Reports & Papers

Introduction

Economic diplomacy has long been integral to the implementation of U.S. foreign policy goals. From deploying development aid and establishing multilateral institutions that facilitate global commerce, to levying economic sanctions and erecting trade barriers, U.S. policymakers have wielded various carrots and sticks to promote national objectives.

Today, economic diplomacy has taken on a more complex and vital character. The Trump Administration has made it central to its foreign policy, using coercive economic tools to gain concessions on a wide range of policy issues. Since taking office, the Administration has added over 3,000 people and entities to the sanctions list, a marked increase from predecessors. It has placed export restrictions on Huawei, ZTE, and various Chinese supercomputing firms. It has also imposed worldwide tariffs on steel and aluminum imports, in addition to engaging in a trade war with China.

At the same time, more nations have gained the capacity to project economic power, and the interconnectedness of the global economy has created new economic pressure points for the U.S. Whereas the U.S. once enjoyed economic hegemony, China can now respond with its own set of tariffs, deploy foreign investment that surpasses what the U.S. has to offer, and establish rival multilateral institutions. Where U.S. sanctions were once a death sentence, the European Union and others have begun to explore alternate arrangements to circumvent U.S. oversight. With the integration of supply chains and the global flow of capital and talent, the U.S. must weigh measures to protect critical domestic industries, against its longstanding commitment to open markets.

For the next Administration, developing a clear strategy for maintaining and projecting American economic power will be critical. At the Belfer Center’s Economic Diplomacy Initiative, we define three key objectives for a U.S. economic diplomacy strategy. Against each of these objectives, our students have identified a range of pressing issues that the next Administration must address. The objectives and associated issues are:

- Promoting U.S. competitiveness in critical economic sectors, including protecting America’s leadership in AI, building U.S. competitiveness in 5G, evaluating the track record of the Committee of Foreign Investment in the U.S. (CFIUS), and defining federal data privacy regulation.

- Setting a clear vision for the international economic order, including maintaining the dominance of the U.S. dollar as the global reserve currency, updating the governance of multilateral institutions like the World Trade Organization (WTO), and countering China’s economic diplomacy strategies in the Indo-Pacific.

- Demonstrating American leadership in addressing transnational challenges, including deploying economic aid to address the migration challenge and developing a global health security strategy.

The nine issue papers contained in this report were proposed and written by graduate students at the Belfer Center for Science and International Affairs at Harvard Kennedy School. They present fact-based, nonpartisan analysis to help focus the next Administration on the key policy debates that must be resolved. And, they aim to create a platform for our students to engage with the most pressing policy issues of the day as they continue their careers in public service.

—Aditi Kumar, Executive Director, Belfer Center

1. Maintaining American AI leadership

Bo Julie Crowley

Issue Overview

As Artificial Intelligence (AI) drives relentless operational efficiency in the public and private spheres, it creates new economic winners and losers, introduces security opportunities and risks, and generates public concern about the safe and ethical use of technology. AI refers to computer systems capable of perceiving their environment and making decisions, such as processing a complex set of data and predicting outcomes or taking an action in response. Machine learning (ML) is often used interchangeably with AI, but is a subfield of AI that enables a computer to learn and improve on its own without being explicitly programmed for a particular outcome.

Recent breakthroughs in ML have enabled AI researchers to surpass human records in specialized skillsets, like chess and poker, and to mirror human linguistics and behavior with software. Combined with sensors and robotics, AI/ML solutions bridge the physical world with the virtual, leading to innovations like improved drone targeting and autonomous vehicles.

U.S. policymakers must maximize AI-powered economic opportunity while mitigating job replacement and inequality, establish international norms, address public concerns over the use of AI in warfare and surveillance, and navigate U.S.-China competition for global AI leadership.

Background

When AI is applied to a particular problem or task, the core components are algorithms and data. A learning algorithm allows the computer to identify patterns in a data set, build a predictive model, and make a decision without being pre-programmed for that exact scenario. AI can be broken down into four waves of development that are maturing at different rates:1

- Internet AI: algorithms that use internet behavior data (e.g., sites visited, products purchased) to build a user profile and tailor content (e.g., ads, suggested Netflix shows).

- Business AI: algorithms that use proprietary data (e.g., lifestyle and financial risk) to inform complex business processes (e.g., an applicant’s likelihood of repaying a loan).

- Perception AI: algorithms that process physical data (e.g., the number of eggs in the fridge, voice commands) to make decisions (e.g., to order more groceries, to play a song).

- Autonomous AI: algorithms that use data generated from multiple sensors (e.g., visual and audio feeds) to navigate the world on their own (e.g., in self-driving cars).

Despite continuous advancement, most sectors have not realized the majority of benefits from AI. The technology & communications, automotive, and financial service industries report the widest use of AI, but the adoption rate remains below one third across each industry. Large segments of manufacturing and retail remain offline; only 1% of cars sold in 2016 had basic autonomous capabilities, and only 10% of total sales in the U.S. and Western Europe occur online.2

Key Topics

AI represents enormous opportunity potential and is predicted to add $15+ trillion to the world economy by 2030.3 It also poses significant policy challenges around international competitiveness, worker displacement, the future of warfare, and data privacy. While this memo focuses on the economic and national security implications of AI, ethical issues, such as algorithmic bias, surveillance state AI tools, and artificial general intelligence (AGI) are also contested topics.

U.S.-China competition

The U.S. and China far outpace other regions of the world in AI research and application. Some experts believe the exponential pace of AI development creates a winner take all model where the most advanced country will concentrate insurmountable advantages. The McKinsey Global Institute estimates that leading countries will capture 20-25% of net economic benefits from AI.4

While the U.S. maintains an advantage in AI research over China, this lead is declining. The majority of AI conference researchers study in the U.S. (44% compared with 11% in China),5 but China recently surpassed the U.S. in number of annual AI research publications and patents.6 The U.S. maintains a lead in AI company valuations; American high-tech unicorns (startups valued above $1 billion) account for 40% of global high-tech unicorns compared to 14% within China.7 This gap will decrease, however, as Chinese AI companies rival their American peers in creativity and profitability and no longer depend on IP theft or copycat business models to drive growth. It is more difficult to compare financial investment in AI: U.S. figures account for direct investment in R&D while China also includes indirect investment, like construction costs for AI office parks and universities, in its investment totals. Chinese local governments, however, offer a range of AI investment and incentive programs, such as subsidies for AI companies, AI economic zones, and regulatory support for applications like autonomous vehicles. Nevertheless, global investment studies consistently report greater funding for U.S. AI startups, with U.S. venture capital and private equity firms investing over $16 billion in AI in 2017 compared to $13 billion in China.8

AI leadership will allow countries to concentrate economic gains and project foreign influence in unprecedented ways. China’s AI-enabled exports, like facial recognition software, mirror its Belt and Road infrastructure investments, with Chinese AI companies dominating parts of Southeast Asia, Africa, and Latin America. Analysts estimate that China exports AI-enabled surveillance technology to 50+ countries around the world.9 For example, Ecuador used part of a $250 million loan from China to purchase a statewide network of Chinese “smart” cameras and response centers.10

These private sector relationships establish new communication channels between China and foreign governments. They also advance Chinese norms around the use of AI to monitor domestic dissent, empower state surveillance, and restrict movement. For example, Megvii, one of China’s leading surveillance technology companies, provides facial recognition software to police departments across China. Independent reporting revealed that Megvii helped create software to identify Uighur muslims, a minority group interned in China’s northwest Xinjiang region. Last year, Megvii reported over 100% annual growth in international revenue and plans to open offices across Asia and the Middle East.11

Impact on jobs and wages

AI’s unintended consequences include worker displacement and growing inequality. AI’s net impact on overall employment may be low: McKinsey estimates that AI-driven job displacement could impact up to 25% of the U.S. workforce, but AI will create new opportunities to offset the majority of this loss. The study notes that technology has historically been a net job creator. At the same time, AI will transform the nature of work. An estimated 3% of the global workforce will need to change occupations by 2030, with physical, manual, and repetitive labor needs declining 30% and managerial, technological, and advanced analytics needs increasing 8% - 55%.12 AI is also not a silver bullet for the economy; U.S. productivity growth rates are predicted to decline from 2.5% annually in the 2000s to 2% annually in the next decade.13

More worryingly, studies show economic benefits from AI accrue to a small number of researchers and executives while median wages stagnate. Even within Silicon Valley, a 2017 study found that wages for 90% of workers (all workers excluding the top 10%) were lower in 2017 than 1997 after adjusting for inflation.14 Middle income workers in the 50th and 60th percentiles saw wages decline 14% after adjusting for inflation, despite the fact that per capita economic output increased 74% overall. In contrast, the top 10% enjoyed a wage increase. Without policy intervention, AI innovation and gains will be restricted to a small number of highly specialized individuals.

