im-weltraum-vor-wir-haben-geld-aber-keine-zeit-a-e820db05-fe05-4f81-b02d-f2db59e5cae9 (Accessed: 20 July 2026).

- Twenty-two of NATO's then thirty allies signed the founding commitment at the Madrid Summit on 30 June 2022; twenty-three had become limited partners by August 2023, and the fund is today backed by twenty-four of thirty-two allies, all of them European. NATO as an organization neither invests in nor participates in the governance of the fund.

- Dealroom (2026) “Space tech in Europe”. Available at: https://dealroom.co/guides/space-tech-europe (Accessed: 20 July 2026).

- McKinsey & Company (2024) “Space: The 1.8 Trillion-Dollar Opportunity”. Available at: https://www.mckinsey.com/industries/aerospace-and-defense/our-insights/space-the-1-point-8-trillion-dollar-opportunity-for-global-economic-growth (Accessed: 20 July 2026).

- European Parliamentary Research Service (2025) “Space 2050: Scenarios for the European Union”. Available at: https://www.europarl.europa.eu/RegData/etudes/IDAN/2025/765792/EPRS_IDA(2025)765792_EN.pdf (Accessed: 20 July 2026).