Impact on national security

Maintaining AI competitiveness is critical to the U.S.’s defense posture. The FY19 National Defense Authorization Act15 and DoD AI Strategy16 increased funding and support for defense AI applications and public-private sector partnerships to improve the Department of Defense’s capabilities. While AI has increased the accuracy, efficiency, and lethality of defense technology, there remains considerable opportunity to improve capabilities like intelligence collection and analysis, logistics, cyber operations, and autonomous vehicles.17 U.S. rivals are actively incorporating AI into military systems.18 China aims to become a global leader in AI by 2030 and is focused on using AI to improve national security decision making, while Russia is primarily focused on military use cases for AI and robotics. Barriers to AI adoption in national security include integration with legacy systems, maintaining interoperability with allies, applying commercially-trained AI to military environments with different conditions (e.g., poor map data), and obtaining the cloud computing power needed to run AI algorithms.

Although the DoD is not currently developing fully autonomous weapons systems, technology companies and civil society groups have opposed defense projects on ethical grounds that “killer robots” pose a threat to society. Regardless of DoD policy, AI and robotics technology is not advanced enough to deploy lethal robots that could pose an existential threat to society.

Data privacy

Data privacy regulation will directly impact AI research and competitiveness. Some studies suggest access to large quantities of training data is the greatest factor on AI development. U.S. states and the European Union have stricter privacy regimes than China, which may curtail U.S. companies’ access to training data. With over 750 million internet users (nearly three times as in the U.S.), China’s AI companies enjoy greater access to live consumer data. This advantage, however, may be overstated.19 While Chinese officials highlighted the country’s database of over 1 billion facial images, the FBI alone maintains a database of over 640 million facial images.20 U.S. companies like Microsoft and Alphabet are also investing in artificial training data, which may reduce China’s advantage in data access.

2. Competing in 5G

Raina Davis and Matthew Shackelford

Issue Overview

Fifth Generation (5G) wireless telecommunications networks will increase the bandwidth, capacity, and reliability of mobile communications. This latest evolution will provide critical support to a number of emerging technologies—including autonomous vehicles, augmented and virtual reality, remote healthcare, the internet of things (IoT)—that depend on reliable, low-latency,21 high-throughput22 connections to transfer large quantities of data. These networks have the potential to generate vast wealth and social benefits for the U.S., but also introduce certain risks.

Supply-chain integrations and technological challenges accentuate these risks. U.S. companies continue to dominate 5G component manufacturing, but the U.S. relies exclusively on foreign suppliers for telecommunications systems.23 The more interconnected and technologically-dependent U.S. infrastructure becomes, the greater its vulnerability to cyberattacks that cause physical, psychological, or financial harm. Two Chinese firms, Huawei and ZTE, dominate a substantial share of the 5G market. Reliance on their equipment generates national security concerns due to the firms’ close ties to the Chinese Communist Party (CCP) and legal obligation to comply with state intelligence requests. Several countries, including the U.S., have placed restrictions on the use of Huawei and ZTE equipment.

U.S. policymakers need to grapple with the opportunities and challenges that 5G presents to American consumers, businesses, and society. Engaging on a forward-thinking basis with 5G technology will drive American economic growth and prosperity in the coming decades, but important questions must be answered regarding the security and privacy threats posed by the incorporation of data and network technology into all aspects of daily life. As American businesses try to catch up with foreign competitors in technology development and deployment, innovative government policies can catalyze their growth and leadership. 5G calls for clear, well-developed, and values-driven leadership from policymakers to enable optimal outcomes for the U.S. and its citizens.

Background

Technological Developments

Since the first cellular network launched in the U.S. in 1982, a new generation of communications technology has entered the market each decade. The first generation (1G) supported basic speech; the second generation (2G) introduced digital transmission over the air, enabling mobile data use such as text and picture messaging; the third generation (3G) added data overlay capabilities such as GPS and video conferencing; and the fourth generation (4G) led to the transition from content download to wide-scale streaming. While most Americans today rely on recent 4G evolutions, 2G and 3G continue to be used in rural areas that lack 4G coverage.

5G will transform mobile networks through the integration of new technology and legacy equipment to support ultra-low latency and high-throughput connections. Unlike previous generations that utilize low-band radio frequencies, 5G networks will transmit and receive data across low-, medium-, and high-band radio frequencies.24 Broad-spectrum use will decrease wireless traffic congestion and increase perceived network speed. To compensate for the shorter transmission and lower penetration rates of medium- and high-band frequencies, 5G systems will relay data through a network of smaller, non-traditional deployments, such as small cells and micro-cells.25 These miniature and small cellular towers transmit short-range radio signals and will need to be deployed across cities on street lights, street signs, vehicles, and buildings.

The 3rd Generation Partnership Project (3GPP), a leading standard and regulatory body, divides future 5G demand into three categories based on radio-band frequency: Enhanced Mobile Broadband (eMBB) (low-band); Ultra-Reliable Low-Latency Communications (URLLC) (medium-band): and Massive Machine Type Communications (mMTC) (high-band). With download speeds up to 20x faster than current standards, eMBB supports data-driven applications over large areas, like augmented/virtual reality, as well as traditional mobile connectivity and broadband. Autonomous vehicles, smart grids, tactical feedback in remote medical procedures, and other time-sensitive applications that require high reliability will utilize URLLC (end-to-end latency of <5ms and uptime of 99.999%). mMTC will connect tens of billions of low-complexities, low-power devices in the IoT domain.

The 5G network in the U.S. launched in a limited capacity beginning in 2018,26 reaching over 30 U.S. cities as of July 2019,27 but widespread domestic availability faces technical and physical challenges that cannot currently be overcome by U.S. firms alone. Even as the U.S. expands its reliance on foreign equipment, China races to end its dependence on U.S. technology and has invested heavily to develop an end-to-end domestic supply chain.

The 5G Marketplace

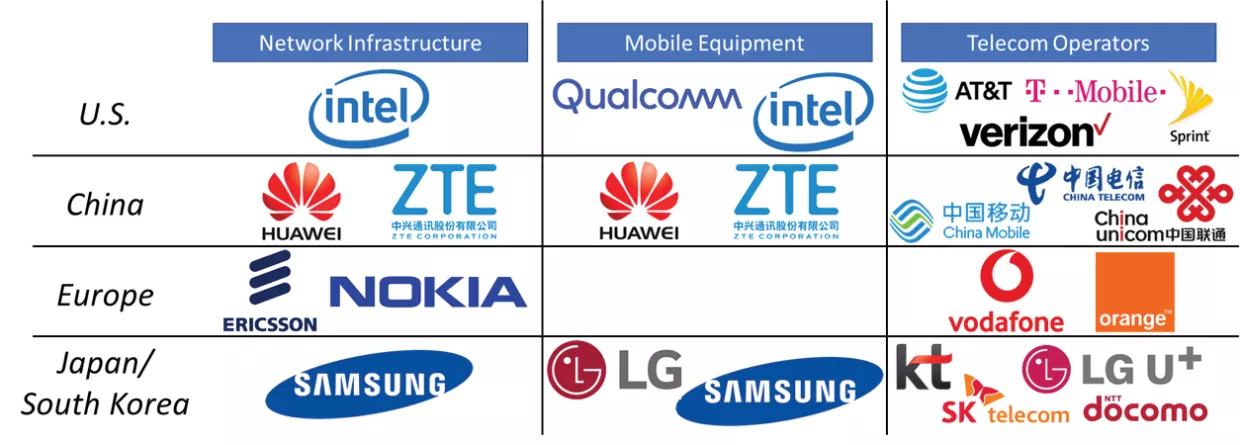

Important 5G companies can be divided into three functional categories: Network Infrastructure, Mobile Equipment, and Telecom Operators. Network Infrastructure companies focus on developing software or hardware solutions for the core or periphery of 5G networks. As an example, Intel is a leading provider of specialized software called Network Functions Virtualization (NFV) that enables the functionality of the network core, while Ericsson produces, among other things, the radio system that is deployed at the network periphery to communicate with mobile devices. Mobile Equipment companies produce 5G mobile phones or modems for 5G-enabled devices. Finally, the Telecom Operators are the firms that manage cellular networks.

Companies in all three verticals interact with each other regularly. Network Infrastructure firms need to ensure that their technology can communicate with the phones and modems being produced by the Mobile Equipment companies, and vice versa. Telecom Operators enter into contracts with Network Infrastructure firms to upgrade their networks to 5G and agree to sell the devices of Mobile Equipment companies for use on their networks.

Federal Legal & Regulatory Structure

The rollout of 5G in the U.S. and around the world will be gradual and incremental.

Systems and devices already operating on current networks, such as smartphones and infrastructure, will begin using 5G far quicker than those that require wide spectrum availability. Most devices will continue to utilize 4G, a hybrid of 4G/5G infrastructure, or Non-Stand-Alone (NSA) 5G Networks.28 Stand-Alone (SA) 5G Networks are projected for rollout in 202029 and widespread adoption in 2022.30 Their deployment requires the finalization of 5G standards by international regulatory bodies, like the 3GPP and the International Telecommunications Union (ITU), and the release of broader spectrum by the FCC.31

U.S. 5G regulation is driven by the Department of Commerce, Department of Homeland Security, and Federal Communications Commission (FCC). The Department of Commerce works closely with industry stakeholders and international partners to develop 5G standards, promote innovation and competitiveness, and manage export controls and treaty compliance.32 The Federal Communications Commission (FCC) leads federal regulation of telecommunications technology and manages commercial spectrum use. Under its 5G FAST Plan, the FCC plans to auction 6,000 licenses for underutilized high-band spectrum (28-24 GHz) to communications companies. Finally, the Department of Homeland Security leads the federal government’s 5G resilience and security efforts.

Security concerns have driven additional 5G-specific and communications supply chain regulations. The Federal Acquisition Supply Chain Security Act (FASCA) of 2018 (P.L. 115-390) established the interagency Federal Acquisition Security Council to mitigate, via “removal orders” and “exclusion orders,” supply chain risk in federal information and communications technology (ICT) acquisition, including 5G. The 2018 National Defense Authorization Act (NDAA) prohibited federal agencies and contractors from purchasing or using certain telecommunications and surveillance products from Huawei, ZTE, and Chinese surveillance-equipment makers. Section 889 of the 2019 NDAA reiterated this ban.

Key Topics

5G Security

Director Christopher Krebs of DHS’s Cybersecurity and Infrastructure Security Agency (CISA) categorizes the risks associated with U.S. 5G deployment as technical, physical, and logistical related vulnerabilities.33 On the technical side, the current 5G rollout is overlaid on existing 4GLTE networks, making the network vulnerable to legacy exploits that previously enabled eavesdropping, location tracking, device fraud, or denial of service attacks.34 As with any new technology, initial 5G equipment and protocols will likely contain exploitable backdoors, which will increase in consequence as 5G takes on mission-critical functions.

On the physical side, 5G expands the potential attack surface area of mobile infrastructure. The ubiquity of small cell sites will make the physical security of telecom hardware nearly impossible. However, such entry points are unlikely to provide widespread network access or allow for substantial data extraction.35

Finally, 5G represents a significant shift from hardware to software-based telecom, giving more power to vendors. As with cellphones and computers, future telecom technology will maintain connection to manufacturers long after sale and require frequent software updates, which malicious actors could use to create backdoors or disrupt service.36 Working with trusted companies and a diversity of vendors can help mitigate this risk.

The Huawei, ZTE Threat

Two Chinese telecom companies, Huawei and ZTE, have been at the center of the 5G policy and security debate. Accusations of economic espionage and theft of trade secrets culminated in a Department of Justice (DOJ) indictment against Huawei in January 2018.37 Concerns that Chinese telecom equipment will be exploited by Beijing for espionage, surveillance, or cyber-attacks, prompted many Western governments, including the U.S., to restrict or altogether ban Huawei equipment.38 Lawsuits filed by the targeted corporations and an international lobbying campaign to portray Huawei as the only technologically viable 5G provider39 have muddled the debate. How should governments assess the threat that Huawei and ZTE pose to 5G infrastructure security?

China has long pursued a strategy of cyber-enabled economic espionage and cross-border intellectual property theft to bypass lengthy and expensive R&D and strengthen its economic competitiveness, often to the private benefit of party leaders or PLA units. Chinese cyber espionage rose to unprecedented levels as part of President Xi’s larger military modernization effort.40 The 2019 Worldwide Threat Assessment of the U.S. Intelligence Community warned that “China presents a persistent cyber espionage threat and a growing attack threat to our core military and critical infrastructure systems.” In addition, former Director of National Intelligence Dan Coats voiced “concern that Chinese intelligence and security services [may] use Chinese information technology firms as routine and systematic espionage platforms against the United States and allies.” This warning echoed the findings of the 2012 House Permanent Select Committee on Intelligence’s study on Huawei and ZTE, which concluded that China has the “means, opportunity, and motive to use telecommunications companies for malicious purposes,” and supply-chain risks in our critical infrastructure from the use of Chinese telecom technology cannot be addressed by “mitigation measures” alone.41

Chinese telecom technology had often been used to pursue state objectives. In 2018, investigative journalists working forLe Monde identified unusual traffic leaving the African Union headquarters following the donation of a Huawei telecom system.42 Huawei denies any complicity, and Ren Zhengfei, CEO and founder of Huawei, has vowed to deny any request from the Chinese government to access user data.43

Indeed, there is no “smoking gun” indicating that Chinese telecom companies have willingly given access or data to the government. Proven vulnerabilities in Huawei equipment44 have been subsequently identified in a number of non-Chinese products, including from Cisco, Sony, and D-Link. Global 5G competition pressured companies to produce quickly, and it is difficult to ascertain if bugs in Huawei code are deliberate vulnerabilities or accidental mistakes.

Under China’s 2017 National Intelligence Law, which compels all Chinese companies to comply with Ministry of State Security requests, Huawei and other telecom companies can now be forced to assist the government in surveillance and espionage. As James Andrew Lewis, CSIS Senior Vice President, testified before Congress, “The issue is not whether one trusts the Chinese company, but whether one trusts the Chinese government.”45

Other concerns related to Chinese telecoms include network hijacking and surveillance.

China has sufficient penetration into the Internet backbone to redirect or disrupt global traffic. In 2010, Chinese telecoms took over 15% of internet traffic for 18 minutes. 46 Domestically, China has doubled down on surveillance, deploying AI-enabled facial recognition technologies run on 5G networks to track individuals and identify ethnic minorities.47 Huawei and ZTE are actively exporting these “smart city” surveillance systems to repressive regimes, including Mongolia, Ethiopia, Zimbabwe, Malaysia, and Ecuador.48

Making U.S. Firms Competitive

To compete globally in an effective manner, U.S. companies need to overcome three key obstacles that currently prevent them from doing so. The first is the successful vertical integration of their 5G offering. Currently, no U.S. firm offers an end-to-end solution for telecom operators who seek to build a 5G network, while Huawei does,49 making it difficult for U.S. firms to compete effectively. Second, U.S. firms are being out-competed on price. Firms from other nations, particularly Huawei, are undercutting the prices charged by U.S. companies by up to 30%, principally driven by manufacturing advantages for non-U.S. firms and alleged state subsidization for Chinese firms.50 The third obstacle is the technological advantage possessed by non-U.S. firms in some specific 5G technologies. Experts believe that U.S. firms are 18-24 months behind competitors in the research of and rollout capacity for particular technologies,51 preventing U.S. companies from playing a larger role in the global 5G market.

To support American growth and increase U.S. competitiveness, U.S. policymakers should implement two broad sets of actions: fostering actions to bolster U.S. businesses to compete in the 5G market and diminishment actions against foreign firms focused on leveling the playing field for U.S. companies. 5G supply chain integration creates challenges in pursuing a wholesale “decoupling” of U.S. firms from international markets, yet policymakers can strengthen U.S. firms and selectively work with U.S. allies to diminish the role of strategic adversaries. By focusing on overcoming the potential dominance of strategic adversaries, the U.S. could attain leadership in some 5G technology facets while maintaining a competitive edge in others.

3. Evaluating the Track Record of CFIUS

Allison Lazarus and Raina Davis

Issue Overview

The Committee on Foreign Investment in the United States (CFIUS) has largely kept a low profile over its 44-year history. CFIUS is an interagency committee charged with reviewing the national security implications of foreign investments in U.S. companies and was originally established in response to concerns about foreign direct investment by Organization of the Petroleum Exporting Countries (OPEC) in American portfolio assets in the 1970s. However, in recent years, the committee’s activities have become newly visible to the American public amid concerns about growing Chinese investment in American companies, particularly in the technology sector.

This influx of Chinese investment revived interest in CFIUS and led, in the summer of 2018, to the bipartisan passage of the Foreign Investment Risk Review Modernization Act (FIRRMA). FIRRMA expanded CFIUS’s jurisdiction to include a broader range of transactions, including joint ventures, and doubled the list of national security factors for CFIUS to consider in its risk reviews. However, further reform may be necessary to ensure that CFIUS is able to successfully meet its objectives. Current criticisms of CFIUS range from allegations of unfair targeting of Chinese investment and perversion of American free market principles to concerns that there are still too many loopholes for problematic foreign investment.

Background

CFIUS is chaired by the Secretary of the Treasury, and includes voting members from the Departments of Commerce, Defense, Homeland Security, Justice, State, and Energy, with several additional non-voting members. The establishing language called for the committee to have responsibility for “monitoring the impact of foreign investment in the United States,” and for “coordinating the implementation of U.S. policy on such investment.”52 In its original iteration, CFIUS existed only to study foreign investment, but by 1988, fear of Japanese investment, particularly in the semiconductor industry, led Congress to pass the Exon-Florio Amendment, which allowed CFIUS to reject deals. The committee did not have a formal statutory basis until 2007, with the passage of the Foreign Investment and National Security Act (FINSA), which also provided a broader oversight role for Congress but left the President as the only officer with the authority to suspend or prohibit actions under CFIUS.

The committee’s jurisdiction over ‘national security’ effects is wide: it can review any “covered transactions,” which are defined as mergers, acquisitions, and takeovers by or with a foreign entity that could result in foreign “control” of a U.S. business.53 However, it generally focuses on transactions for which there is some fear that the technology involved might be transferred abroad inappropriately, especially related to critical infrastructure and defense. Companies involved in an acquisition by a foreign firm are required to notify CFIUS, but the committee can also review transactions of its own accord. CFIUS does not publicize which deals are under review, involve parties directly, or publicly announce its findings.

The committee’s process is fairly simple. The reviews begin with a 30-day period to authorize a transaction or begin an investigation. CFIUS considers 10 specific factors when analyzing the national security implications of a transaction (e.g., domestic production needed for projected national defense requirements, capability and capacity of domestic industries to meet national defense requirements). If it pursues an investigation, it has a 45-day decision period to either permit the acquisition or order divestment. This is potentially followed by a 15-day period for presidential review if CFIUS refers a transaction to the President for a decision. Most transactions are approved without a statutory investigation – in 2015, only 46% of the cases that had been noticed were investigated.54 If CFIUS finds that a covered transaction poses national security risks, it can impose certain conditions before allowing the deal to proceed, including a mitigation agreement to address these risks. Some parties opt to withdraw the deal rather than executing a mitigation plan or waiting for referral to the President.

However straightforward these guidelines, their application has varied significantly over recent decades. While largely inactive in earlier years, the committee’s investigations increased beginning in 2008 and continuing until today.55 High profile recent cases have included the 2012 ordered divestment of wind farm projects in Oregon by a Chinese company, the 2016 blockage of acquisitions by a Chinese company interested in gallium nitride, the 2017 blockage of a Chinese buyer for Lattice Semiconductor, the 2018 blockage of a Singaporean company from purchasing Qualcomm, and the 2019 requirement for divestment from Grindr by a Chinese company.56 To date, only five transactions have been formally blocked through this process, though this number certainly understates CFIUS’s true impact as many other transactions under investigation have been subject to stringent mitigation actions or withdrawn by the firms (who anticipate them being blocked if allowed to proceed).

In recent years, CFIUS has focused primarily on investment from China. Chinese investment in U.S. companies has quickly grown, tripling from 2015 to 2016 at a peak of $46 billion.57 Though there has been a recent fall-off in the level of investment given the Trump administration’s trade policies, policymakers remain concerned that some of this investment may, though conducted by private firms, be centrally directed toward acquiring early-stage U.S. technology with potential military applications. This concern is reinforced by public Chinese documents, such as the “Made in China 2025” plan, which includes measures to provide domestic Chinese companies with preferential access to capital to support acquisition of technology from overseas.58 These fears have been bipartisan, with the Obama White House publicly questioning Chinese investment in semiconductors, and the Trump administration doubling down on this skepticism. From 2016-2017, a full 20% of CFIUS’s cases were related to Chinese investment.59

In 2018, Congress passed FIRRMA, a reform to CFIUS, on a bipartisan basis. This Act gave CFIUS new powers over particular types of FDI, including real estate investing, minority investments, and joint ventures.60 FIRRMA targeted these areas because they were widely perceived as gaps in CFIUS’s authorities exploited by Chinese firms. The committee also gained more resources, the authority to lengthen review periods, and to request widened disclosure from involved parties. The rhetoric surrounding FIRRMA’s passage was explicitly tied to concerns about Chinese investment. Though FIRRMA reformed CFIUS, it did not fundamentally change the committee’s structure and did not impose a categorical ban on any type of foreign investment, potentially reflecting the ongoing consensus on FDI’s value except in specific situations of concern.

Key Topics

Is CFIUS effectively balancing economic competitiveness and national security?

Historically, the U.S. has been intent on establishing an open and rules-based international economic system. This approach has maintained that, except in exceptional cases, FDI has positive net benefits for the U.S. and the global economy. CFIUS represents that small group of cases where this prevailing viewpoint is challenged. The Committee must balance, on the one hand, the maintenance of an open and efficient investment climate where U.S. firms are competitive, and on the other, the appropriate protection of U.S. technology and other critical industries from foreign theft or injury.

There is limited evidence that CFIUS enforcement has hurt U.S. business on a macro scale. The global FDI position of the United States, or the cumulative amount of inward foreign direct investment, was recorded at around $7.8 trillion in 2017, with the U.S. outward FDI position of about $7.9 trillion.61 This is on par with recent years, despite an uptick in CFIUS activity beginning in the same period. However, CFIUS seems to have had an impact on the inflow of Chinese capital. Chinese investment in the tech sector dropped from $18.7 billion across 107 deals in 2016, to $2.2 billion across 80 deals in 2018.62 The numbers suggest that Chinese investors may be pursuing smaller deals in order to avoid CFIUS scrutiny.

FIRRMA also newly allowed for investors’ nationalities to be considered directly during the review, which will further target CFIUS’s attention on the highest perceived national security risks. Ultimately, the limited volume of cases investigated by CFIUS are unlikely to harm U.S. economic competitiveness overall, although the impact on specific sectors may be more significant. At an individual company level, however, the CFIUS process can create an “overhang” that negatively affects a firm’s valuation and ability to access funding. If the scale of CFIUS activity were to increase substantially, these concerns might become more important for the evaluation of the committee’s work.

Proponents and critics disagree on CFIUS’s efficacy in addressing national security concerns. On one hand, by blocking investments into critical infrastructure and companies like Grindr that hold sensitive information on U.S. customers, CFIUS has protected key American assets. There is some evidence that CFIUS’s greatest impact may be occurring outside of the formal process: the committee’s most recent public report indicated that CFIUS applied mitigation measures to 47 cases in the 2016-2017 period.63

However, criticisms range from whether the process is unfairly targeting Chinese investors to a lax enforcement regime (e.g., 89% of the investment transactions notified to CFIUS from 2008 to 2015 ultimately took place).64 For example, the voluntary disclosure that begins the process is nominally checked by CFIUS through a review of ongoing deals that might not have been reported. But, it is likely that, even with a well-intentioned, hard-working staff, the committee is not resourced appropriately to follow up on all investment flows into the United States. Often, foreign investors enter the U.S. market through complex investment structures, such as pooled investment funds managed by U.S. private equity firms, and detecting this activity would require a full investigative capability that the committee does not currently have.

If we conclude that CFIUS does not harm the economic situation of the U.S., but may be missing genuine security threats, there are several potential remedies. CFIUS could be modified to include a mandatory approval process for some transactions or to act as part of a larger industrial policy which actively protects and promotes certain target industries. Solutions nearer to the minimal end of this spectrum may be best positioned to ensure that the committee does not end up inadvertently harming broader foreign investment.

Is CFIUS structured in the right way to be effective?

Even if there is agreement on the balance between CFIUS’ objectives, the committee’s structure still influences whether it is able to achieve them. Would-be reformers of CFIUS might choose to focus on potential areas for improvement where the committee’s structure currently stops it from being most effective.

The first of these areas is resourcing. Though FIRRMA designated more resources for the committee (including the piloting of a fee-financing structure) and added positions at Treasury focusing specifically on this issue (e.g., Assistant Secretary for Investment Security), CFIUS must be resourced appropriately for the duties that it is assigned. Current voluntary reporting as the main source of information for the committee on ongoing deals means that it may miss deals of real concern, so the committee may need to invest in a more robust investigative capacity. Moreover, understanding which technologies may have national security implications for the U.S. requires deep functional expertise which the committee may not currently be resourced to provide. Finally, FINSA authorized CFIUS to evaluate the compliance of firms that have entered into a mitigation agreement – another duty that is critical to the committee’s success as an institution but likely to require significant manpower.

Another area of potential reform is specialization. CFIUS does not affect all industries equally: 43% of foreign investment transactions notified to CFIUS from 2008 to 2015 were in the manufacturing sector (especially within computer and electronic parts).65 Investments in the finance, information, and services sectors accounted for another 31% of the total notified transactions. However, the committee is ostensibly structured to be equally applicable across industries. Future reformers might consider specializing CFIUS in such a way as to be capable of operating across sectors but more knowledgeable about those few which will make up the vast majority of its work.

Finally, CFIUS might be more effectively structured for its interaction with the companies and investors that it investigates. Much of the committee’s work with them (e.g., informal discussions, creation of mitigation plans) was not envisioned when the statute was drafted. Mitigation agreements can include steps like ensuring only authorized persons have access to technology, establishing a Corporate Security Committee, establishing governance structures, particularly if investors must give up Board seats or other decision-making authority during the course of the investigation, or other security protocols. These agreements, despite their broad nature, often have little basis in statute and have not been tested in court. Therefore, going forward, it would be helpful both for private investors and the committee to better understand the bounds of these mitigation agreements and the potential actions that can be included within them. Such reforms might also help to mitigate past criticism that CFIUS’s process can feel like a black box subject to politicization.

Ultimately, these areas represent some potential reforms that could enable CFIUS to function more effectively, but the real work for a future administration will be in determining their ideological stance on weighing national security concerns against broader economic interests. The committee should then be structured to support this consensus.

4. Developing Data Privacy Regulation

Angela Winegar

Issue Overview

Large data breaches at Equifax, CapitalOne, Facebook, and a host of other companies have ignited a policy debate about data privacy and security. These incidents highlight the significant risk to consumers of allowing online social media providers, data brokers, and others to collect their personal data. First, consumers may not have given proper consent for personal data to be collected, signing complex terms and conditions of free services without a thorough understanding of their contents. Second, consumers may know their data is being collected, but the data may be stored in a way that is sub-optimal and susceptible to hacks by bad actors, as in the case of the Equifax breach. Third, as the Cambridge Analytica scandal illustrated, companies may intentionally use consumer data in inappropriate ways, in this case to influence votes in the 2016 election.

While consumer data protections have already been proposed or enacted in China and the European Union, and various U.S. states have proposed their own versions, U.S. policymakers have yet to outline a national data privacy policy. In addition to the benefits of consumer protection, these policies must weigh a number of risks. First, regulation should consider how data privacy policy will impact tech business models, and thus impact access to services and cost to consumers. Facebook, Google, LinkedIn and other tech giants offer free services to consumers because of their ability to profit from targeted advertising. Eliminating this opportunity could threaten the free nature of many products and services, disadvantaging the lowest income consumers, as well as potentially harm innovation by smaller tech players.

Second, data privacy regulation will have direct impacts on the development of the U.S. tech industry, and particularly the artificial intelligence (AI) sector. Many AI and ML solutions require consumer data to train the algorithm, and how a data privacy policy mandates data collection, usage, and storage of this consumer data will have massive implications for the industry. Thus, the specifics of any national consumer data regulation must balance consumer protection while still encouraging key types of technological innovation.66

Background

While the U.S. has yet to develop a national consumer data privacy policy, similar policies have been proposed or adopted by foreign jurisdictions, notably the E.U.’s General Data Protection Regulation (GDPR); by U.S. states, notably the California Consumer Privacy Act (CCPA); and within specific economic sector like the Health Insurance Portability and Accountability Act (HIPAA) and the Family Educational Rights and Privacy Act (FERPA).

GDPR was passed in the E.U. in 2016 and went into effect in 2018. It is applicable to any company processing the personal data of individuals residing in the E.U., regardless of the company’s physical location. GDPR enables the E.U. to fine companies the greater of €20 million or up to 4% of annual global revenue should the company not meet GDPR’s robust data standards. GDPR also includes a number of consumer-friendly stipulations, including: no longer allowing companies to use long, indiscernible terms and conditions; requiring users to give consent before their data can be used by advertisers (effectively pursuing an opt-in model); requiring ease for withdrawal of that consent; requiring mandatory breach notifications; protecting the right of consumers to access their data in a commonly used, machine-readable format with understanding of why it is being processed; and mandating the right to delete data (the right to be forgotten), among others.67

Just one month after GDPR went into effect, the California State Legislature, led by Governor Jerry Brown, signed the California Consumer Privacy Act (CCPA), which went into effect on January 1, 2020. CCPA is similar to GDPR for California residents, with a few key distinctions. It only applies to certain companies, based on revenue, data type, and how revenue is generated, and has a broader definition of “personal information”, extending to households what GDPR classifies as individual-only. CCPA also includes: the right for consumers to know what personal information a business has collected, where it was sourced from, and what it is being used for; the right to opt out of allowing a business to sell their personal information to third parties; the right to delete personal data used by companies; and the right to receive equal service and pricing from a business.68

Following passage of the CCPA, Vermont passed its own data privacy legislation in December 2018, followed shortly by Maine and Nevada. Hawaii, North Dakota, New York, Texas, and others are currently considering similar measures. Big Tech companies have been lobbying the federal government for a national policy since the introduction of CCPA, to avoid implementing and managing adherence to fifty different policies.

Similar data protection policies have long been effective in specific sectors. In the healthcare sector, HIPAA outlines national standards for processing electronic healthcare transactions at the national level, as well as standards for how healthcare providers and insurers must treat confidential consumer data. Similarly, FERPA protects the privacy of student education records, by stipulating how schools and school districts must treat student data.

Currently, Congress is considering several bills to establish a federal data privacy policy. Bills range from those weaker in data privacy protection to proposals that are even stricter than CCPA, GDPR, and other similar policies. In the Senate, Marco Rubio has introduced the American Data Dissemination Act and Senator Marsha Blackburn has introduced the Balancing the Rights of Web Surfers Equally and Responsibly Act. Both were meant to pre-empt the implementation of the CCPA and offer less stringent protections; both have stalled in committee. In the House, Representative Suzan DelBene’s Information Transparency and Personal Data Control Act was also meant to pre-empt the implementation of CCPA while offering slightly more protections than the two Senate bills. On the stricter end, Senator Catherine Cortez Masto introduced the DATA Privacy Act which is very similar to CCPA and GDPR, while Senator Ed Markey’s Privacy Bill of Rights Act goes even further in protecting consumer privacy and punishing violations by tech companies, including the provision that consumers are able to sue. To date, none of these bills look likely to pass, paving the way for a fragmented patchwork of state-level regulations.

Key Topics

Any national data privacy policy will need to weigh the tradeoffs between consumer protection and impacts to economic development, specifically the future of America’s AI industry.

Consumer protection

From a consumer protection standpoint, a data privacy policy will need to address obvious concerns about consumer harm: for example, because Equifax didn’t take the necessary precautions in storing consumer data, roughly half of all American’s social security numbers were leaked. Similarly, the Cambridge Analytica scandal demonstrated how users’ personal data could be used without their consent or knowledge for political advertising.

Perhaps less intuitively, data protection is also about reducing different forms of consumer bias, for example, preventing companies from deciding who sees a job advertisement based on race, religion, gender, income, or other factors, or colleges from collecting enough data to identify and admit the likely highest income earners to maximize their endowments. This is particularly relevant when consumer data is an input to machine learning algorithms, which is increasingly the case. A clear data privacy policy must not only protect consumers from theft and misuse of their data, but also from discriminatory practices and biased algorithms.

U.S. competitiveness

Moreover, data privacy policy proposals must also consider impacts on the U.S. tech industry. For example, the introduction of GDPR necessitated changes to business models, particularly in the digital marketing sector.69 Global advisory firm Ernst & Young estimated that Fortune 500 companies spent $7.8 billion70 simply to comply with GDPR before the law took effect, in addition to the ongoing costs of compliance. While larger firms may have the resources to comply with this, many small businesses have been unable to compete and simply ceased operations in Europe71. If the U.S. were to implement a similar policy, one potential risk is disproportionate impacts on small businesses that are unable to manage compliance costs, with the effect of reducing overall competition.

In addition, proposed data privacy policies must evaluate the impact on AI development in the United States. AI is expected to add over $15 trillion to the world economy by 203072, with gains anticipated to accrue disproportionately to leading U.S. firms. A data privacy policy that hampers data use in the AI sector could risk U.S. competitiveness, particularly relative to Chinese developers. Some recent studies find that the E.U.’s lack of competitiveness in the AI sector can be attributed, in part, to GDPR,73,74 specifically because AI development requires exceptionally large datasets. GDPR prohibits use of certain consumer data in these datasets, or requires the structuring of it in a certain way (to allow for right to delete, etc.) limiting the ways in which private companies can leverage these datasets to create AI and machine-learning algorithms. By contrast, it is believed that China leads in the facial recognition field because of its large population and limited privacy requirements, allowing both government and private sector to leverage data, such as camera footage, to develop these algorithms.75 As such, it is important to collaborate with the private sector and those developing AI-related products to ensure a data privacy policy does not hamper economic competitiveness in this space.

In conclusion, data privacy policies must carefully consider the long-term repercussions on consumer protection and economic competitiveness.

5. Protecting U.S. Dollar Dominance

John Michael Cassetta

Issue overview

Since the end of the Second World War, the U.S. has been the system operator of the international financial system. The world uses the U.S. dollar (USD) and dollar-backed assets as a de facto reserve currency, and the U.S. financial system is central to global commerce.

This position endows the U.S. with unique power and responsibility in at least three critical areas: (1) a position of leadership in the global coordination of economic policies, such as among G7/G20 nations, (2) the ability to sanction and therefore influence any state engaged in dollar-based global commerce, and (3) the paradoxical effect that, because USD securities such as U.S. government debt are “safe harbor” assets, the USD and U.S. government debt strengthen in global economic crises, even those originating at home.

A strong dollar, buoyed by global demand, also presents challenges. In supplying the world with sufficient dollar liquidity, the U.S. runs a large trade deficit: it imports goods and exports dollars. Because world demand for dollars is strong, the dollar is often overvalued relative to other currencies, inflating the cost of U.S. exports and harming American exporters (although some argue a weaker dollar could indirectly do greater harm to the U.S. economy by slowing the global economy). Foreign countries and companies reinvest dollar savings earned from exports to the U.S. back into the U.S. economy. China alone holds 4.6% of U.S. government debt, for example, and accounts for 15.7% of foreign holdings of U.S. government debt.76

When put to productive use, this “easy credit” allows the U.S. to finance spending cheaper than other countries; when put to unproductive use, this credit can fuel bubbles such as in the subprime mortgage market that triggered the Great Financial Crisis. Cognizant of the power the dollar-based system gives the U.S. over their economies, China and Russia, but also the E.U., are exploring alternative non-dollar systems, though with limited success to date.

The current debates focus on the tension between the U.S. using its advantage to prioritize unilateral aims. This tension plays out in three major policy areas:

- How aggressively should the U.S. use secondary sanctions to achieve foreign policy goals, and should it do so unilaterally?

- How seriously should the U.S. be concerned about attempts by other states to create non-dollar systems? How should it respond?

- Should the U.S. devalue the dollar to support exporters and American jobs, or will a weaker dollar harm the global economy in a way that ultimately harms the U.S.?

Background

America emerged from WWII as the leader of the international economic system. In what came to be known as the Bretton Woods system, the victorious nations agreed to fix world currencies to the U.S. dollar, which would be backed by and redeemable in gold at $35 per ounce (i.e., the gold standard).77

While in the 1950s and early 1960s the U.S. became a major exporter to foreign countries, especially Europe flush with aid from the Marshall Plan, by the late 60s the trend reversed as war-ravaged economies grew and began exporting to the U.S. The U.S. ran a trade deficit, importing goods and exporting dollars to the world. To finance government expenditures, especially the Vietnam War and President Johnson’s Great Society programs, the U.S. increased the supply of dollars. As a result, the global supply of dollars (claims on U.S. gold deposits) held by foreigners grew beyond the gold reserves of the U.S.78

Then, two developments shaped the modern monetary system. In August 1971, in the face of downward market pressure on an overvalued dollar and threats from foreign countries to redeem their dollars for gold, President Nixon took the U.S. off the gold standard. Despite attempts to set new fixed exchange rates, notably in the 1971 Smithsonian Agreement, market pressure forced another dollar devaluation. G-10 countries agreed to allow European Community currencies to float against the dollar, and eventually most world currencies, rather than being fixed to the dollar, would float with market forces.79

Second, a wave of “balance of payment crises” swept the developing world in the 1980s and 90s, convincing central banks to hold significantly more dollars reserves. The Asian Financial Crisis of 1997-8, for example, occurred when Asian countries who had pegged their currencies to the dollar and borrowed heavily from foreign creditors faced sharply rising borrowing rates as creditors grew doubtful about their ability to repay. Lacking a stockpile of dollars to defend their currencies, countries such as Thailand devalued their currencies, stifling imports and domestic growth, while spreading a global economic contagion.80

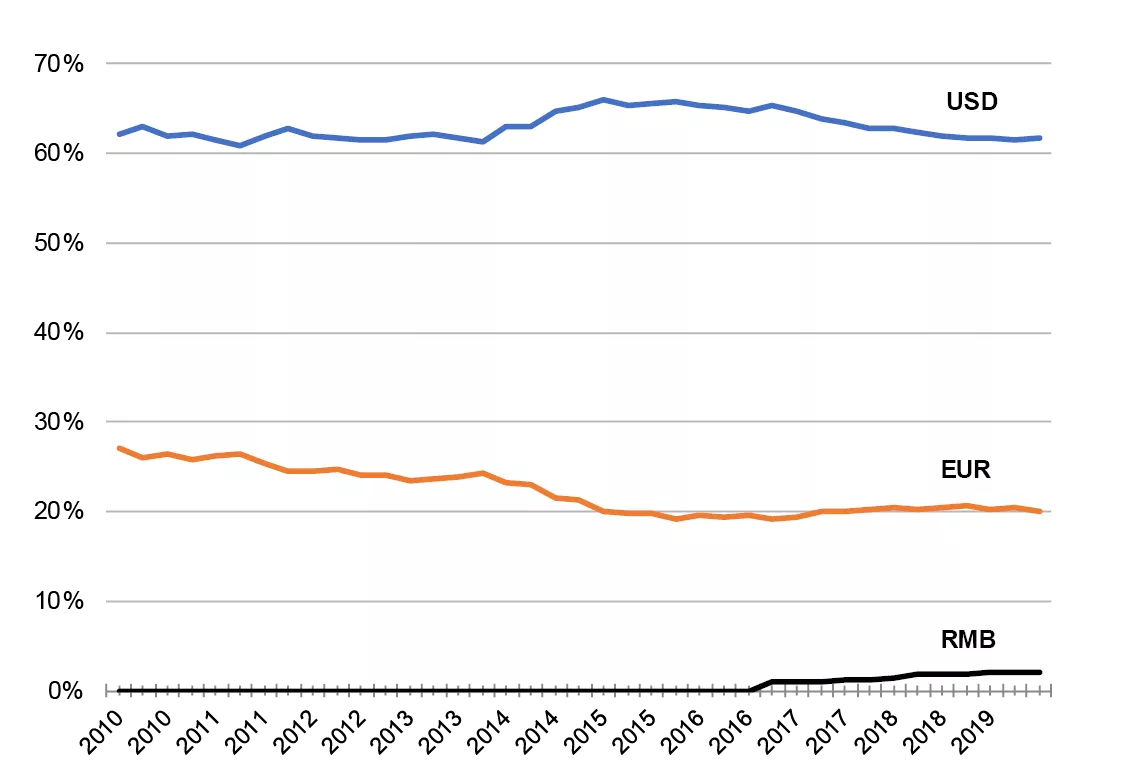

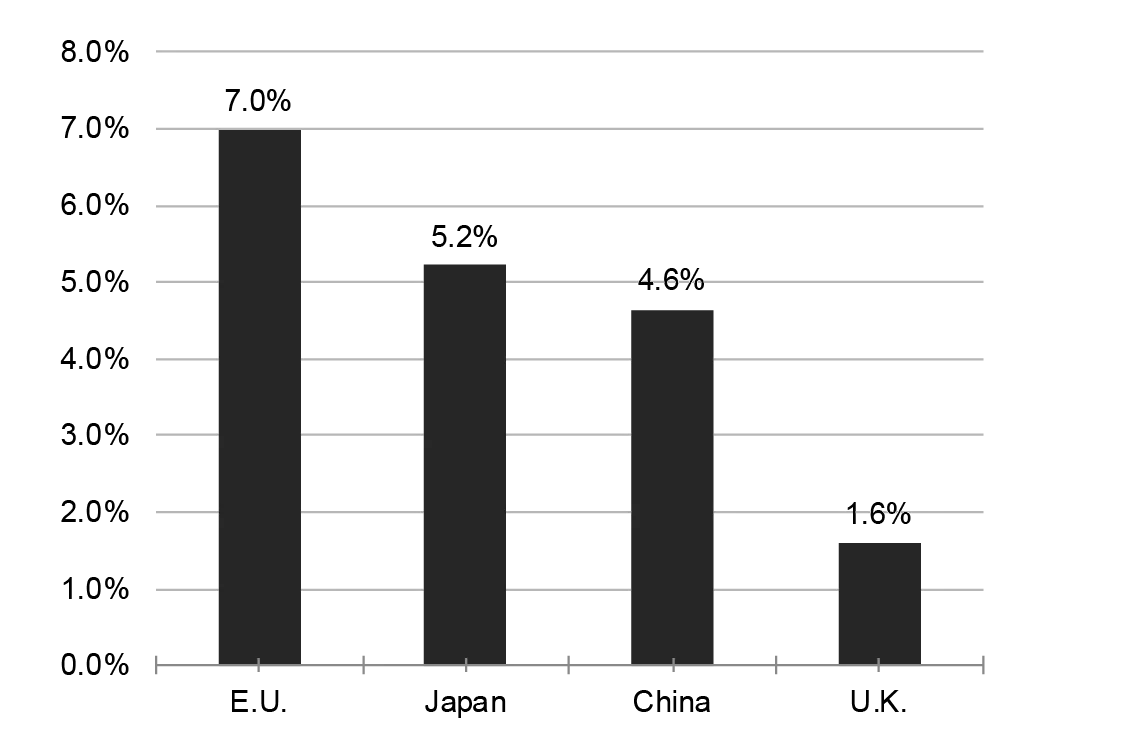

Today, the dollar represents 88% of global currency transactions.81 Much of world trade is conducted in USD, particularly trade in commodities such as oil, even by adversaries of the U.S. To guard against such crises, many central banks now hold significantly greater foreign exchange holdings, 62% of which are in dollars (Figure 1).82 To earn interest on their dollars, foreigners invest dollars in dollar assets, primarily U.S. Treasury bonds: 39% of U.S. government debt held by the public is held by foreigners, including China which holds 4.6%, or over $1 trillion. (See Figure 2.)83

Three major factors prop up the dollar’s popularity. First, the dollar is the preeminent medium of exchange. World trade is settled in dollars largely because the dollar is a liquid asset everyone can agree everyone else wants. As balance of payment crises are ultimately about trade, central banks hold dollar assets to prop up their currencies and service their dollar-denominated sovereign debt in times of crisis.

Second, the dollar is a store of value. Other countries are confident that U.S. institutions will set prudent policies (such as the Federal Reserve Bank which controls value-eroding inflation). Central banks store dollars and dollar assets because of their prominence as a medium of exchange, but also because they believe the dollar will hold its value over time. Both factors rely, however, on the choices of other nations: were other countries to doubt the dollar’s strength or its acceptability to other countries, they might abandon it for alternative currencies.

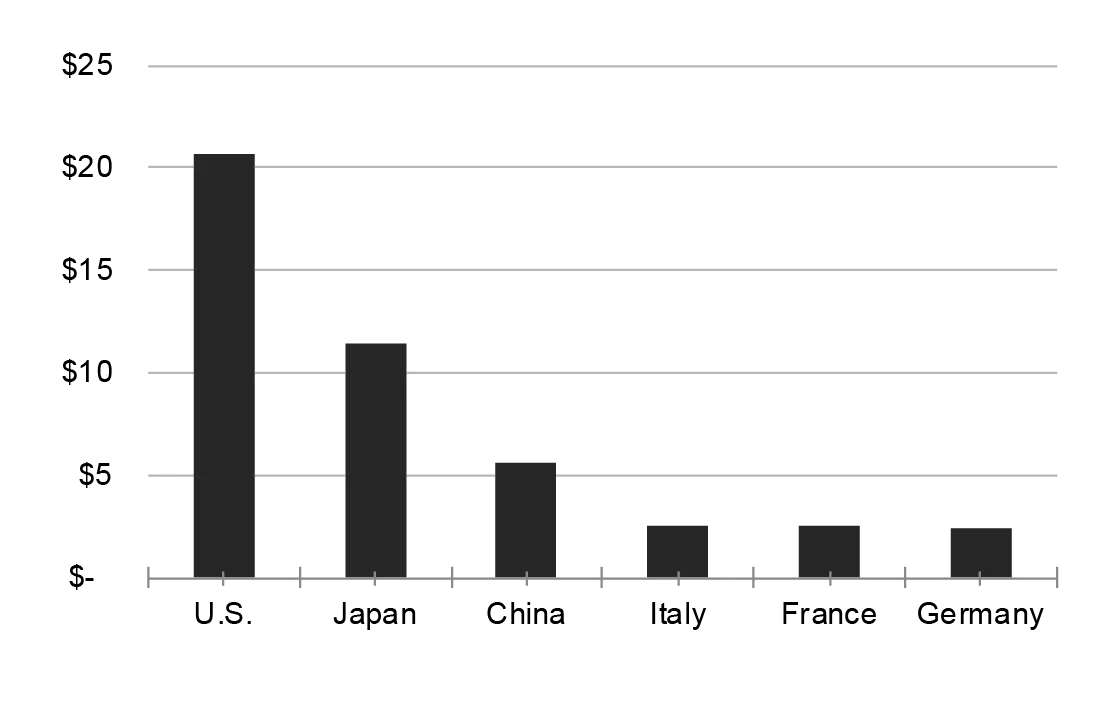

Third, structural features of the system make it difficult to divest dollar assets. No other currency market is as liquid or as large (“deep”) as the dollar markets. The market for U.S. government debt markets is nearly twice as large as the second biggest, Japan’s. (See Figure 3.) Were large countries such as China to divest their dollar holdings, they’d struggle to find alternative assets in which to park their value. Similarly, many countries and firms frequently turn to dollar markets to issue debt rather than their own currencies, increasing the supply of dollar-denominated debt for those who hold dollars to invest in.

Nations, firms and individuals who use dollars must inevitably interact with the U.S. financial system, making U.S. banks and institutions central to the plumbing of international finance. U.S. policies that affect the domestic financial system therefore ultimately affect the global financial system. Dollar holders, searching for investments to earn interest on their dollars, also increase the demand for dollar-denominated assets such as bonds. The increase in savings as populations age and prepare for retirement through personal investments or pension funds (the “global savings glut”) has increased this demand. At best, this demand makes it cheaper and easier for the U.S. government, firms and individuals to borrow money. At worst, it can fuel asset bubbles, such as the subprime mortgage bubble that precipitated the global financial crisis. Nonetheless, the prominence of the dollar in the global economy endows the U.S. with a leadership role in shaping global economic policy.

Key Topics

Secondary sanctions

Primary sanctions prohibit U.S. entities from transacting with foreign third-parties, such as those in Iran or North Korea. Secondary sanctions threaten entities, such as banks, with being cut off from the U.S. financial system if they transact with parties under primary sanctions. For entities such as banks or multinational corporations, losing access to the U.S. financial system is a death sentence. Secondary sanctions are therefore a powerful tool to compel non-U.S. entities to cease economic activity with adversaries of the U.S.

In 2017, for example, the Treasury’s Financial Crimes Enforcement Network (FinCEN) sanctioned the Chinese Bank of Dandong, which laundered money for North Korea. As a result, Bank of Dandong could no longer facilitate transactions for its clients in the United States.84 Leading up to the Joint Comprehensive Plan of Action (JCPOA), the U.S. in coordination with other nations put financial sanctions in place against Iran. As a result of congressional legislation passed in 2012 authorizing the president to sanction SWIFT—the Belgian-based system nearly all banks use to transact with each other across borders—for providing services to Iranian banks, the service severed ties with Iran’s financial sector.85 Following the U.S.’s unilateral withdrawal from the JCPOA, U.S. financial sanctions have prevented European banks, which rely on access to the U.S. dollar system, from transacting with Iranian entities, to the ire of European politicians.

One perspective holds that the U.S. should use these tools aggressively. The Obama administration considered broadening its sanctions against Chinese companies that transacted with North Korea. In spite of European resistance, SWIFT again ejected Iranian banks from its network following pressure from the Trump administration.86 And the Trump administration has since formally withdrawn waivers that allowed Chinese oil companies to continue transacting with Iran, causing China to reduce its purchases of Iranian oil.87

The opposing perspective holds that aggressive use of secondary sanctions without multilateral support encourages other countries, particularly allies, to find alternatives to the dollar. Europe in particular is searching for alternatives: politicians call for an end to the dollar’s dominance and have established Instrument in Support of Trade Exchanges (“INSTEX”) to facilitate marginal trade in humanitarian goods with Iran without transacting in dollars.88 Furthermore, critics argue that were the U.S. to impose secondary sanctions on a systemically important institution—for example, central banks or multinational banks in Europe or China, or global payments infrastructure such as SWIFT—it would cause a global financial crisis.

Threat of Alternative Currencies

While the dollar is still the most used currency by a wide margin, it is losing ground. Central banks have been slowly decreasing their dollar holdings. And Europe, Russia and China have made prominent attempts to create alternatives to dollar payment systems.89 China, perceiving its need to use dollars to purchase oil (nearly all of which it imports) as a strategic weakness, has engaged in “barter” transactions in commodities (mainly oil) rather than dollars. It has also extended as much as $50 billion of official loans to Venezuela that are guaranteed by or expected to be paid in oil rather than dollars.90

To date, however, efforts to replace the dollar on a wide scale have not been successful. In 2018, China and Russia committed to developing the capability to settle their bilateral trade in rubles and yuan. Yet only 10-12% of bilateral trade between the two countries, which increased by 25% y/y in 2018, was settled in yuan or rubles.91 Middle East countries, many of which peg their currencies to the dollar, prefer global oil trade to be conducted in dollars.92 Although nine European nations now participate in INSTEX, it has largely been ineffective, and European banks and multinationals remain wary of doing business with Iran for fear of U.S. sanctions.93 The yuan remains, at 2.0%, the fifth most held currency by central banks. Analysts argue that China’s tight controls on cross-border currency flows and its long policy of running a trade surplus prevent the yuan from being a sufficiently global and liquid market to serve as a reserve currency. China similarly lacks political transparency relative to the issuers of other major global currencies.

Many policymakers and observers agree that the U.S. draws important benefits from the dollar as a reserve currency. However, they disagree on the extent to which the U.S. can use that advantage to its benefit at the expense of other nations before the other nations conspire to develop credible alternatives.

On one hand, some argue that failed efforts by foreign countries to develop dollar alternatives prove the U.S. should not be concerned. Small declines in dollar holdings by central banks are still a long way from threatening the dollar’s dominance. On the other hand, transitions between reserve currencies have historically been a slow process. The British Pound, for example, was replaced by the dollar over the course of decades, and did not fully cease to be a reserve currency until long after the American economy had overtaken the British economy. Although China’s new yuan settlement scheme, the Cross-border Interbank Payments System (CIPS), handled less transactions in all of 2018 than SWIFT handles in a day, China’s attempts to onboard other countries to its global non-dollar payment systems should be taken seriously,94 as should efforts by other countries to weaken the dollar’s standing regardless of their limited initial success. Policymakers should work to build multilateral consensus before deploying tools such as secondary sanctions, as the Obama administration did in the run-up to the signing of the JCPOA with Iran.

Balancing Domestic and Global Priorities in Trade Policy

Recently, the most nuanced debate over how the U.S. should use the advantage of the U.S. dollar and its centrality in the global economic system has focused on trade. By running a trade deficit—importing goods and exporting dollars—the U.S. supplies the world with the dollar liquidity required of a reserve currency. However, the deficit represents potential losses for American firms and workers.

One argument holds that the U.S. should devalue the dollar to improve its trade position. A cheaper dollar would make exports more competitive, boosting the profit of U.S. exporters and leading to more jobs at home. China, proponents of this view point out, in 2019 allowed its currency to weaken below 7 RMB-per-dollar for the first time since 2010 to offset the effects of tariffs.95 By objective metrics the dollar has been overvalued in recent years.96 Therefore, proponents of this view argue, the U.S. should either devalue the dollar unilaterally (with Treasury intervening in currency markets) or through agreements with other economic powers to jointly devalue (as in the 1985 Plaza Accords amongst the G5).

Opponents of this view argue it will harm the U.S. for at least three reasons. First, a devalued dollar would have wide-spread negative effects on the global economy which would ultimately harm the U.S. Central banks would see the value of their currency reserves decline. Governments may tighten policy in response, leading to a worldwide slowdown in GDP, decreasing demand for U.S. exports and harming U.S. industry and workers.

Second, because currency reserves at central banks would be less valuable, their ability to fight balance of payment crises by defending their own currencies would be diminished (i.e., by selling dollars and buying their currency). If their “financial firepower” were to fail, countries would be more likely to turn to the IMF (which is funded in part by the U.S.) for support, or rely on alternatives, such as direct lending from China, that risks eroding American relationships with those countries.

Third, opponents argue that other countries would be inclined to devalue their own currencies in response, offsetting the benefits of a cheaper dollar. Currency wars, where all nations devalue their currencies and make each worse off, could lead to global economic turmoil.

Ultimately, these factors would hasten the erosion of the dollar as a reserve currency and deprive the U.S. of the advantages afforded it. U.S. policies should therefore consider the needs of global constituents who use the dollar to ensure it remains a reserve currency. Furthermore, the U.S. could use its advantages to benefit domestic constituents in other ways, for example by channel demand for dollar-denominated bonds (which lowers interest rates) into productive uses such as infrastructure investment.

6. Reforming the WTO

Aaron Huang

Issue Overview

The perceived unfair trade practices that the People’s Republic of China (PRC) has engaged in over decades and the recent aggressive tactics the United States has used on eliminating its trade deficits have reignited the discussion on reforming the World Trade Organization (WTO). The WTO requires reform in the areas of state-owned enterprises (SOEs), forced technology transfers, subsidies, intellectual property (IP), transparency and reporting, and special treatment for developing countries. The PRC disagrees with the West (namely, the United States, the European Union, and Japan) on these issues, and it has put forth its own proposal for what the future WTO should look like, that is, a WTO that protects developing countries.

Beijing is finding few allies in the developed world for its plan, however, as developed countries seek to (1) end China’s perceived systematic cheating of global trade norms and (2) strip China of its “developing country” status at the WTO. Summarized by Peter Navarro, the White House Office of Trade and Manufacturing Policy Director, the sentiment and resolve to achieve these two goals are strong: “As soon as one bad actor like China massively cheats, they win at the expense of us; they win at the expense of Europe, and over time, it threatens the entire integrity of the global financial system and the global trading system.”97

Background

Founded over 25 years ago in 1995, the World Trade Organization (WTO) is an international organization with the purpose of “open trade for the benefit of all.”98 It was designed to serve four principal functions: operate a global system of trade rules; act as a forum for negotiating trade agreements; settle trade disputes between its members; and support the needs of developing countries.

Since its inception, the WTO has been successful in reducing trade barriers in both goods and services among its member states.99 However, the organization is now in dire need of reform to address an evolving set of issues and areas of potential dispute. (See table on next page.)100

The WTO Appellate Body’s inability to discipline China’s SOEs is an example of how WTO rules must be updated in order to address modern global trade disputes.101 However, many of the structural reforms the WTO needs require unanimous consensus, and Beijing disagrees with developed countries on the issues of government subsidies, SOE discipline, competition neutrality, technology transfer, and IP protection.102 China, resolved to preserve its state-capitalist economic system, is standing against the West’s liberalization proposals and offering its own vision for the WTO to compete against the United States in determining the future of trade norms.103, 104

| Issue | Description |

| State-owned enterprises (SOEs) | Government-funded national champions, through subsidies, have flooded global markets and unfairly driven out businesses around the world, and the current WTO can do little to identify these murky subsidies and enforce its SOE reporting regulations on violating countries.105 |

| Forced technology transfers | For years, Beijing has illegally forced foreign firms that wish to do business in China to reveal and share their proprietary technologies, and the present WTO takes over years to settle a dispute of this kind between countries.106 |

| Subsidies | Countries are arguing that the WTO’s anti-subsidy rules do not take into account the many ways that China supports its industries and SOEs and that other WTO countries have a poor track record of complying with the Organization’s subsidy notification requirements.107 |

| Intellectual property (IP) | Critics, such as the United States, are accusing the WTO of failing to enforce IP rules and effectively impose WTO countries’ “affirmative obligation” to protect IP rights.108 |

| Transparency and reporting | Many WTO members are not meeting their obligations to submit information about their trade regimes, and the WTO at the moment does not punish these countries for failing to be transparent.109 |

| Special and differential treatment (S&DT) | The WTO gives developing countries special rights, including “longer time periods for implementing agreements and commitments, measures to increase trading opportunities for these countries, provisions requiring all WTO members to safeguard the trade interests of developing countries, and support to help developing countries build the infrastructure to undertake WTO work, handle disputes, and implement technical standards.”110 However, countries that have since flourished, such as China and Singapore, still hold on to the “developing country” status to continue to benefit from these special treatments.111 |

Key Topics

China’s WTO Reform Priorities and Strategies

On May 13, 2019, Beijing formally submitted its WTO reform proposal.112 In it, China outlines three fundamental principles that the WTO should follow: 1) uphold the organization’s core values of nondiscrimination and opening, 2) protect development interests of developing members and address their difficulties in integrating into economic globalization, and 3) follow the mechanism of decision making by consensus.113 Flowing from these principles come four of Beijing’s WTO priorities:114115

- Tackle the essential and pressing issues threatening the organization’s existence: China wants to change WTO rules so that countries, such as the United States, can no longer, without punishment, block the appointment of Appellate Body members (those who settle disputes), erect trade barriers using the national security exception as a pretext, and impose unilateral measures inconsistent with WTO rules, such as secondary sanctions.

- Increase WTO relevance in international economic governance: Beijing seeks to reform what it sees as agricultural rules that disadvantage developing countries and trade remedy guidelines that discriminate against enterprises with public interests (i.e. SOEs). It also aims for the WTO to establish e-commerce rules, particularly ones that protect internet sovereignty.

- Improve the organization’s operating efficiency: China wants i) developed members to better comply with notification (of each country’s trade actions and environment) obligations, ii) developing members to receive technical assistance to “endeavour to improve” their notification compliance, and iii) more representation of developing members in WTO subsidiary bodies.

- Increase the multilateral trade mechanism’s inclusiveness: China is asking developed members to respect developing members’ “developing country” status and give them the full S&DT entitled to them under WTO rules. Moreover, Beijing demands that countries halt their discriminatory practices against SOEs, that they be treated as any other enterprise, and that they not be labelled as ‘public bodies.’

In short, the PRC argues that its proposal is needed now to counter the “rising unilateralist and protectionist practices,” suggesting that the United States is the reason the WTO is in an “existential crisis.”116